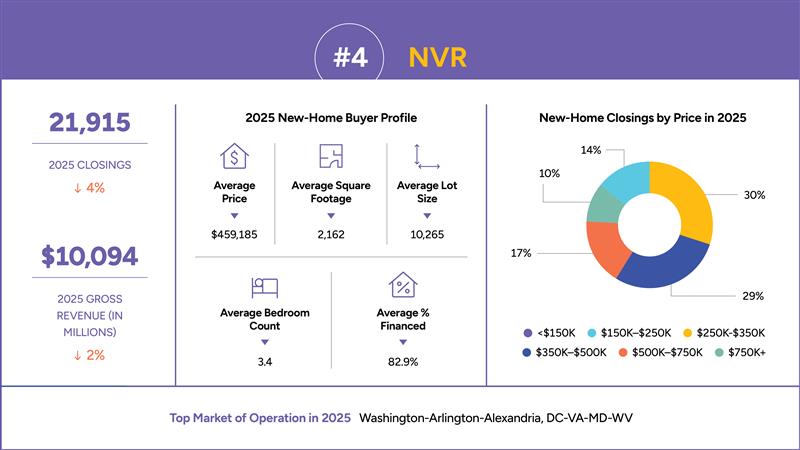

With an increasing number of public builders shifting toward a land-light, asset-light approach, one builder’s name consistently appears as the aspirational target: NVR. The Reston, Virginia-based builder has been described as the “standard of consistency” and a company with the “holy grail” of business models by investors and analysts.

NVR does not generally engage in land development, instead acquiring finished building lots from third-party developers. In its SEC statement, NVR said the approach “avoids the financial requirements and risks associated with direct land ownership and land development.” At the end of the 2025 fiscal year, NVR controlled approximately 169,250 lots under fixed price lot purchase agreements with third parties while it owned land that is expected to be developed into approximately 2,300 finished lots.

Zonda’s chief advisory officer Tim Sullivan called NVR the “poster child” for land-light operating models. The land-light model has become more prevalent as builders favor the flexibility to allocate their own capital elsewhere and remove land, an asset perceived as risky and less favorable by Wall Street, from their balance sheets. As proof of the model’s value to investors, NVR’s stock price, which has held a value above $4,000 per share since 2021 and peaked at over $9,900 per share in 2024, far outpaces those of its public peers.

NVR serves buyers in 37 markets across 16 states and Washington, D.C. More than 70% of NVR’s closings are from its Mid-Atlantic (Maryland, Virginia, West Virginia, Delaware, and Washington, D.C.) and Southeast (North Carolina, South Carolina, Tennessee, Florida, Georgia, and Kentucky) regions.