Reversals of Fortune: Remember when, only a few years ago, build…

Click here to see the 2009 Builder 100 list.

When the U.S. CongressionalBudget Office (CBO) released its outlook for America’s housing market in November 2008, it accentuated, if nothing else, just how hard predicting the future can be for a business sector in recession. Using three different economic scenarios, CBO shakily projected that annual housing starts between 2008 and 2012 would either increase to 1.72 million or continue to tread water at 620,000, far below what CBO saw as the market’s “underlying demand.”

Most builders would gladly have settled for that lower projection in 2009. But even CBO’s worst-case scenario turned out to be wishful thinking as housing starts fell to 554,000, dropping below one million units for only the second time since 1945. Single-family starts, at 444,000, were the lowest on record since 1959.

Diminished construction was hardly surprising, given the anemic buyer demand builders confronted. New single-family home sales, at 374,000, fell nearly 23 percent from a limp 2008, and represented fewer than 8 percent of all homes sold, about half of their historical portion. New homes fitfully competed with mountains of existing homes on the market (almost 3.3 million at the end of the year), many of which were foreclosures with bargain-basement prices.

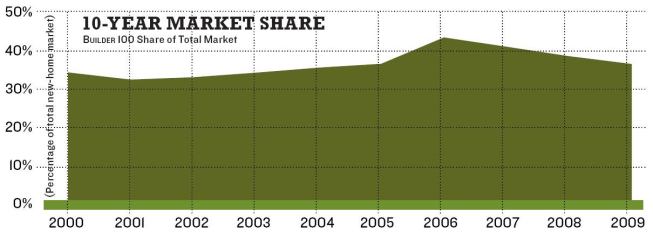

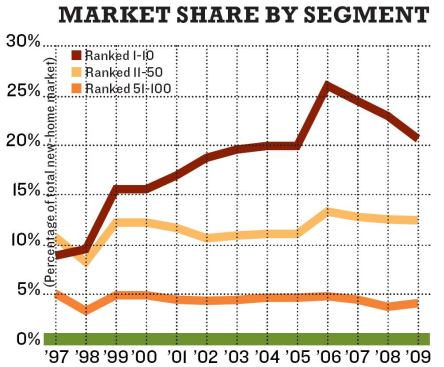

The builders comprising the 2009 Builder 100 were pretty much in the same boat as the rest of the industry, struggling to find customers and to complete sales. Their closings fell by nearly 29 percent from the previous year. Their market share of 439,000 total single-family and condominium closings declined from 2008 levels. Evidence that builders ranking between 51 and 100 picked up share was tempered by the reality that any gains were off of a significantly smaller base number than in 2008. And the possibility of bankruptcy or worse still loomed over some companies.

The financial precariousness of some builders limits the comprehensiveness of our Builder 100 ranking for 2009. At least two builders admitted they were withholding data because they are currently in workout situations and didn’t want to disclose publicly their closings or revenue to their creditors. Other builders simply chose not to release data at a time when their businesses remain weak.

That being said, our ranking shows that 2009 wasn’t quite the disaster of the previous year. Twenty-six of the top 100 builders reported positive increases in closings, compared to only five in 2008. Sixteen builders enjoyed revenue gains, three times the number in the previous year. Admittedly, many builders sacrificed revenue and profit for market share. But new-home pricing found its bottom in more markets.

2009 Builder 100 Coverage

-

2009 Builder 100

See the complete interactive Builder 100 list.

-

Builder 100: The Housing Industry Finally Hits Bottom In 2009

But uncertainties such as rising mortgage rates and impending foreclosures leave a strong recovery in 2010 in doubt.

-

Home Buyer Demand in 2009 Finally Hit a Bottom It Could Bounce Back From

Builders say they’re working twice as hard to keep their heads above water.

-

Top 10 Builders Slogged Through Tough 2009

Our annual Builder 100 survey reveals how the leaders ceded market share again last year.

-

Modular Builders Use Innovation to Drive Sales

Although not immune to the downturn, some factory-built firms survived by turning to new products and ideas.

-

Top Builders Disappear

It’s not a mistake: The industry’s longtime major players didn’t make the 2010 rankings.

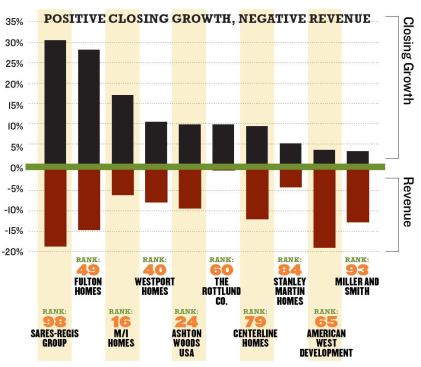

Even builders in recession-wracked areas prevailed. Take, for example, Dominion Homes, the Dublin, Ohio–based builder that four years ago was teetering on the brink. Its salvation came from an investment group that acquired Dominion and took it private in 2008. Last year, Dominion ranked among the industry’s leaders in revenue and closing percentage gains. Lombardo Homes, operating in what owner Tony Lombardo calls “the worst housing market in the country,” cracked into the Builder 100 for the first time and led the industry in percentage increases in closings. Lombardo attributes his success to “being willing to accept change early.” Back in 2004, when signs of economic trouble were burbling, Lombardo Homes adjusted its products and price points. Operational efficiencies helped lower the builder’s construction costs 15 percent. Lombardo was also opportunistic when, in 2008, it acquired Centex’s assets in Detroit, which included 498 lots, and secured a construction management contract to build out 120 homes. Its lenders worked with the company to sell the 90 to 120 spec homes it had in inventory. Lombardo projects that his company will sell 250 to 300 homes in 2010, and close 220, but he’s still looking to reduce overhead. “Everything’s a process here.”

The Defense Department’s military base consolidation program turned out to be a godsend for builders in the right markets. H&H Homes in Fayetteville, N.C., near Fort Bragg and Camp Lejeune, saw its market share increase to 22 percent in 2009 from 7 percent in 2006, even though overall starts in Fayetteville were half of 2006 levels. H&H leapt 43 places on the 2009 Builder 100 list and ranked first and second, respectively, in revenue and closing gains. Ralph Huff III, H&H’s CEO, explains that joining his local Builder 20 Club in 2004 propelled his company’s production by exposing it to new systems and processes. “Last year, we budgeted for 300 homes, but built almost 200 more because we were able to adjust.”

Huff notes that even in a tough borrowing environment, lenders still financed H&H’s construction of spec homes, which account for 80 percent of its production.

But banks also pulled back on mortgage lending, leaving FHA as one of the few sources where home buyers could turn for loans. Consequently, builders continued to create smaller, less-expensive products, not only to meet those buyers’ needs but also to compete against resales and get their own costs down. As a result, the median floor area for house starts fell to 2,107 square feet in 2009 from 2,230 square feet in 2007, according to Census Bureau estimates. The NAHB reported that a recent poll of its members showed that virtually all of the respondents are building smaller houses now. Those smaller products helped stimulate demand for builders such as KB Home, whose “Open Series” of houses accounted for half of the company’s sales last year. Other builders drew buyers with homes under 1,000 square feet.

The first quarter of 2010 offered positive signs that home buyer demand is picking up across the country. But with market conditions still uncertain, builders will need to be hyper-vigilant about their business practices, and more selective in pursuing growth, to sustain whatever momentum they attained last year.

Learn more about markets featured in this article: Raleigh, NC, Detroit, MI.