There may always be a debate about exactly who or what brought the real estate market to its knees in 2007, but according to leading analysts, there’s no debate over which builders were hit the hardest: those who were sitting on anything but the best-of-the-best locations. At that time, the few buyers left in the market could afford to be choosy—acquiring A- and B-grade spots for C- and D-grade prices. Builders working off the beaten path, or in infill, or in “path of growth” projects, found themselves paralyzed.

“At the beginning of the previous recession, all of the financing was pulled from those particular builders,” says Mark Boud, principal of Real Estate Economics (REE). “Those are the ones who felt it the most, because it halted the development of those neighborhoods and master-planned communities.”

Some of those developments sat with half-graded lots and unfinished amenities for nearly a decade, waiting for values to catch up to original pro formas. Others changed hands—some two or three times—over the same period. But finally, with A- and B-grade inventory a rarity around most metro areas and signs that entry-level buyers are returning, the sound of hammers is slowly coming back in those forgotten markets.

“In 2014 and 2015, public builders were very reluctant to look at C and D markets,” Boud says. “In 2016, they’re beginning to turn their heads a little, and I think developers have taken note of that. They’re beginning to reactivate in those areas, as builders show more interest.”

Trilogy Lake Norman

Denver, N.C.

Purchased: 2013

Size: 606 acres

Planned units: Approx. 1,600

Prices: $260,000 – $420,000

Median New Home Closing Price (2015): $283,800

Description: After discovering that its Trilogy brand developments appeal to more than just boomers, Shea looks to break the mold with Lake Norman by linking it to future economic growth and jobs development, while offering resort-style living 45 minutes from Charlotte.

BUILDER pinned down six projects moving outside of the A and B lines in 2016—many of which are finally starting, restarting, or just reaching stride after a hiatus. Interviews with nearly a dozen builders and developers for those projects, ranging from infill properties to far-out locations, reveal that they’re approaching these markets with a mix of trepidation and newfound confidence—sure of the necessity of their timing, but kicking the tires a little harder on their investments. Nonetheless, these projects demonstrate that, heading into 2016, builders are willing—once again—to take a risk.

Scarce Lots and Rising Costs

With its Trilogy Lake Norman project, which lies 45 minutes outside of Charlotte, N.C., Shea Homes is “moving forward” by moving out—hopefully in the direction of economic growth and industry, says general manager Jay Seymoure. But analysts for the Charlotte market also say that with land opportunities fading, this is partly a matter of necessity.

“The more interior core markets are reaching the point where they’re really more or less built out,” says Jay Colvin, Metrostudy’s regional director for the Carolinas.

Analysts and builders from markets such as Denver, Houston, Las Vegas, and Albuquerque, N.M., say they’re facing the same situations and that it’s time to move in on submarkets.

“You wouldn’t have done this three years ago, because there was still plenty of land to go around right in Denver, at reasonable prices,” says Rick Dengler, regional president for Brookfield Homes, speaking about Barefoot Lakes, one of his company’s developments located about 40 minutes north of Denver.

Brookfield purchased the property in 2007 and is just now getting around to developing it. And although analysts say that Denver has recovered with more momentum than some markets, Dengler says that in order to revive the project for 2016, his company has to “think outside of the box.”

“A lot of Coloradans say, ‘Wow, that’s out there!’” Dengler says. “I tease my coworkers that folks here, when they have to commute more than 15 minutes, they feel they need to book a hotel room.”

But some Californians and East Coasters, Dengler suggests, think nothing of the 30- to 40-minute commute it takes to get from Barefoot to any job market—or at least he’s hoping so. Brookfield is marketing to East and West Coast transplants looking to tap into Denver’s robust gains in employment. In fact, he says that his company is styling its homes around the tastes of those individuals, through a mix of modern and contemporary (California) as well as traditional (East Coast) designs.

Barefoot Lakes

Firestone, Colo.

Purchased: 2007

Size: 1,300 acres

Planned units: Approx. 5,000

Prices: Low $300s – mid $600s

Median New Home Closing Price (2015): $308,900

Description: Located 40 minutes north of Denver, this revived Brookfield development combines an outdoors-oriented flavor with East Coast– and West Coast–inspired designs, in an attempt to attract relocated buyers who are willing to commute farther than most native Coloradans.

Like in Charlotte, though, necessity may also play a role. “I think that in many ways the market has come to Barefoot Lakes, because home prices have accelerated so quickly in Denver,” says John Covert, regional director for Metrostudy in Colorado and New Mexico. “If average sales prices weren’t suddenly clocking in at around $480,000 within the Denver beltway, Barefoot Lakes might not be on the drawing board.”

