With ever-more-intense focus in housing these days going to questions, speculation, and initiatives around entry-level, young adult home buyers, Lennar pounced on a prize diametrically opposite that point of focus. It agreed to acquire renascent Florida high-end community developer and builder WCI Communities in a cash and stock transaction valued at $23.50 per WCI share.

The deal is all about timing, and it speaks to a masterful job of optimizing WCI’s value by ceo Keith Bass and his team, as it does to an opportunistic past-mid-cycle stroke of brilliance by Lennar ceo Stuart Miller, president Rick Beckwitt, and their team.

Per a press statement from Lennar this morning, here’s the gist of the deal:

The transaction gives WCI a total equity value of approximately $643 million and an enterprise value of $809 million.

The transaction will be in the form of a merger of WCI and a newly formed Lennar subsidiary. The current expectation is that the merger consideration for each WCI share will be $11.75 in cash and a fraction of a share of Lennar Class A common stock with a value of $11.75, based on the volume weighted average price of Lennar’s Class A common stock on the New York Stock Exchange over the ten trading days preceding the WCI stockholder vote on the merger. However, Lennar has the option of varying the portions of the $23.50 per share merger consideration that will be cash and Lennar stock, including paying the entire merger consideration in cash. The transaction is structured in a manner intended to cause the receipt of Lennar stock as a result of the merger not to be a taxable event for WCI stockholders.

WCI officials note that the sale price represents a 37% premium to WCI’s closing share price yesterday. If the deal concludes following a 35-day “go-shop” period that gives the WCI board leeway to pursue offers from other suitors, it should close by January 2017.

Now some thoughts about the deal–from our vantage point. First, let’s note down the language Lennar’s using in its release as a starting place to talk about motivations, opportunities, challenges, etc. The statement says:

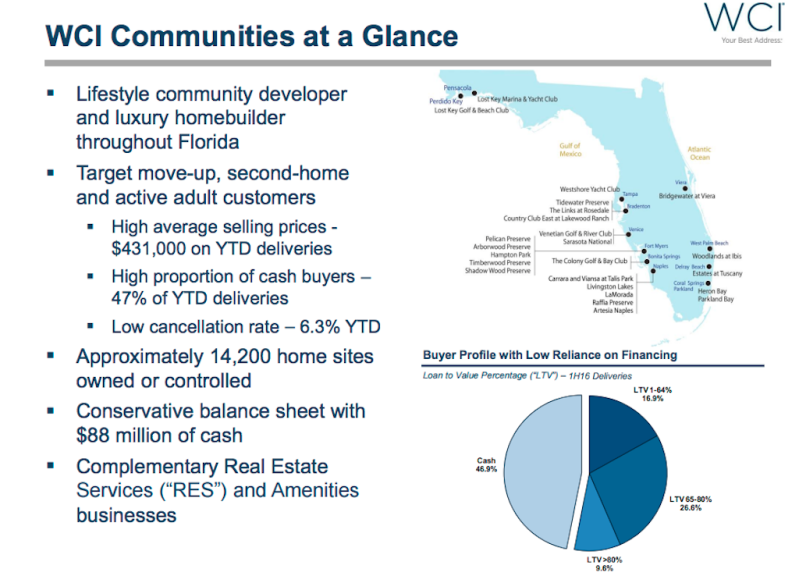

The transaction will combine two of the largest homebuilders in Florida. With a legacy that spans more than 60 years, WCI has established a leading expertise in developing amenity rich, lifestyle master planned communities catering to move-up, active adult and second-home buyers. In the latest 12 months ended June 30, 2016, WCI delivered 1,118 homes with an average sales price of approximately $444,000. The transaction will include a portfolio of owned and controlled land totaling approximately 14,200 homesites, located in most of the highest growth and largest coastal Florida markets.

The deal works on multiple levels for Lennar.

- At average selling prices of almost $100,000 more than Lennar’s current level, WCI gives Lennar a solid new brand tier, as well as a Florida land pipeline in prime, constrained, mostly coastal positions that can stretch well into housing’s next cycle.

- The Florida concentration for the present represents a perfect opportunity to capture operational and administrative efficiencies within a finite geographical footprint, a potentially accelerated integration process.

- The Bonita Springs, Fla.-based WCI community development model and upmarket brand currency may also be one Lennar could port beyond the Florida market; it has had prior exposure in the Northeast and MidAtlantic markets, and may work in other geographies as well, including Texas, California, and the Northwest.

- With WCI, Lennar’s positioning and brand portfolio in residential real estate includes an expansive line of for-rent multifamily, single-family attached, and multiple price-points of single family detached, and now a premium luxury line.

- The WCI line–which includes single-family, condo, and high-rise for-sale communities, is also a powerful learning tool to understand retirees and soon-to-be retirees’ preferences, values, and demands in homes and communities.

For WCI, motivations may include a blend of lessening risk and seizing a moment of opportunity to secure a future for its brand and value generation, with an infusion of cash and resources it could never have achieved as a stand-alone.

- By selling now, WCI spares itself having to continue to replenish its land and lot pipeline as bigger, more well-heeled players continue to crowd into the Florida marketplace competing for the same tracts, bidding up the prices.

- With the sale, WCI investors and the board reduce their exposure to latter cyclical weakening at a moment where its valuation may have peaked.

Institutional investors like such a deal, because it sucks excess overhead cost and capacity out of the system and consolidates more clout with fewer larger players. Lennar’s acquisition strategy for the past several years has been far more conservative than No. 1 home builder D.R. Horton, which has mounted a huge blitz in the Atlanta market over the past couple of years with several purchases there.

But Lennar’s real estate knowledge and strategy–be it residential for-sale, for-rent, financial assets, and commercial–is among best of breed. So its timing on the WCI buy, while all eyes are fixed on what’s going to happen next with entry-level home buyers and builders, is as canny as it may seem counter-intuitive.