Adobe Stock

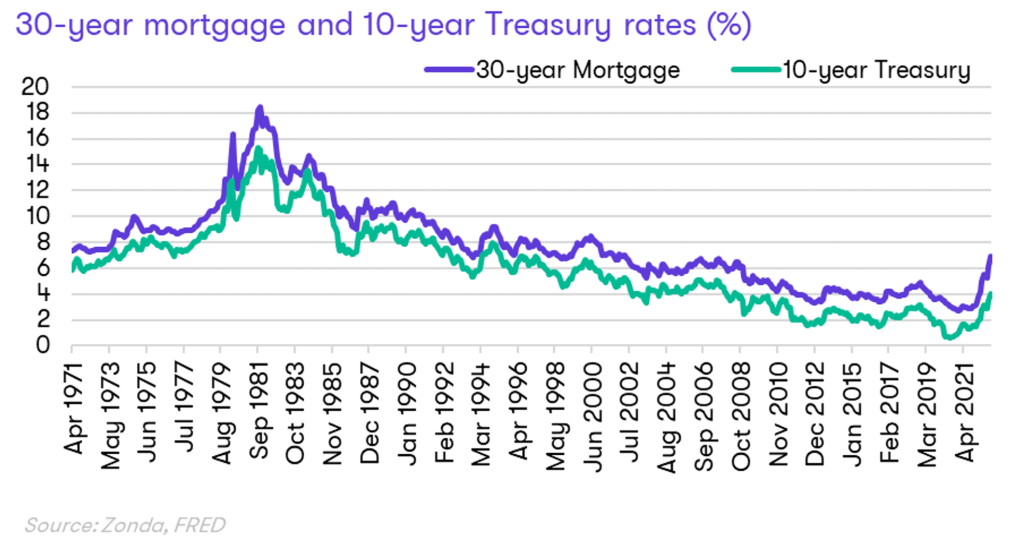

The 30-year fixed-rate mortgage moved past 7% in October to reach its highest level in two decades, far above the estimated 4% many economists had expected going into 2022. These higher rates have put substantial pressure on the housing market as the average monthly mortgage payment is now 75% more expensive than at the beginning of the year. The higher rates raise the questions of how did we get here, and where do we go from here?

Treasury Yield Basics

Mortgage rates are complicated to forecast because there are a lot of factors that come to play, including government bonds, the mortgage-backed securities (MBS) market, and how investors perceive the relative risk of different asset classes. Let’s go through each of those factors, starting with government bonds.

As a reminder, a 10-year Treasury bond is issued by the government to support its spending and obligations. Investors buy bonds because they get compensated for lending the government money.

The yearly interest rate paid by the government is called the yield. Bonds are perceived to be extremely safe investments because they are backed by the full faith and credit of the U.S. government.

The Federal Reserve is directly raising short-term interest rates, which is different than the yield on the 10-year Treasury bond. The bond yield is determined by supply and demand with investors taking into consideration inflation, Federal Reserve policy changes (yields often rise in anticipation of rate increases versus at the time of the rate increases), and how the anticipated policy changes will impact the economy. Investors, then, place their money accordingly.

Oftentimes, the yield on the 10-year Treasury bond will rise due to investor optimism about the U.S. economy. Bond yields and price move in inverse directions, so if investors think economic prospects are good, they will demand less of government bonds and the yield will rise to entice more demand. The 10-year yield can also rise as a result of higher inflation, like what we are seeing today; the yield has more than doubled since the beginning of the year.

Link to Mortgage Rates

Investors looking to place money in the fixed-income markets will compare assets. This is where mortgage rates come into the discussion. Investors looking for a steady return will consider similar products, like comparing government bonds and MBS for example. The MBS market determines mortgage rates.

Mortgage-backed securities are loans that are packaged up and sold to investors. The MBS market has become a bit dysfunctional in 2022 following the Federal Reserve removing itself as a buyer of last resort and investors seeing increased risk in the space.

In solid economic times, default risk is low and investing in the MBS market is deemed relatively safe. However, during times of uncertainty and volatility, like today, investors expect that there is a higher possibility of default due to potential income losses for borrowers; consider the ramifications of duration risk and how they want to be positioned around that; and think through the Federal Reserve’s next step related to their MBS portfolio.

With these considerations in mind, the space has become less liquid and investors have been demanding a higher interest rate to hold or buy more MBS. That, in turn, has pushed the 30-year fixed rate mortgage up.

Given the relationship between the 10-year Treasury yield and the MBS market, and the relationship between the MBS market and mortgage rates, there is a strong correlation between mortgage rates and 10-year Treasury yields.

Relative Risk: Widening Spread

With the relationship established, it’s now time to tie all of this back to peculiarity of today’s times. The dysfunction in the MBS market is leading to mortgage rates rising quicker than what we see during a more stable economic climate.

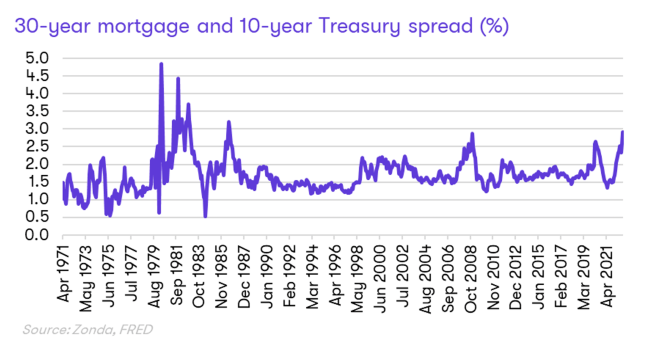

For example, the 30-year fixed-rate mortgage has traditionally been an average of 1.7% higher than the 10-year Treasury yield. Put another way, the spread between the two averaged 1.7%. As you can see in the graph below, periods of economic instability are associated with increasing spreads. The recession in the 1980s was related to high inflation and aggressive Federal Reserve action, and the Great Financial Crisis, the COVID-induced recession, and today’s market are all periods where the spread widened.

The spread between the 30-year fixed rate mortgage and the 10-year Treasury yield averaged 2.9% for the month of October, 1.2 percentage points above the historical average and 1.4 percentage points above levels this time last year.

The wider spread is linked to the 7% interest rates and the notable housing slowdown across the country as consumers respond to the higher cost of homeownership. If the spread were to normalize back to the historical average, we would be looking at a mortgage rate in the mid-5s compared with the low-7s.

The housing market is expected to face continued uncertainty heading into 2023 as consumers, financial markets, and policymakers work through their respective challenges in today’s economy. While the widening spread is making it more difficult to accurately forecast mortgage rates, we are watching for any additional stability in the MBS market, signs of cooling inflation, and/or less aggressive Federal Reserve action to give us confidence that mortgage rates are past their peak.