After several years of aggressive deliveries, the national multifamily sector is clearly past the peak in new supply deliveries. Annual apartment completions are finally declining, with roughly 75,000 units delivered in the first quarter of 2026, the lowest quarterly total in three years. While 2025 completions remained above long-term averages, the slowdown in new supply is beginning to ease pressure across the market. At the same time, demand showed signs of improvement, with first-quarter absorption exceeding concurrent supply.

Rent growth remains modest and uneven geographically based on local supply and demand pressures. Early 2026 posted mild rent increases nationally, largely in line with results seen from 2023 through 2025. Gateway and select Midwest markets are leading, helped by limited new construction and improving urban demand. In contrast, many Sun Belt and high-supply markets continue to see rent cuts, likely tied to the sheer volume of units delivered over the past several years.

Scattered SFR REITs show resilience amid softer growth

Performance trends among scattered single-family rental REITs highlight a more defensive posture. Renewal lease rent growth for major operators has gradually ticked down since late 2023, but it remains positive and continues to outperform new lease rent growth, which has turned negative in Q4 2025 and Q1 2026. However, both REITs reported positive new lease growth in April 2026.

Occupancy levels across these portfolios have normalized after peaking earlier in the cycle, yet operators have managed to preserve solid net operating income margins. This balance suggests that while growth is slower, operating discipline and scale continue to support healthy fundamentals within the scattered SFR space.

National BTR market recalibrates

It is important to note that the investor appetite to acquire completed or start development of new BTR projects is effectively turned off due to policy uncertainty. It is likely capital will remain on the sidelines until a housing bill that eliminates the seven-year disposition requirement is guaranteed. As a result, after record deliveries in 2024 and 2025, total BTR completions are expected to decline sharply in 2026 and early 2027 due to uncertainty of federal and state regulatory issues. Even so, the sector continues to evolve. Townhomes are projected to account for the largest share of BTR completions this year, followed by cottages, reflecting renter preferences, developers’ efforts to manage density, affordability, and regulatory risk.

Geographically, the Sun Belt remains the epicenter of BTR activity. Markets such as Dallas and Phoenix are still expected to lead in both unit and community completions, even as volumes pull back from recent highs. Product performance also varies, with single-family and townhome BTR rents outperforming cottage formats, which have faced more direct competition from garden apartments.

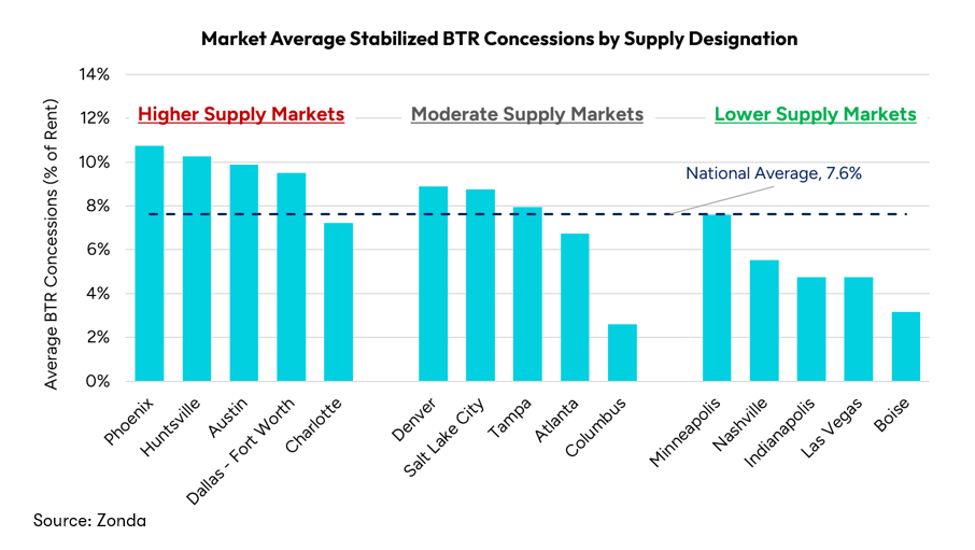

Regional supply and concessions tell a nuanced story

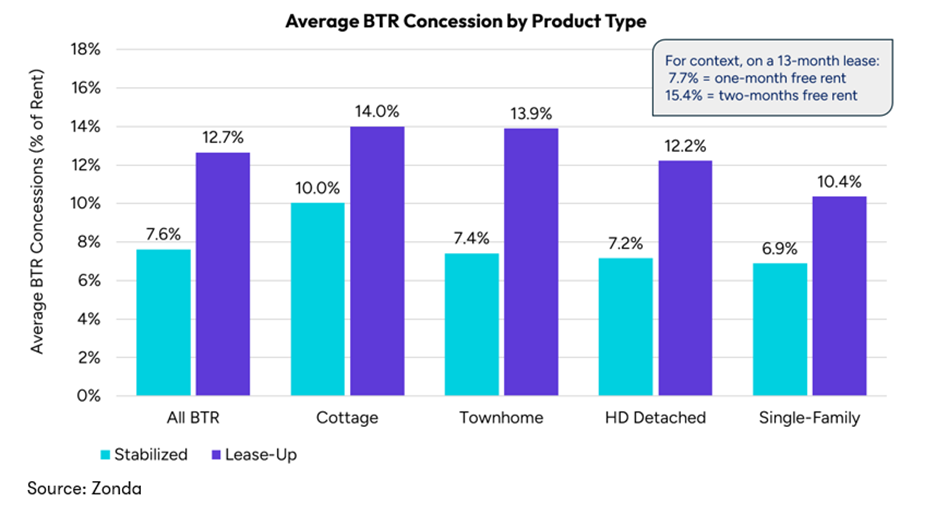

At the local level, concessions have become a key pressure valve. Stabilized BTR communities average nearly one month of free rent, while lease-up properties average about six weeks. Single-family is posting the lowest average concessions, pointing to relatively healthy fundamentals, while cottages have pushed concessions to compete with greater competition.

Notably, concessions are generally highest in high-supply markets and lowest where new deliveries are more limited, underscoring how localized competition has become. Markets like Phoenix illustrate the challenge clearly: heavy supply has pushed concessions higher and occupancy lower, while lower-supply markets such as Las Vegas and Nashville are seeing tighter occupancy and far less concession pricing pressure. For builders and developers, these dynamics reinforce the importance of market selection, product mix, and pacing in a BTR landscape still finding equilibrium.