Similarly, Vinny Pizzonia, co-president of EOS New Homes, a subsidiary of Twilight Homes, says that in his area of Albuquerque, builders who want to offer affordable houses have no choice but to push past the closer-in A and B locations.

Twilight made its name scooping up foreclosed lots right in Albuquerque. But going forward, Pizzonia says, his company has to change its strategy. “A few years ago, there were plenty of foreclosed lots closer in, but now that those lots are all consumed, builders and mortgage companies are moving back out and going after first-time buyers,” he explains. “We started looking around for ways that we could compete, which includes looking for sites that are farther out.”

After forming EOS as a subsidiary, Pizzonia says his company tiptoed into its new strategy with a couple of spec homes built on lots in Los Lunas and north Rio Rancho, about 30 minutes south and north of Albuquerque, respectively. But when the company sold seven homes over a 10-day period, Pizzonia says he knew that its timing was right for starter homes in those regions, with a base price of $79,900.

“It is a little bit further out, sure,” he says. “But we build in other locations about 15 minutes closer in and [know that the extra] 15-minute ride can save you $50,000.”

Risk Mitigation

Even in instances where builders feel driven out by necessity, they’re applying new levels of discipline to their decisions, as well as incorporating strategies to help reduce risk.

With 70 homes completed ahead of its models, Seymoure says Shea feels comfortable moving on at Trilogy Lake Norman to the second of seven phases in 2016. But the builder is moving carefully.

“If you’re operating today and you were around in 2006, then you have to be stronger by default,” Seymoure says. “We’ve all had to up our game from an underwriting perspective. There’s so little margin left for error these days. You just have to be precise and move forward.”

While some of the imagery in Shea’s marketing for its Trilogy brand developments (the company has done a total of 22 since 2001) leans toward active adults, with Lake Norman the company is shooting primarily for a working-class audience, linking them to jobs and economic growth outside of Charlotte. But by integrating some degree of age-targeted development, Boud says, Shea may lessen its risks.

Meridiana

Manvel/Iowa Colony, Texas

Purchased: 2009

Size: 2,700 acres

Planned units: Approx. 5,500

Prices: TBD

Median New Home Closing Price (2015): $280,200

Description: At a 30-minute drive from Houston, this one-of-a-kind project adds new schools, extensive amenities, a new highway interchange, and free transportation to lure residents out to an area where no developer has gone before.

“What we’re doing in the studies we’re conducting for a lot of submarkets is if age-qualified housing is an opportunity, we’ll include that in order to reduce the support needed from jobs within the commute ring,” Boud notes.

It’s understandable why builders move outside of the A and B zones with some level of caution. The last thing they want to discover is that buyers aren’t willing to make the extra drive.

“We’ve been relatively risk-averse when it comes to going too far away,” says Sean Mulroony, director of land for Highland Homes in Plano, Texas. “To be compelling enough of a value, there has to be enough included into a community.”

With the exception of age-based communities, first on every builder’s list is good schools. Three of the communities reviewed for this article report they’re adding private schools or helping to facilitate new public schools as part of their offerings. Mulroony says new schools were partly what lured his company into Meridiana, a 2,700-acre master-planned community about 30 minutes outside of Houston, where he says no developer has ever gone before.

“Meridiana has always been considered to be ‘frontiering it,’” says Dan Naef, president of Rise Communities in Katy, Texas. “Most people say, ‘You’re out there.’ So we all agreed that we needed to create something that’s worth the extra drive.”

As part of its development plan, Rise donated a $1 million tract of land to the local school system for a new elementary school, which is slated to open in August 2016. Middle and high schools will follow, along with a $1 million outdoor learning environment that was planned with the help of a local university professor. The company also is funding 55% of the costs for a new highway interchange and added transportation services into its development to carry residents to and from local employers. So far, the project has drawn the participation of eight builders.

“This one is a little farther out, so we just had to look at exactly what they’re doing to lure folks in—the design and the amenities of the neighborhood,” says Mike Sharp, division president for Perry Homes, another builder entering Meridiana. Sharp says everyone knows that the risk of another downturn is always eminent, but “when you find [a project] where everything is coming together the right way and in the right position, you’ve got to be unafraid to take it and prepare for whatever the case may be.”

Picking the Right Partner

But regardless of how attractive the schools and amenities may be, before builders take those risks, these days they say they look to ensure that they’re taking the leap alongside the right builders. Sharp says his company has passed up numerous opportunities because they would have paired Perry Homes with “the wrong builders,” which he says includes any with a reputation for subpar quality, or those who have no experience building in master planned communities.

