Zonda recently completed its seventh annual millennial survey. The results provide detailed insight into the minds of the largest living generation as they think about buying, renting, and all things housing.

Millennials—born between 1980 and 2000—are a critical demographic for the housing market and wider economy. The cohort has the second-highest after-tax income among generations, and the group represented 28% of home sales in 2023 per the National Association of Realtors. For both statistics, millennials were second to baby boomers.

Understanding millennial dynamics is crucial for home builders, given their large influence on the housing market’s performance. Here’s what we learned about income and savings from the survey.

Millennials Earned More in 2023

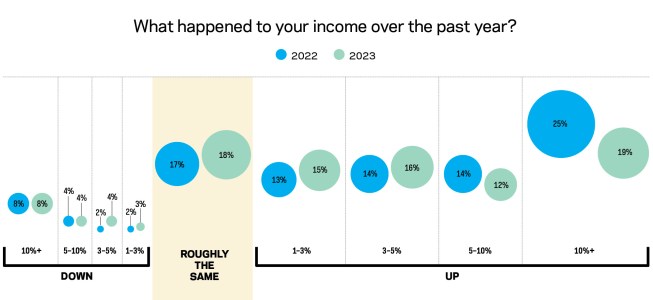

Sixty-two percent of millennials reported higher incomes in 2023 compared with 2022. This aligns with federal data for the wider economy that shows wages and salaries for private workers rose 4.3% year over year at the end of 2023. From our survey:

- 19% reported their incomes grew 10% or more in 2023. This was a decline from 2022, when 25% reported income growth of over 10%. The 10%-plus income change was the only category with a material deceleration compared with the prior year. This might seem concerning, but double-digit income growth was a significant contributor to inflation. A slowdown in these wage increases can be seen as a positive step toward price stabilization.

- 19% of millennials also noted some level of pay decreases over the past year. While this is similar to the 16% captured in 2022, it is worth understanding why. A softening job market with rising layoffs and/or cut hours could be partly to blame. However, some decreases might be voluntary.

Millennials may be prioritizing work-life balance, potentially taking lower-paying jobs that offer more flexibility. Further, some may have relocated to more affordable parts of the country and took a top-line pay cut as a result.

Source: Zonda

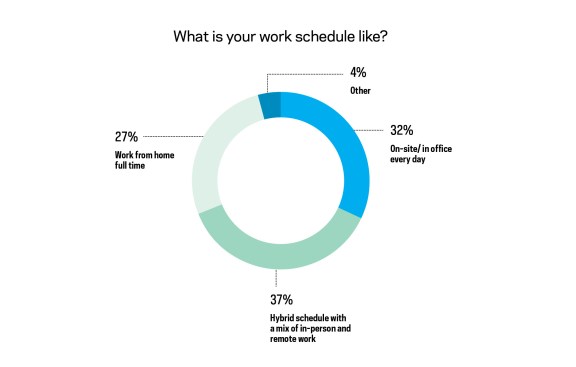

While there are some millennials who moved and switched jobs, our survey captures that nearly 1 in 5 are working remotely in a different state. If they moved, this cohort likely retained their annual salary while changing where and how they work.

In general, though, two-thirds of millennials we spoke to work from home at least a portion of the time.

This trend holds particular significance for the home building industry. Instead of being focused on living near employment hubs, many millennials may have opted to reside farther from their employers to capitalize on reduced living expenses and better housing options. This can, in effect, increase their relative annual earnings as they put less of their monthly budget toward housing and commuting expenses.

Source: Zonda

Millennials Are Saving Money at a Decelerated Rate

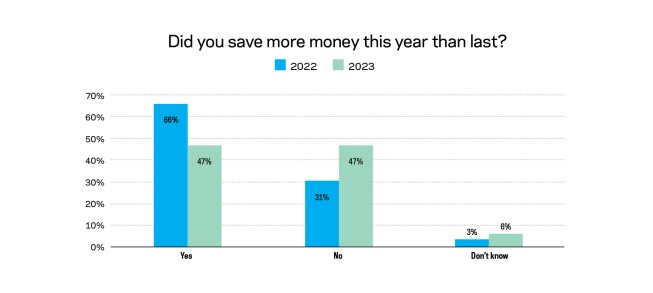

While nearly half of millennials saved more in 2023 than 2022, it’s a decrease from the previous year’s impressive 66%. This mirrors a national trend of declining personal savings rates due to the resumption of student loan payments and higher cost of living across the economy.

Source: Zonda

For the 47% of respondents who saved more money, a mix of factors is likely at play: rising incomes, flexible work arrangements lowering commute expenses, relocations impacting housing costs, and a growing focus on saving.

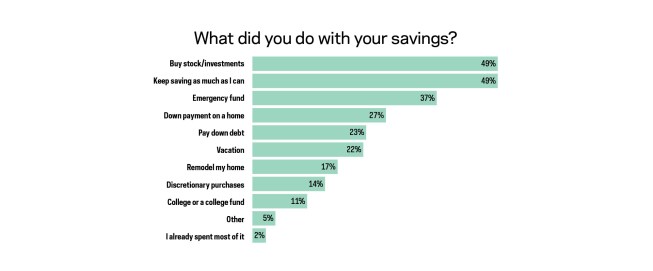

We asked millennials what they did with their savings. While some used the money for home-related expenses, a significant portion is set to fuel housing demand in the future. We capture this future tailwind through three of the responses:

- Buy stocks/investments. This can translate to future down payments as their wealth grows;

- Keep saving as much as I can. This builds their financial cushion for a future home purchase; and

- Pay down debt. This improves their debt-to-income ratio, making them more attractive borrowers.

Source: Zonda

Millennial savings show a divided picture, though. While many have increased their nest eggs, nearly half haven’t seen a rise or even experienced a decrease. The restart of student loan payments is partly to blame.

From 2020 to 2023, student loan forbearance provided a reprieve to nearly 43.4 million borrowers. According to the Federal Reserve, the average monthly student loan payment is between $200 and $299. This translated to significant savings for many. For instance, a couple where both partners have student loans could have saved an average of $600 per month during the forbearance period.

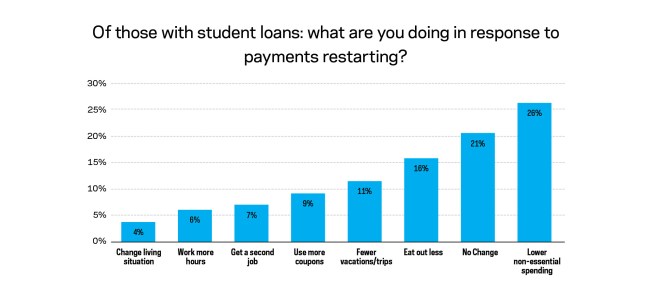

The forbearance period ended in October. We asked our respondents what they were doing in response. A significant portion planned to adjust their spending habits. Over a quarter, 26%, aimed to cut back on nonessential spending, while others planned to reduce dining out, 16%, and vacations, 11%.

Source: Zonda

With the return of student loan payments, the housing market faces a renewed headwind. Prospective home buyers may struggle to save money toward a down payment or meet mortgage qualifications. The end of forbearance may further delay homeownership dreams and dampen consumer spending for millennials, putting a potential strain not only on home buying activity but also on the overall U.S. economy.