Funny how things work.

Only 24 or 36 months ago, the big, burning question for residential developers and builders was “will 30-somethings buy homes?” and the marketplace has quelled worries that demand from that generational cohort that needs no introduction would never materialize.

It has. Big time. And–factoring for a three-to-five year delay thanks to a combo of influences ranging from college debt to a slower pace of maturity and rate of commitment to a life partner of some sort–demand for single-family homeownership in the mid- to late-30s is going great guns right now, from what we’re hearing.

Tables have turned on the big, burning question. A fear about a structural housing shift–that young adults would turn away from homeownership in droves because they wanted nimbler, more urban-connected, less financially-onerous households–is now calming down, but another is emerging in its place, especially in the wake of the recently enacted Tax Cut and Jobs Act.

The big, burning question now–just three short weeks from Super Bowl LII and Ground Hog Day, the unofficial start to 2018’s Spring Selling Season–has to do with older Americans and homeownership patterns–which is particularly relevant to home builders, who view the 55+ customer segment as one of the top two areas of demand for new homes. The question, then, is will tax reform further dis-incentivize retiring Americans from buying the house of their dreams to serve as their post-career home and community?

Here are a couple of perspectives that lend evidence–and, perhaps, spark anxiety–around the question.

Urban Institute economics and research associates Laurie Goodman and Edward Golding conclude that, net-net, taxpayers’ gains in the form of paying lower taxes may actually influence them to rent rather than to buy. Goodman and Golding write:

While most taxpayers will pay lower taxes, allowing them to save for a home more easily if they choose, the increased standard deduction means fewer taxpayers will itemize. The reduction in tax rates also suggests less of a benefit for those who do itemize.

The net result is that renting will look more attractive than homeownership to many Americans in 2018 and beyond.

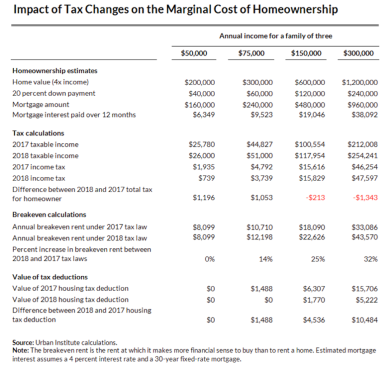

Goodman and Golding’s analysis looks at four household income levels to draw out how tax reform will look and feel to families considering renting vs. buying. Here’s a scenario that might be somewhat more common among 55+ adults considering a next step in their housing journey.

The savings from homeownership is slashed dramatically—by $10,484 per year, or $874 per month. Under the 2017 tax code, the family would choose to own once rents hit $33,086 per year ($2,757 per month) or more. The breakeven point in 2018, however, will now be at $43,570 per year ($3,631 per month), a 32 percent increase.

Do we expect people not to buy because of these changes? At the margin, yes. But because homeownership is generally more affordable than renting, and there are other benefits to homeownership (stability, an inflation hedge, more and different choices in size and location of houses), the impact on homeownership rates will likely be small.

Nevertheless, the effect of these changes may increase, possibly resulting in a slightly lower homeownership rate as more households choose to rent.

Economists at the Federal Reserve Bank of Kansas City take the anxiety level up even another notch, as they play out impacts of tax reform on behavioral economics and housing choices. KC Fed senior economist Jordan Rappaport writes:

Looking beyond 2018, multifamily construction, which requires far less land and only half the labor input per unit as single-family construction, may be able to meet a large portion of pent-up demand as aging baby boomers increasingly downsize into multifamily units. This downsizing appears to be just now getting underway, as the leading edge of the baby boom, those born from 1946 to 1950, recently entered their late sixties. From 2010 to 2015, the share of these boomer households living in multifamily units increased by 1 percentage point, freeing up almost 100,000 single-family homes. The doubling of the standard tax deduction will likely accelerate this shift by significantly lowering the tax penalty of switching from homeownership to renting.

So, here’s a reality as residential developers and builders look at opportunity and risk to their budgets and strategies in 2018 and beyond. Labor, lots, lending, and what Millennials were going to embrace as a cohort-defining housing preference might have been the big challenge areas of yesteryear. Now, it’s more like labor, lots, materials price inflation, and what 55+ adults are going to embrace as their cohort-defining housing preference, given that tax policy may be swinging from a tailwind to a headwind on that front.

The one lever builders have at their disposal to tilt the playing field in their favor is the choice, the ability, and the willingness to drive costs lower to create more value for a new home buyer than he or she or they can get anywhere else in any other housing choice.

So, while the rules of the game are always changing, the way the game is won or lost never does. What weighs heavily as a chronic, intractable, and almost unbearable problem for many builders and developers is–as we speak–regarded as a huge, welcome, and wildly profitable opportunity for a few. Never a dull moment as we peer ahead into 2018.