“There are times when all the world’s asleep,

The questions run too deep

For such a simple man.

Won’t you please, please tell me what we’ve learned

I know it sounds absurd

But please tell me who I am.”

Excerpt from “Logical Song”

By Supertramp (1979)

A couple of weeks ago, I had the opportunity to moderate a panel at the Urban Land Institute’s Spring meeting in Philadelphia on the topic: “New Single Family Homes for Rent Grows Up: Opportunity for Master Planned Communities.”

In the panel, we discussed the evolution of the current single family home for-rent business from its mom-and-pop roots prior to the great recession into an institutional investment asset category.

Starting with buying distressed homes going through foreclosure in the 2007-2008 timeframe, individuals and companies purchased existing homes, did some repairs, and then put them out for rent.

Much has been written about how several companies developed large portfolios of these homes, learned how to manage the diversity of product and location, and then figured out how to finance the growing asset base. Many different business models were tried and some succeeded better than others.

A review of examples of these early deals revealed that pre-tax cash on cash yields, after management fees, fell typically in the 4% to 11% range, mostly depending on the quality of the asset and the shrewdness of the buy.

Around 2012, we started to begin to see some builders taking some of their completed unsold homes and sell them to the growing companies that were managing large portfolios of single family homes for rent. Sometimes representing the last homes in a community or sometimes representing challenging lots, it provided another mechanism for builders to move homes off of their balance sheets.

Although often selling at discounts of 10 to 15% from list price, the hit to the builder wasn’t that bad. They saved sales commissions and discounts/incentives usually needed to move tough-to-sell homes and cut the tail-end fixed carry costs of their communities significantly.

The houses were oftentimes larger than the rental market needed, though. It kind of fit square pegs into octagonal holes.

For the investor/purchaser, the cash on cash yields kind of settled into the 6-8% range.

Also during this period, some home builders began to look at building new homes exclusively for rent, both in communities of for-sale and for-rent homes and then in exclusive communities of just for-rent single family homes. Sometimes the builders put together investment vehicles to own these homes and sometimes they developed relationships with institutional buyers who would manage the homes as part of their portfolio.

In these situations, the “sweet spot” of the ideal rental home for a market became known through market research and trial and error. Typically, smaller in size than normal in the marketplace and with specifications designed for best long-term ownership cycle cost, rather than least expense to drive a selling price, these homes were able to be built over and over again, enabling lower costs and faster cycle times than normal for-sale homes.

As this applied knowledge became baked in to business models, the new single family homes for-rent built in communities or sub-communities together evolved to a fairly stable 6-8% cash on cash yield profile, without giving any benefit to the increasing market value of the underlying asset, which, empirically, seems to add an additional 2-5% annually to the yield, giving an implied 8-13% total unleveraged annual yield before any tax effects.

What intrigued me was that, when given the choice of building new for-rent and new for-sale single family homes, these builder-developers opted for the for-rent model, feeling that it gave them a better economic outcome.

Being like the simple man in the “Logical” song, several questions started arising in my head in the night:

- How did these yield profiles compare to those of the traditional for-sale builders?

- Were there environmental or risk factors that had made this business model more attractive than before?

- Were there any lessons learned that might be applied to the industry as a whole?

To begin with, my prior research had shown that building new for-sale and for-rent homes, often in the same community or subdivision, had been a relatively common business model up until the 1970s. At that point, the industry seemed to bifurcate to one where new single family homes were almost exclusively built for sale and new multifamily were built for rent. The single family home for-rent marketplace consisted almost exclusively of older used homes and were most often focused on those who could not get the credit approvals or did not have the financial wherewithal to purchase a home. There was almost no institutional ownership of used single family homes for-rent. It was the province of mom-and-pop operators. Institutional money, however, did come to be a fairly large player in the multifamily market, purchasing both newly constructed and existing apartment complexes.

To help look at the yield profiles of the single-family for sale business, the equivalent unleveraged return metric is EBIDTA/Assets (Return on Assets). (EBIDTA is Earnings before Interest, Depreciation, Taxes, and Amortization). Long considered the best metric to look at financial efficiency, this blends the income statement and the balance sheet into one metric that looks quite simply at what kind of annual return does one get on the assets employed by the company.

