I’ve been slow to comment on artificial intelligence (AI) in housing/building products, but we are now at a stage where the implications are becoming clearer, and the industry is approaching a set of underappreciated decisions that will matter over the next three years.

Adoption Today, Shifting Over Next Six Months

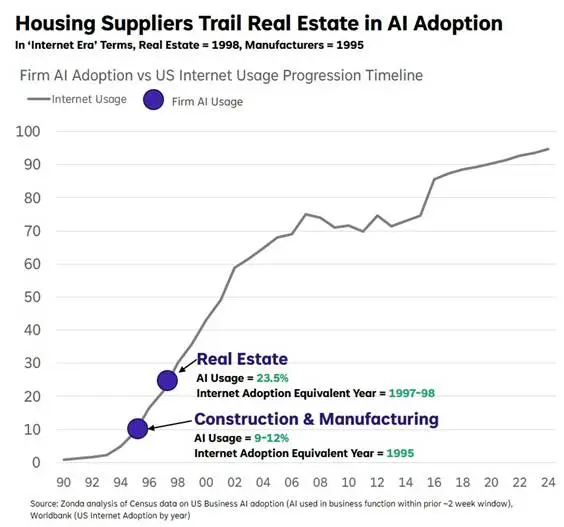

In a nutshell, AI adoption in real estate is two times higher than in ‘inputs to housing’ like building products or construction, even lower in distribution. Adoption across both housing and upstream inputs is likely to accelerate rapidly over the next six to 12 months.

To put AI adoption in perspective, real estate firms use AI at roughly the same rate that U.S. households used the internet in 1998. Upstream suppliers are closer to 1995. For those that remember that period (1995-2001), the gap in capability, and business impact, was enormous, with most downstream effects still ahead.

Census data reveals that about one out of four real estate professionals use AI in some official corporate function. Employee usage within those firms is often higher, though using ChatGPT to make social media graphics is not the same as driving corporate productivity gains.

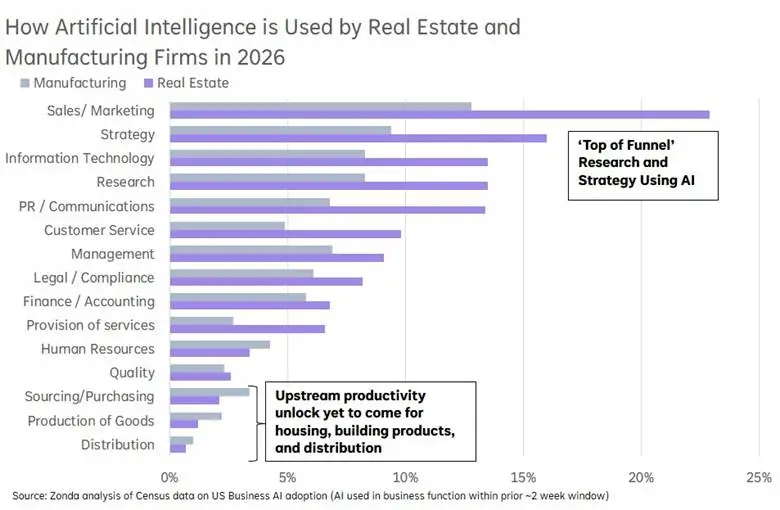

More important is how AI is being used. Today, usage is concentrated in marketing/strategy, and legal review. The real productivity unlock of using AI in actual output, upstream distribution, and manufacturing of products, still has extremely low adoption, 2% to 3% for production and 1% for distribution.

Where penetration changes over the next six to 24 months will be corporate deployment of AI in upstream production, distribution, sourcing, and core operations. Some companies are already experimenting. As they do, we can expect their management to face several surprising changes.

How AI Progresses Versus Human Judgement

Nearly 30 years ago, IBM’s Deep Blue defeated Garry Kasparov, Russian chess grandmaster. At the time, some pundits wondered if ‘chess is dead,’ because if machines can always win, why watch or play?

Fast forward to today, AI chess engines can defeat any human, yet chess popularity is higher than ever. Humans still want to watch humans compete, but the AI aids in the analysis and interpretation.

What’s more: AI chess plays differently than humans do. AI will make risky-looking moves that feel wrong to humans initially, sacrificing material for advantages that only become clear many moves later.

AI didn’t just ‘brute force’ human-style methods, it identified moves that seemed wrong to humans, but were ultimately superior moves. As a result, AI dramatically increased creativity in chess, such as new openings, new definitions of how to value pieces, etc.

Translating the Same Progression to Housing and Building Products

Up to this point, housing and building product companies generally make pricing and research decisions using a very ‘human’ approach. Some would argue several years behind other industries like CPG because of weaker data infrastructure. That all becomes more complex with AI.

As AI systems are brought online to optimizing decisions, housing and building product leaders will face suggestions that fundamentally look ‘wrong,’ but could be correct for reasons that are not yet perceived.

Examples:

- Pricing a freestanding bath to maximize spending elsewhere in the home

- What home features to place on a corner lot to maximize total transaction value

- Cross-selling pro contractors via e-commerce in ways that feel unintuitive

The companies best positioned to use these insights will have superior visibility to decision-level data, such as pricing across competition categories, brands, and seemingly unrelated categories. As AI adoption expands, the creativity of proposed solutions will increase. Many of the best answers might initially feel wrong, some will be actually wrong, but a turning point will be reached where some of the ‘feels wrong’ answers will be proven right at scale.

