Home builders might be encouraged by the growing sense of optimism among Americans nearing retirement.

That 55+ customer, whether he or she is looking for an age-targeted or -restricted community or prefers a home in an age-integrated neighborhood, the 55+ age group represents 30% or more of many home building firms’ expectations.

What’s more, with the questions and headwinds–earnings, credit access, college debt, etc.–that have weighed on young adults’ typical embrace of a homeownership track as they form households and families, the 55+ buyer and potential customer have become, along with international buyers, a key contributor to the for-sale housing recovery itself.

So, it’s probably coming as good news to those in the business that both the Conference Board and University of Michigan indicators of consumer confidence among 55+ Americans show sustained gains over the past 12 months.

Wall Street Journal staffer Sarah Chaney has chronicled in two pieces, here and here, the fast-rising consumer sentiment among people 55 and older, with two important side notes.

One, is that younger adults don’t share the shiny outlook their older American survey co-respondents do.

Second, and more important, perhaps, to home builders, is that while the mood indicators are showing full-bore momentum, actual spending among those older consumers has not. Here, Chaney calls on economic expertise for comment:

“(Older Americans) could still have high expectations because the stock market is a part of their equation and home prices are part of their equation,” said Jack Kleinhenz, chief economist for the National Retail Federation. “Their general ability to spend might be good going forward with time, but that doesn’t necessarily mean they’re going to spend it right now.”

And, yet, if that sentiment trajectory is riding Wall Street’s juggernaut, what happens if all doesn’t go as planned with a big corporate and individual tax cut, or if certain regulations at the local level continue suppress business interests, or if new international trade tariffs and fees begin to play out in lower corporate profitability, impacting stock prices?

When it comes down to it, many Americans nearing retirement don’t have a lot of means at their disposal for an expensive move into their “next adventure” post-career home.

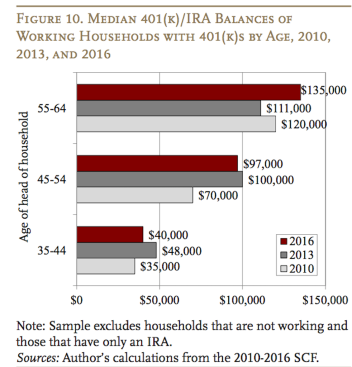

Here’s data, highlighted by New Strategist editorial director Cheryl Russell, that shows average balances among Americans with 401(k) programs nearing retirement: $135,000. That’s it.

Among typical working households with a 401(k)/IRA, the median balance in their plan(s) as they approach retirement is $135,000, according to the Center for Retirement Research’s analysis of the Federal Reserve Board’s 2016 Survey of Consumer Finances. This is not enough to provide much financial support in retirement and is well below what they should have saved over the years, according to Center for Retirement Research calculations.

Now, it’s these Americans who likely reflect the lion’s share of would-be 55+ new-home buyers.

This is why we’re suggesting that D.R Horton’s Freedom brand for 55+, Epcon Communities’ no-muss-no-fuss low-maintainance living for retirees, and Dan Ryan Builders’ Elevate product line represent smart positioning for a large market of would-be 55+ buyers with less wherewithal than typical lifestyle communities for retirees would require.

Call it an “active entry-level” segment, for people with a growing sense of urgency around wanting to be closer to kids and grandchildren, as well as desirous of a simpler, less arduous, more efficient and manageable mode of homeownership.

As 55+ new residential marketing bifurcates between high-margin, well-heeled residents and “the rest,” we sense a very strong market opportunity for developers, designers, engineers, and builders, who can model a profitable higher-volume play for “the rest.”