In its most basic formulation, the metric asks the question: if I have a dollar, what kind of annual return can I get on that dollar? 6% is better than 3%, without giving weight to the risks involved. Since higher risks usually demand higher rewards, typically the businesses with the higher risk profiles should enjoy higher yields.

The metric is also a good tool to test whether leverage makes sense. If my core EBIDTA/Assets is, say, 10% and I can borrow money at 5%, that would be smart, as it would be accretive to my return on equity. However, if my EBIDTA/Assets is, say, 4%, and I borrow at 5%, I dilute my return on equity. That’s a bad thing.

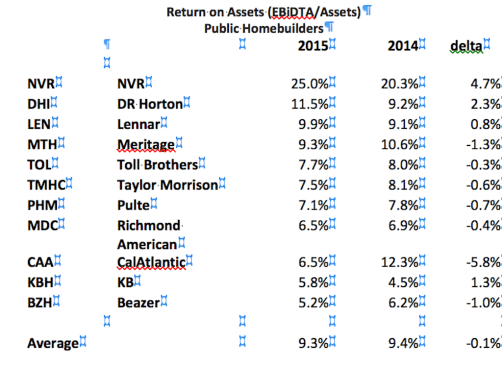

As I started researching the recent Return on Assets data for the public builders from their Annual 10-k filings with the SEC, here is what I found:

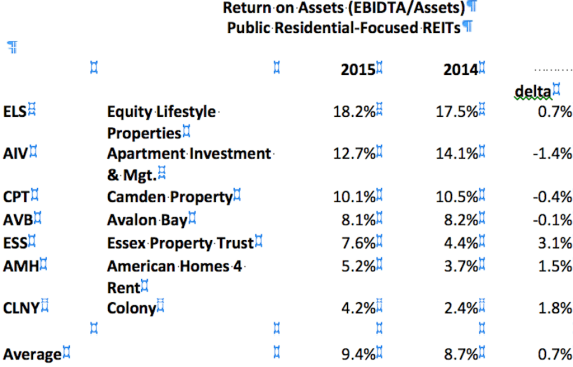

At the same time, I thought that testing the same metric from some of the residential focused REITs would be instructive, also.

A couple of surprising insights came out of the analysis.

First, on the home builder side, NVR is playing chess while everyone else is playing checkers. It is obvious that their land-light model coupled with great operational excellence yields financial returns that are two to four times the others. DR Horton is also meaningfully above the pack, but nowhere near the distance of NVR. More on that in a future article, as this forms another question for a simple man.

Second, most of the public builders tend to cluster around returns in the 6.5-9.5% range, which is not materially different than the cash on cash current yield data from the private builders who have evolved into doing stand-alone single family for-rent projects. The difference is that there is a disposition upside to the yields in the for-rent space that has already been captured in the disposition/sale of the for-sale single family homes.

Third, the average yield for the sampling of public residential-focused REITs is not significantly different than the average for the public homebuilders (9.4% vs. 9.3% for 2015). Since not much disposition activity was reported in the REIT data for the past couple of years, there is still a potential upside to the yields.

Fourth, two of the lowest-performing REITs (American Homes 4 Rent and Colony) had significant parts of their portfolio in the scattered single family for-rent products acquired during the heavy foreclosure period (2008-2014). Although their yields are improving, it brings into focus some of the learning from my ULI panel members that, in several markets, they thought that the run-up in acquisition costs and misunderstanding of repair costs led to situations where building new (at low costs of land and construction) was actually more economically efficient than buying foreclosures. Many thought that, in the rush to get homes, some of the Wall Street backed acquirers overpaid and the data seems to add credence to that theory.

Fifth, the yields on the more standard concentrated rental product, whether it was apartments (AIV, CPT, AVB, or ESS) or mobile-home and RV parks (ELS), tended to be equal to or higher than the return on assets of the public home builders, in general.

And, finally, the return on assets for the REIT world tended to be increasing, where for the home builders, it was decreasing in many cases. However, the top home building performers on the metric (NVR, DHI and LEN) all had improving returns.

So, to answer the first of my “simple man’ questions (how do the yields on communities built specifically for new single-family homes for rent compare to those for standard “for sale” home builders) the answer seems to be “roughly equivalent” with a potential upside taking them into the range of the the best of the builder-developers, but nowhere near the returns that NVR achieves.