The AI ‘Decision Squeeze’ Ahead

Social media is full of examples poking fun at generative AI mistakes, factual inaccuracies, hallucinations, and obviously wrong conclusions. The ‘eager intern’ behavior of generative AI, which sounds confident but doesn’t recognize where the logic breaks.

Making fun of flaws in AI analysis today feels a bit like making fun of the Wright Brothers flyer because it looked superficially impractical while failing to perceive what it meant for the future of air travel. Housing executives will face a timing decision: the difficult question ‘when to step on the aircraft’ but not miss the opportunity.

The challenge is that obvious mistakes by AI today will blur rapidly into transformational analysis tomorrow. Insight that still looks wrong superficially, like AI chess moves, but are directionally correct.

At some point soon, plausibly within the next three years, housing suppliers will face a decision point where AI deployment on major business decisions like pricing, production, and distribution will begin producing recommendations that look wrong, but may be economically correct at scale. How housing leaders navigate that blurred decision point is the next real hurdle for AI productivity unlock. Profits will accrue to whomever identifies that turning point correctly.

Knock-On Impact From AI Advances in the U.S. Economy and Other Industries

One last underappreciated issue: there is a case that housing may be one of the most underestimated beneficiaries of AI adoption across other sectors in the broader economy.

There is an emerging narrative among investors today whether remodeling and housing is ‘permanently broken.’ The fear stems from a switch in tone on housing ‘undersupply versus oversupply’ debate, with longer term fears of slowing demographics significantly slowing the need for new housing. Add to that bearish picture the pressure of ‘higher for longer’ interest rates, exacerbated by persistent inflation and fiscal concern.

Those are real concerns. That said, both look more constructive when viewed through the lens of a world undergoing AI adoption:

- AI will have a positive effect on U.S. productivity and growth, but we don’t know how much. When it does, productivity growth will tend to drive costs lower, and bias interest rates lower versus whatever non-AI baseline scenario you believe is correct. Current forecasts, from Congressional Budget Office and others, assume minimal or zero productivity improvement, which is probably an understatement.

- AI will have a positive, non-zero effect on longevity and healthcare, which will drive knock-on housing demand in some fashion. We don’t know precisely how much, but current long-term demographic forecasts from the Census generally largely assume pre-AI longevity trends. Again likely understating the positive impact.

What’s key here is that most industry participants believe that AI will benefit the economy via productivity growth, improved healthcare, faster services, and other improvements. However, the underlying calculations that are being used as the basis for long-term housing analysis have zero of the above explicitly built in. We just haven’t seen it yet, but the improved fundamentals from AI to the industry are almost certainly still ahead.

If you believe that AI will drive any improvement in productivity or healthcare/longevity, you should become more bullish on long-term housing than the current narrative. We just don’t know by how much. I’ll take the over on that.

What an exciting time for housing.

*The timing progression of AI in chess is an intriguing analogy for other industries. Real estate adoption of AI is roughly where U.S. internet adoption was in 1998, while construction and manufacturing firms are closer to 1995. Interestingly, Garry Kasparov lost his first match to Deep Blue in 1997 versus a computer with custom hardware, extensive human tuning, and a machine that was expensive to own or replicate. Within 10 years, top chess engines exceeded all humans by a wide margin, and a laptop could beat any human in a match. Roughly 20 years after Kasparov lost to Deep Blue, AlphaZero began playing differently than humans and redefining what ‘perfect chess’ looked like. AI is advancing faster than prior technology cycles. If progress scales at 1.4 to 2 times pace of internet adoption, it might suggest business/logistics/manufacturing decisions could be three to seven years away from ‘human level’ support, with AI reframing decisions seven to 10 years later. Speculative, but context worth considering.

**Productivity gains from AI are unknown but plausibly have a larger effect on overall demand than the industry currently has modeled. Researchers at the Dallas Federal Reserve suggested that 0.3% growth in productivity could be reasonable. However, even slower productivity growth would likely result in outsized benefit to residential construction. One intriguing analysis from researchers at Stanford suggested a 0.1% growth in productivity would raise the fundamental value of U.S. Treasury’s by $1.3 trillion (4% of market value), implying at 71 basis point decline in long term Treasury yields simply from 0.1% of AI driven productivity growth. Other research from economists at Yale suggested 20% productivity growth in the U.S. over the next decade. Whether these projections are correct remain to be seen, but the industry currently is modeling near-zero impact, which we suspect is low. See Kung, H., Lustig, H., & Paron, J. (2026, May 14). U.S. Treasury investors are long in AI, Merali, A. (2025, December 25). Scaling laws for economic productivity: Experimental evidence in LLM-assisted consulting, data analyst, and management tasks.

Read the earlier iterations of this six-part series below. The insights in this article were taken from a more detailed review in Zonda’s Building Products Outlook.

-

Low-Key Luxury: An Alternative Indicator of Housing’s Next Phase

Part four of six issues housing and building product leaders need to know in 2026.

-

From Cars to Housing: A Familiar Industry Shift Reemerges

Part three of six issues housing and building product leaders need to consider in 2026.

-

E-Commerce and ‘Workflow Capture’ in Housing Supply

Issue two of six key issues housing and building product leaders need to consider in 2026.

-

The Great Reset in Building Product Pricing

Issue one of six key issues housing and building product leaders need to consider in 2026.