The days of the turbocharged pandemic housing market are behind us as mortgage rates have doubled from 2021 lows, the relocation boom is cooling, and housing monthly payments have pushed beyond reach for many. We are now entering a new phase in the housing market, one that can be described as an impasse. There is a buyer and a seller strike today as both groups are having difficulty reconciling their views on the market.

As a result, new-home sales have fallen dramatically since the start of the year and existing home sales are back to late-2011 levels. The slowdown in sales is both supply and demand related.

To make sense of the current impasse, we put ourselves in the shoes of buyers and sellers to see different factors that are driving their behaviors and explore ways to break the gridlock.

Buyers Strike

From the buyer point of view, confidence and affordability are key factors influencing their decisions. While there are still active shoppers out there, those that have pulled back from the market have done so for a variety of reasons:

- FOBATT. Scars from the Great Financial Crisis are fresh enough that perceived changes in the housing cycle put consumers on high alert. What the Zonda team has observed is that people moved from fear of missing out, or FOMO, earlier this year to fear of buying at the top, or FOBATT, today.

- Federal Reserve words and policy. The Federal Reserve added to the angst by saying in a recent speech that the housing market was in a “bubble.” Further, the Fed has insisted that it will maintain restrictive monetary policy in an effort to tame persistently high inflation, which could result in an economic recession.

- Job security concerns. Unsurprisingly, potential home buyers are increasingly hearing the word “recession” and are catching wind of layoffs. The most notable layoffs so far have been in the tech sector (Twitter, Meta, and Stripe), real estate (Redfin, LoanDepot, and Zillow), and entertainment (AMC and CNN). We are tracking to see if layoffs spread more widely, but even this kind of uncertainty has caused some potential home buyers to evaluate if now is the right time to make one of the largest purchases in their lives.

- Affordability. Prospective home buyers that are renting have been rethinking the rent-versus-own equation given the current levels of affordability. Many have chosen to put their house hunting plans on hold.

- The lock-in effect. Prospective home buyers that already own are also tracking affordability trends but have an even bigger concern: the differential between their current interest rate and market interest rates. Nationally, 90% of homeowners have a mortgage rate under 5%, and nearly 55% have a mortgage rate lower than 3.5%. This is creating reluctance to act due to what is known as the lock-in effect. Even if a seller is willing to reset their mortgage rate to trade up or down, they may find selling in the resale market a challenge today given the pullback in the broader market.

It is not just primary buyers that have pulled back, however. iBuyers, for example, are slowing down purchases as well. Zillow and Redfin have completely exited the space, while others such as Opendoor are significantly scaling back. Zonda analyzed public record data and found a 73% reduction in iBuyer activity from August 2021 to August 2022. These cuts are linked to the currently lower levels of housing demand, especially in markets where they were particularly active, like Phoenix.

Sellers Strike

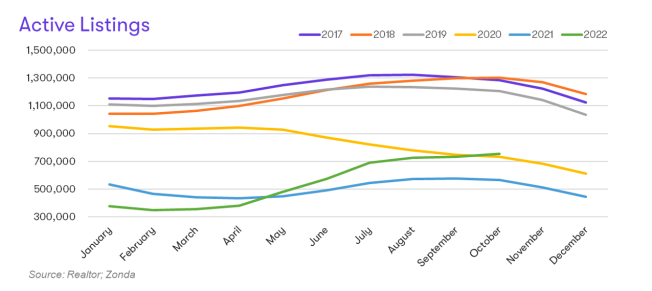

On the seller side, we are still operating in an extremely limited supply environment. Active listings finally picked up this year after troughing during the spring selling season of 2021. The increase, however, leaves the overall market down about 38% compared with 2019, and the rate at which new listings are posted is slowing.

Finances and optionality are the main drivers behind action or inaction for sellers:

- Lock-in effect. The lock-in effect works on both buyers and sellers. Some potential sellers are questioning the wisdom of selling and therefore resetting their interest rate. This is especially true as many sellers may be getting less home for more money due to higher rates combined with still-elevated home prices. It should be noted, however, that the lock-in effect doesn’t apply to all homeowners. For example, U.S. Census Bureau data shows that nearly 42% of homeowners own their home free and clear and that trend is concentrated in homeowners that are 55-plus. For these homeowners, the lock-in effect is a non-issue.

- Rental alternative. Some potential sellers may still move without contributing to the housing supply. Given the low borrowing costs secured over the past couple of years, there are existing homeowners that are choosing to hold an existing home as a rental and move into a different primary residence, pulling from the supply of for-sale homes without adding to it.

- Knock-on effect. People and their actions are at the core of the housing market. Individual decisions to buy or sell will inevitably have a knock-on effect on subsequent individuals, the classic example being the rampant FOMO in the pandemic housing market. Today, the lack of compelling options for purchase on the resale market creates a vicious cycle where fewer people choose to sell, which leads to fewer options on the market, which leads to fewer sellers and so on. The new-home market is filling this gap to some extent, with Zonda data showing quick move-in inventory up 40% since 2019; however, the new supply isn’t enough to offset the lack of new resale listings.

- Trying to time the market. While we haven’t seen it in a couple of years due to pandemic-related abnormalities, the fall and winter are historically slower times for the housing market. Listings normally slow as buyers and sellers get distracted with the holidays. Sellers may be holding on to listings until spring 2023 for hopes of more buyers and a stronger market.

- Federal Reserve and the direction of the economy. As on the buyer side, sellers are also watching to see what actions the Federal Reserve takes over the next few months to get a better sense of the direction of the market. While buyers are having FOBATT, some sellers have the fear of selling at the wrong time.

Breaking the Impasse

Something must give on the buyer side, seller side, or a little of both to break the impasse. Below are a few ways we could see some balance return to the market:

- Lower rates. A better-than-expected inflation number, a Fed policy pivot, a more normal spread in the fixed-income markets between bonds and mortgage rates, and/or deepening recession fears could push down mortgage rates. This, in turn, would help both buyers and sellers through better financing terms.

- Sweetened deals. Even without lower rates, aggressive mortgage rate buydowns offer a costly but effective way to help with affordability. Both fixed-rate and adjustable mortgage rate buydowns help lower monthly payments for prospective home buyers and the phrase “date the rate, marry the house” is used across the country to get potential buyers off the fence. Beyond mortgage rate buydowns, increased use of incentives, especially when combined with lower home prices, can entice consumers to get off the sidelines and reenter the market. Everyone likes getting what they perceive to be a “deal.”

- Dry powder. There appears to be a lot of “dry powder,” or money, sitting on the sidelines from investors looking to reenter the housing market at the right price.

- Motivated sellers. While total inventory levels are down, we are watching for what we are calling motivated sellers—sellers that have a reason to sell ASAP. Investors, iBuyers, flippers, and even home builders can fall into this group depending on their holdings, financial plans, and perception of where the market is going. Motivated sellers not only increase the supply of homes but help get consumers off the sidelines if price cuts and/or incentives are used.

- Selling for economic reasons. If/when the wider economy does fall into a recession, there may be job losses that force some to cash in on their accumulated home equity. Further, those that bought based on additional income related to commissions or bonuses may need to reevaluate their housing needs if their total pay stays depressed for too long.

As is typically the case in negotiations, both buyers and sellers will need to compromise to reboot the housing market. While rates remain high (though have fluctuated wildly over the past few months), sellers will need to lower asking prices or offer various other incentives to help with affordability constraints, while buyers will need to move on from dreams of historically low rates and accept that timing the market is a fool’s errand.