As I approach the second question (are there changes that have made the new single-family home for-rent asset class more viable than previously), I think that a variety of well-meaning adjustments in the operating environment have made it more difficult to achieve good returns in for-sale housing and have opened up for-rent. Some of these include:

- Tougher mortgage qualification standards. Current FICO scores for approved mortgages are still 50-80 points above where they historically have been (factoring out the go-go subprime years). Driven in part by the federal agencies providing a good part of the secondary market qualification metrics and in part by banks being overly conservative after paying out millions in fines to governments, the end result is that underwriting is significantly more conservative than previously. Part of this is good, in that it subdues tendencies toward excess. However, the collateral damage is that homeownership and affordability become negatively impacted.

- More constrained federal lending limits on mortgages. Even though the costs of construction, fees, and land have been climbing significantly over the past several years, federal lending limits have either stayed the same or declined, depending on the market, creating a profit squeeze for builders attempting to sell for-sale housing, particularly at the lower price points. On the other hand, these individual occupant constraints do not apply as robustly to those seeking to rent a new home. There is no appraiser to tell the renter that they can’t rent because they might be paying too much or telling a landlord that the rent they want to charge is too much. The free market is more at play. (There is a government constraint risk at play here, however, as we are beginning to see in California and several other states, where market based pricing on rentals is counteracted by rent control legislation.)

- The roll up of institutional quality owners of single family homes for-rent has opened financing vehicles and platforms enabling the packaging of rent cashflow streams into bonds that enable acquirers to continue acquiring new product. The experience of the efficiencies of operating new homes in communities rather than the used foreclosed homes on a detached basis has shown that operating costs before interest can be in the mid-20% to low-30% range compared to the 40+% range more typical of detached rentals and older multifamily rentals, helping with operating yield improvement.

- The stigma of being a renter has mostly gone away for GenX and GenY, plus retiring baby boomers don’t seem to mind renting, either, if the location is right. A generation or two ago, to rent was a sign of financial deficiency. To own was one of the prime indicia that one had achieved responsible adulthood. That paradigm has changed significantly, opening up the acceptance of renting a single family home. Studies still show that a strong majority of GenX and GenY want to own, but, lacking the down-payment, qualifying credit profile, or job security to do so, renting a home is not a bad alternative and renting a new home is even better.

- Experience in master planned communities has shown that sometimes up to 20% of the housing stock is in rental, despite what the CCRs might limit. Developers are now seeing for-rent single family homes filling a demographic need and providing an opportunity for accelerated absorption of lots.

- And, finally, entrepreneurial builder-developers, many times from outside of the traditional home building ecosystem, have experimented with and shown that there are business models that work quite well for single-family homes for-rent in coherent communities and sub-communities.

So, the answer to the second question seems to be that yes, things have changed in the operating and economic environment that help to make this business model more feasible than in the past.

The final question: are there lessons learned that might apply to the industry as a whole?

Here, I think that there are several.

- First, this is an option that every production single-family homebuilder should have in their tool-kit. With yields approximately equal to the ROAs that they are currently getting (and sometimes more), building for-rent might be a more viable alternative to building for-sale and having to discount the selling price in order to move the home.

- Second, to do this, builders either have to have a continuing relationship with one of the REITs willing to purchase homes for rent or develop their own in-house property management and financing capability for rental product owned. (It is no surprise that 50 years ago this type of business model was common for many builders.)

- Third, understand that the home design and specifications for efficiency as a rental are different than a for sale home. Trying to fit a for-sale home into a rental model will knock down returns.

- Fourth, in a world of shrinking margins, the construction efficiencies of doing similar rental houses over and over again lead to lower hard costs, higher volumes, lower cycle times, and more efficient use of overhead. All of these lead to better returns on assets.

- Fifth, the business model allows for the liquidation of homes into the for-sale market at opportunistic times when the conditions are favorable, rather than whatever exists at the current time. This flexibility tends to optimize value to the creator of the asset more often, particularly if the builder-developer becomes the owner-manager.

These lessons of improved flexibility, improved return on assets, and simpler operations are ones that can help many builders.

As I look at this issue, I sometimes wonder whether, for some of the public builders, conversion to being a straight build for-rent model might provide a better return to their shareholders than staying with what they are currently doing.

The model of the current regional or national builder was developed over the past 40 to 50 years when conditions were overly favorable for owning homes. If those conditions have changed over the past decade, might the structure of the new homebuilding company have to adjust also?

That is a great question for the night time thought of a simple man.