With the Super Bowl behind us, it’s time get ready for the spring selling season. Traditionally, the months following the big game produce the strongest home sales activity of the year, with purchases generally peaking in May and June. In the new-home market, builders often achieve their strongest absorptions during these months as buyers are motivated to find a home before summer vacation and the start of the next school year.

Last year, we published our top three things to watch for the spring selling season in 2023. We are going to revisit those items and update our list for 2024.

Last Year’s Recap

1. Treasury Rates

Treasury rates, especially the 10-year, are important to the home building industry due to their relationship to mortgage rates. Last year we said: “The uncertainty related to rates is not yet behind us,” and that was the key story in 2023. Mortgage rates bounced between 6% and 8% over the year.

Why it matters: One of the most impactful changes for the housing industry this year is the spread between the 10-year Treasury yield and the 30-year fixed-rate mortgage. As we have discussed, a widening spread can show signs of problems for the home building industry.

The historical average between the two interest rates is about 1.7 percentage points. The spread reached a maximum of over 3 percentage points in June 2023 before coming back down to 2.8 by the end of the year. The spread has compressed slightly more to start 2024. This supports our thesis that mortgage rates will be lower this year, assuming the economic data continues to slow.

2. Home Prices

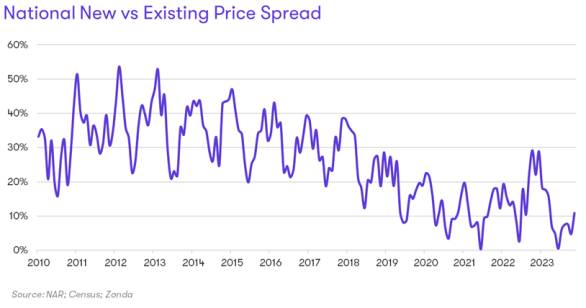

During the housing slowdown in 2022, prices came down in many markets for both new and resale homes. Going into 2023, there was significant uncertainty about what may happen to home prices. What ended up occurring was new-home prices were up marginally from January to November 2023 (latest data) at 0.6%, while existing homes had a stronger year, logging a 7.3% increase.

Why it matters: Since the start of the pandemic, existing homes have appreciated more than new. This has resulted in a narrowing of the price spread between the two subsets. Historically, new homes have been 30% more expensive than resales, but the 2023 average was down to just 9%.

While some of the declining spread is due to builders pivoting to smaller home sizes and locations farther out, a large portion can be attributed to builders getting more competitive on prices with the resale market to maintain absorptions.

3. Listings

Listings started last year up 64% compared with January 2022. However, as the year progressed, the momentum of new listings declined. Inventory ended the year 5% up compared with 2022.

Why it matters: The lack of existing inventory was a boon for home builders. New-home inventory as a share of the overall market rose to 30% compared with 10% to 15% historically.

As we move into spring, we think listings will remain a top item to watch, as well as starts and the path the Federal Reserve takes throughout the year.

This Year’s Top Three

1. Listings, Redux

As mentioned, listings ended 2023 up 5% compared with 2022 but were still down 31% compared with the end of 2019. Baltimore and New York are extreme cases, with inventory down 50% compared with pre-pandemic times.

There are some markets, however, where inventory is rising. These include Austin, Texas (+21% from 2019), Salt Lake City (+13%), San Antonio (+4%), and San Francisco (+3%). Other markets, like Nashville, Tennessee; Phoenix; and Tampa and Orlando, Florida, are just narrowly below pre-pandemic levels. We think this is crucial to watch in 2024 to see if the rise is idiosyncratic or more marketwide as homeowners get sick of putting their lives on hold and decide to sell and purchase a more suitable home for their life stage.

As we see inventory rise, we consider if more listings are good or bad news for the new-home market. The answer depends on who is selling. If investors are selling, then it is more competitive and arguably bad for builders. If homeowners are selling, it means more competition but also more mobility and prospective buyers.

2. Housing Starts

Based on the mixed news from the resale side, we are watching how builders approach 2024. There is still an undersupply of housing in the United States, and many builders are trying to ride out the turbulence of skittish demand. Based on our Zonda survey, nearly 75% of builders are planning on increasing starts this year.

To back up the optimism, there is more lot supply available, and NAHB reports that builder confidence is up slightly as well. We anticipate that single-family housing starts will total 950,000 units in 2024, up 2.2% year over year. Our forecast could understate single-family starts if the early uptick in demand to start 2024 maintains. However, there are risks to the downside as builders navigate the evolving buying pool, relatively tight credit, and general economic uncertainty.

3. Federal Reserve Policy

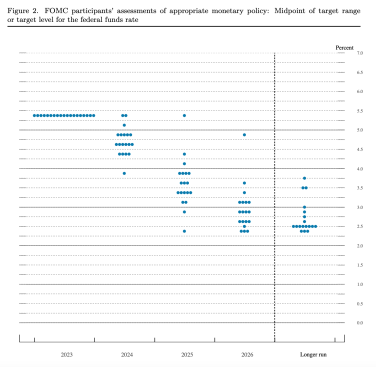

The Federal Reserve aggressively raised rates in 2022 and followed with four additional rate hikes in 2023. However, there has been no further tightening since the July 27 Federal Open Market Committee (FOMC) meeting where rates were set at 5.25% to 5.5% (the Fed sets a band not a specific number).

This is due to inflation softening (although not back to the 2% target) and the Fed’s dual mandate to protect employment as much as possible. The Fed is still hoping for a soft landing, and it is trying to achieve the difficult balance of keeping inflation in check while keeping the labor market strong.

One of 2024’s big stories is if and when the Fed will cut rates. The FOMC’s dot plot, which is made up of FOMC committee members’ forecasts of the federal funds rate (i.e., the dots), shows that rates are projected to come down in 2024. The median projection is to end the year at a federal funds rate of 4.6%. Getting to a 4.6% federal funds rate could be through some combination of 25-, 50-, and 75-basis-point (bp) moves (0.25%, 0.50%, and 0.75% for reference). This could be several smaller cuts of 25 bps, a couple of larger cuts at 50 bps, or even, though unlikely, an emergency 75-bp cut.

Markets are moving well ahead of the Fed’s guidance though, with some projections of six rate cuts starting as soon as March. In previous work, we discussed how mortgage rates tend to lead actions on the federal funds rate. Analyzing data since 1990, we found that 30-year mortgage rates tended to begin declining ahead of Fed rate cuts by an average of seven months. In fact, 30-year mortgage rates were already down on average 13% from the peak ahead of the cuts.

Keep the conversation going—sign up to our newsletter for exclusive content and updates. Sign up for free.