Amid the closure of the Strait of Hormuz, shifting tariffs, and demand uncertainty, housing suppliers face a conundrum. Manufacturers have notified customers of sequential price increases, typically in the 5% to 8% range, but actually pushing those increases through the channel is far more difficult.

As the duration of the conflict extends, manufacturers are likely facing multiple future waves of upstream cost pressure, beyond the initial increases already recognized. As the industry learned in 2021, supply chains become significantly more troublesome the longer upstream disruptions persist. Appliances, windows, and other building products require coordinated inputs across global sources, which increasingly breaks down amid longer durations of geopolitical instability.

Zonda analysis suggests that near-term, knock-on effects, higher gas prices, weakening consumer sentiment, and incremental project deferrals, has the potential to incrementally drive a negative 200 to 700 basis point headwind to product demand if knock-on effects from the conflict last through Q3. As a result, manufacturers are trying to balance announced price increases against the very real risk of losing share to lower-cost competitors eager to gain shelf space with retailers and builders.

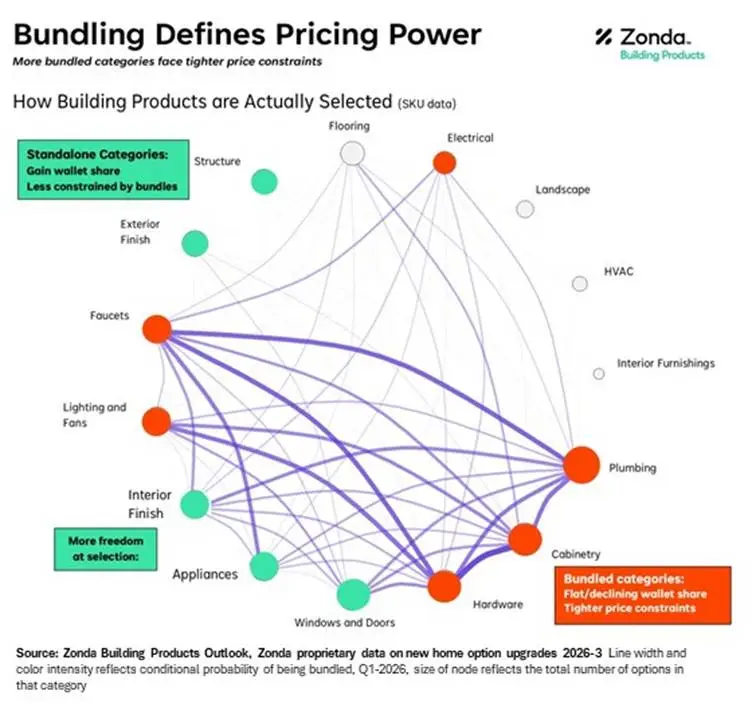

Complicating matters further, most manufacturers are set up to make poorly informed pricing decisions. Pricing is typically benchmarked within categories (e.g., faucets versus faucets, appliances versus appliances). However, consumers make decisions within a broader project budget, typically involving products whose pricing—and elasticity—are not considered. A homebuyer who allocates more to flooring has less to spend on faucets, and vice versa. Some builders offer ‘bundled’ pricing via incentives on entire packages of home upgrades, which is left out of manufacturing pricing decisions.

This imbalance creates systematic pricing errors. Elasticity assumptions fail because manufacturers lack visibility into the broader “bundle” of spending. Brand “A” may believe it understands its pricing power, yet lacks insight into how competing basket of categories are influencing the final purchase decision. As a result, the industry is facing a setup of numerous pricing missteps, which we suspect will drive subsequent shifts in market share.

So who gains in this environment? Companies with exceptional visibility across competing categories of consumer spending, even those outside their core product. Very few firms have this capability, likely fewer than 10, who are fundamentally better positioned to navigate the pricing/elasticity decisions because of simply having the broader picture of where substitution really occurs.

As a result, 2026 has the potential to become a catalyst year, driving accelerated market share gains and losses, increased consolidation, and widening margin differences driven by capability gaps. This would mirror the post-stagflation period of the late 1970s and early 1980s, when deferred demand eventually rebounded, and structurally advantaged firms emerged, including the founding of Home Depot and subsequent expansion during recovery phase.

The lesson for us: manufacturers don’t ultimately dictate end prices for the industry, markets do. In volatile pricing environments like the one emerging in 2026, market share gains are likely to be sticky and strategically important ahead of the next upcycle.

The insights in this article were taken from a more detailed review in Zonda’s Building Products Outlook.