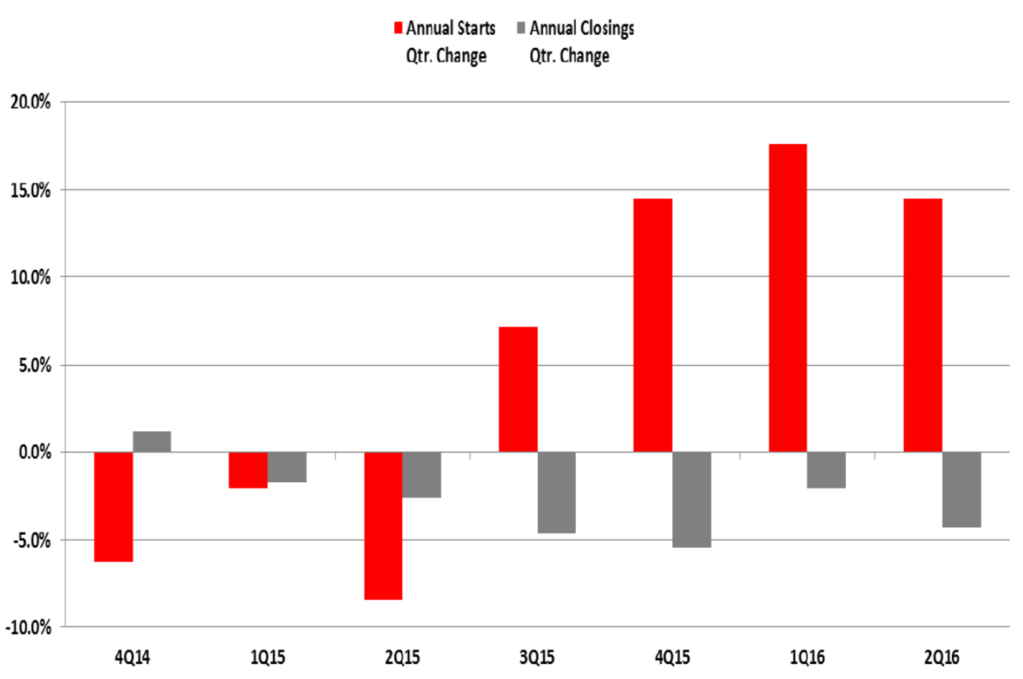

Metrostudy’s 2Q16 survey of the housing market in the Central/Northern New Jersey & NY Suburbs region shows the new home construction market had 1,595 starts in the quarter, an impressive 92.4% increase from 2Q15. There were 920 closings for 2Q16, down 16.4% YoY. In 2Q16, annual starts ended the year with 6,044 new homes started, a 65.1% increase from the annual pace in 2Q15, and annual closings totaled 4,021, a 15.5% decrease YoY.

“Development of the multi-family product in the Northern New Jersey market in particular has been the leading driver in the market,” said Quita Syhapanya, Regional Director for Metrostudy’s Northern New Jersey & New York Suburbs market. “There may be a cap to this development at some point as rents are skyrocketing to levels that just don’t make sense. The rental market was an attractive, cost saving alternative for people looking for a place outside of Manhattan in the Northern New Jersey market, but with rents rising as fast as they are this could be the key ingredient in getting home buying back in play, in particular new home construction markets close to the Hudson River as proximity to public transit is an important factor when a buyer does buy a home in Northern NJ.”

In 2Q16, Northern New Jersey has picked up where it left off in the prior quarter with strong momentum in new home starts at 2,971 annual starts, which is a 175.1% increase in annual start over 2Q15 and up 30.2% over last quarter. Starts have been on a roll for the past three quarters and have continued to increase. New home starts totaled 883 in 2Q16; the most quarterly starts recorded in Northern NJ since Metrostudy started tracking the data in 2Q13. On the other hand, quarterly closings decreased by 15.7% YoY, but bumped up 10.5% QoQ. Keeping an eye on new homes that started occupied as well as move-ins to any finished vacant inventory in condo projects will determine how far this market can expand or if it is starting to show signs of softness.

Central NJ started 537 homes in 2Q16, a decrease of 23% from 1Q16 and a big 27% increase from 2Q15. Annually starts totaled 2,308, up 5.2% from 1Q16. Looking at closings, 2Q16 saw 544 homes occupied for the quarter, down 19.5% QoQ and down 2.9% YoY. Annually closings are also down slightly, 0.7% lower than 1Q16. The market has gone through a majority of the finished lots in Central NJ. There is only 21.3 months of supply which is on the low side for equilibrium and down from the 23.1 last quarter.

Total housing inventory – models, units under construction, and finished vacant units – ended 2Q16 with 7,430 units, up 10.2% from 1Q16 and a big lift of 40.1% YoY. Units under construction totaled 4,033, a 5.3% increase from 1Q16 and a big 53.7% upward swing from 2Q15. Finished vacant inventory increased to 3,062, up 16.3% from 1Q16 and up 27.3% YoY. The increase in finished vacant inventory is one indicator that shows some softness in the market, but it is related more to condo inventory that has come to market recently. Total Inventory months of supply for 2Q16 was at 22.2 months, up from 19.3 months the prior quarter. The months of supply has increased due to the new under-construction units as well as new unoccupied condo units in 2Q16. The market is still on the high side in regards to housing inventory months of supply only because of the condo units that are brand new in the market. Single family detached months of supply is at 9.7, slightly down from 9.9 in 1Q16.

For 2Q16, there were 7,099 Vacant Developed Lots (VDL) in the market, representing a 4% decrease in developed lots in the region from 1Q16 and an 11.7% decline YoY. This region has 14.1 months of supply of vacant developed lots remaining: this is significant drop in available lots, a decrease of 2.7 months from last quarter. A healthy market supply level for equilibrium would be between 24 to 30 months. There were 1,300 lots delivered into the market this quarter, down 19.3% from 1Q16 but up a big 152.4% from the 515 delivered in 2Q15.

“The Northern New Jersey/NY Suburban market continues to be under supplied. Lot affordability is a big concern in a market that is still on the rebound for the new home for sale market,” said Syhapanya. “There is very limited land available for new development in the market and, although the pace of annual lot deliveries ended 2Q16 up 74.2% over the pace in 2Q15, most of the lot deliveries are for high-density attached product. Seeing how fast those homes get absorbed will be important to close out the year.”

For further analysis of the Northern New Jersey/New York suburbs market, reach out to regional director Quita Syhapanya: [email protected]