If a historic low one in five households in America is a married-with-children family, how well-suited are the locations, prices, and home and community products builders offer to the other four out of five household types?

Demographics is destiny.

Recognizing that the classic image of a nuclear family in many of our minds today represents only 20% of American households is an important wake-up call for many builders, developers, and investors.

IN THIS SERIES

BE THE BEST OR LIKE THE REST: WHY INDOOR-OUTDOOR LIVING WORKS IN COLDER CLIMATES

BE THE BEST OR BE LIKE THE REST: PLAY YOUR CULTURE CARD NOW

BE THE BEST, NOT LIKE THE REST, PART 3: SWEAT THE LITTLE STUFF

Housing’s recovery–for what it still is–has found itself colliding with two big demand barriers. One is resistance to rising prices from among buyer types who a year or two ago would have anted up. The other is a failure to make inroads among new potential buyer types, expanding the buyer pool.

Demographics, it turns out, is a primitive tool to understand demand, and it’s in the way of solving for that second big barrier. Moreover, household composition patterns at this broad paintbrush level can actually work at odds with basic principles of knowing, creating relationships, and bringing value to your customers.

Let’s take a couple moments for a for-instance or two.

Here’s a piece from Trulia senior economist Cheryl Young, which focuses on a household formation variation we’re likely to need to get to know more about.

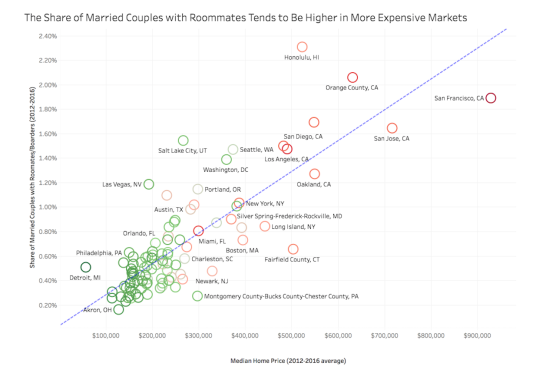

In 2018, 3.28 percent of all U.S. households, or nearly 4.2 million households, lived with a roommate or boarder. But among married couples, that rate was just 0.46 percent (just over 280,000 married households), a scant share to be sure but nevertheless more than double the rate observed in 1995 (the earliest year for which data is available). Among all married householders, 0.46 percent live with roommates, up from an historical average of 0.36 percent. This increase is mostly driven by married homeowners, 0.34 percent of whom live with roommates, or nearly 40 percent higher than the historical average.

The reason for attention to the phenomenon is that it’s expected to evolve from phenomenon to trend, and from trend into a “thing.”

Driving it–just as we’ve found as we explored “root cause” motivations for multigenerational family formations–is a common denominator factor: “for financial reasons.”

While most married couples tend to live without non-family members, the small percentage that take on roommates or boarders are seemingly doing so to help mitigate housing costs—the couple’s, the roommate’s or both. After all, sharing a home offers a financial cushion, even for married couples. In housing markets with the highest rates of married couples living with roommates, including Honolulu and Orange County, Calif., the share is between four and five times the national rate. And it’s probably no coincidence that the areas with the most married-with-roommate households are also fairly pricey: Markets exhibiting the highest rates of married couples with roommates tend to be concentrated on the West Coast, a known stronghold of high home prices.

Among the 100 largest metropolitan areas, those with higher rates of married couples with roommates also tend to have higher home prices. Indeed, on average every $100,000 increase in the median metro home value corresponds to a 0.25 percentage point increase in the share of married couples with roommates, which is more than half of the 0.46 percent national rate in 2018.

Now, housing finance, appraisals, design, and zoning, and planning haven’t so much as begun to fathom the appearance and future traction of this phenomenon–and other emerging household composition types, as well–let alone adapt business and community models to avail of them.

But what better place than in your social networks, and in your sales centers, and among your new and recently sold-through communities to capture knowledge like this that would be invaluable for adaptation, for evolution, for course-corrections that reflect how consumers are morphing their housing preferences, choices, accommodations based on a seminal root cause issue: “for financial reasons.”

Here, too, is a story–with data–on single-person households, another household composition type expected to run fast on its upward trajectory, and will eventually tip balances in new home purchase and ownership. A Deloitte Insights analysis notes.

Projections show that single-person households are set to reach about 41.4 million by 2030, an average annual rise of 1.1 percent over 2015–2030. The projections also show that the numbers will somewhat stabilize for the under-35 cohort, rise steadily for the above-55 cohort, and pick up sharply after 2020 for the 35–54 cohort.

These are just two examples of living choices of more and more people that have big, big, big implications for companies and their partners that expect to make money from developing and building new homes and communities.

What this speaks to–in part–is that while builders, investors, developers, real estate pros, and all of the other partners in new residential construction are so preoccupied with challenges to their own processes, operations, cost-structures, and product-development systems, they’ve become blinded–and deafened–to how their very customers are changing, adapting, re-constituting the very nature of how they become “demand” for new homes and communities. These people–many of them–are either beginning on their journey vis a vis their housing choices, or somewhere well along on the path, or are already customers. They’re talking to you. Are you listening?

Or rather, do we have the talent, discipline, and tools to listen, learn, and put that learning to work in designs, product development, community plans, finance models, etc.?

Many look at exponentially advancing building technology and note that home builders in North America have fallen behind other places in the world, partly because of minimal to no investment in research and development in such advances.

One might look at where builders are on another learning curve–the science of engaging consumers, their customers, their future customers, their former customers and designing great buying and ongoing living experiences for them, from scratch–and note that, in most cases, builders are as early in the learning curve as they are on the construction technology side.

Think of it. Amazon. Google. Apple. Facebook. Microsoft. They would pay–and they do–for what you know about your home buying customers. You know what inspires, motivates, and changes behaviors relative to the most important physical thing most people invest in in their lives.

This is data that you either learn from, or don’t. What lessons have we learned from this recovery? Data scientists–specializing in consumers, not land, or investment, or operations–may not seem as if they’d be a fit for many home building companies. I’m curious as to why that might be.