Cadence

Henderson, Nev.

Purchased: 1992

Size: 2,200 acres

Planned units: Approx. 13,200

Prices: Mid $200s – $400s

Median New Home Closing Price (2015): $311,400

Description: Located 20 minutes outside of Las Vegas, this massive infill project incorporates features like 450 acres of open space and a social bike program, as well as private and charter K-12 schools, converting a 1940s industrial compound into a family destination.

The same goes for developers. “We got caught in the downturn involved with some developers that weren’t first-tier,” says John Hammond, president of Friendswood Development Company, a Lennar company based in Houston. “Before the downturn, we didn’t do as much due diligence on the seller. Now, we check into not only the land, but the developer. We want to be involved with people who, if there’s a downturn, they’re still going to be there.”

Even with those assurances in place, builders say they expect to see amenities up before they’ll consider signing on to a project. “Putting up a sign that says that the recreation center is coming—that’s not cutting it anymore,” Hammond says.

And developers say they’ve heard that message loud and clear. In fact, for six of the seven projects reviewed for this article, developers are constructing at least part—but in some cases all—of their amenities before breaking ground on homes.

“We did quite a bit of research, including some focus groups and telephone interviews,” says Mark Paris, chief executive officer of Landwell Co., the developer of Cadence, a 14,000-unit infill project in Henderson, Nev., about 20 minutes from Las Vegas. “Because of the downturn and the problems that we had in the housing market, especially here in southern Nevada, some people were skeptical of real estate developments, because a lot of promises were unmet … so we made and continue to make substantial investments on the front end, so people know that we will deliver on the things we say we will. Our research indicates that this was a very important thing to do.”

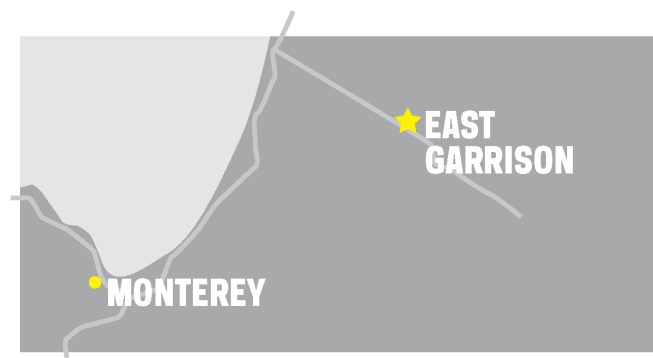

Jim Fletcher, chief executive officer of UCP, says that his company made the mistake of making too soft of a start for East Garrison, an infill project in East Monterey Bay, Calif.

“Initially, everyone locally was very interested in and excited about what we were doing, but sales were slow,” he says. “We opened with a sales trailer, our models weren’t built yet, and there were no production houses.”

East Garrison

Monterey Bay, Calif.

Purchased: 2009

Size: 244 acres

Planned units: Approx. 1,400

Prices: Low $400s – High $600s

Median New Home Closing Price (2015): $496,400

Description: Located just miles from Monterey Bay, this master-planned community revives a decade-old plan for converting a decommissioned military base into a premier community, with a 34,000-square-foot mixed-use town center and its own parks district.

Fletcher says his company knew that East Garrison was a “big risk” when it invested in 2009, and the initial sales made that substantially clear. To make matters worse, he says, the public watched as East Garrison sat in limbo for nearly a decade, as government officials weighed out the best use for the property, which includes Fort Ord, a former U.S. Army post. They also watched a first attempt (by a previous developer) at the project fail amid the recession.

“Understandably, people were a little hesitant to be the first to buy,” he says. “That made it all the more important for us to move forward and build—to pack the vision with product to show how we could transform this into a livable, walkable, vibrant community. You can talk about amenities and show pretty pictures, but people are a little cynical of that these days. So we felt that we needed to really do it.”

While UCP originally set out to include other builders, by 2011 or 2012 its strategy shifted to becoming the master builder, Fletcher says. Amenities were then prioritized to phase one. In 2016—seven years after its original investment—the company is launching phase two.

“All of the sudden, we hit critical mass,” Fletcher says. “We started to get enough homes built that it showed we were fully committed—that we weren’t going anywhere and that it was going to be successful. People began to see it as a new home community with enormous potential, instead of as an old Army base with barracks and mess halls.”

And if these projects are any indicator, “critical mass” may be what’s drawing some builders out of the comforts of A- and B-grade locations and back out to submarkets.