After the record-setting highs and equally historic lows of the last 36 months, builders must take away one lesson: The housing market is still cyclical. Despite the quotable stylings of D.R. Horton CEO Don Tomnitz and others during the peak of the housing boom, averring that the nation’s large public builders were recession-proof, they proved not to be.

The large public companies, it was argued by the builders as well as by some industry experts and observers, had expanded their product lines to hit more corners of the market, and had broadened their reach through geographic expansion into new and different types of markets, making them impervious to fluctuations in local markets and in the greater economy.

But a quick look at this year’s Builder 100 numbers clearly demonstrates that builders both large and small, and public and private alike, remain subject to industry and economic cycles. Nobody is bigger than the cycle.

The Builder 100 struggled through what everyone is euphemistically calling a “difficult” year, with sales down 23.96 percent nationally. That sales were off was predictable, and that Builder 100 companies also saw a slowdown was no surprise. But Builder 100 companies saw a greater drop in closings (28.16 percent) than the overall market, with the Next 100 (down 32.60 percent) and the 10 largest builders (down 28.50 percent) feeling the biggest losses in closings year-over-year.

In the last housing downturn, which hit its nadir in 1991, Builder 100 companies saw their revenues shrink from $34.2 billion in 1989, to $30.7 billion in 1990, to a low of $24.2 billion in 1991. But the 21.17 percent decrease in total Builder 100 revenue from 1990 to 1991 pales in comparison to the 34.99 percent revenue decline the Builder 100 felt between 2006–2007. (Up to 1990, Builder calculated the Builder 100 based on housing starts, not closings. There is no way to tell how large of a closings decrease the Builder 100 saw at its last trough.)

Overall, the housing market saw new-home starts shrink 14.92 percent from 1.193 million in 1990 to 1.015 million units in 1991. In the current recession, total new-home starts shrank 24.74 percent from 1.80 million in 2006 to 1.35 million in 2007, according to the NAHB.

As Builder celebrates its 30th birthday, it’s time for some historical perspective on the Builder 100, using Builder 100 data and the evolving philosophies of some Builder 100 regulars.

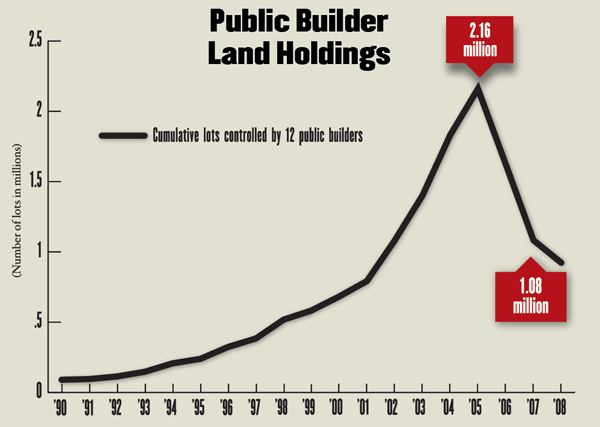

Land Gluttons

Big builders that had seen multiple housing cycles ebb and flow knew to be more cautious buying land during the recent boom. David Weekley, chairman of Houston-based David Weekley Homes, saw builders with large land positions go belly-up during the 1980s in Texas and pushed his company to go slower this time. (See “Last Word,” page 192, for more on Weekley.)

But not everyone took a judicious approach to land acquisition. Builders of all sizes were promoting their long land positions in 2005 and 2006 as major positives, thinking that land would only continue to increase in value, and that they were smart to lock in as much as they could at whatever price they could get before it got even more expensive. It turned out they were buying at the crest of the wave. The land they acquired was worth less than they paid for it almost instantly.

Learn more about markets featured in this article: Dallas, TX.