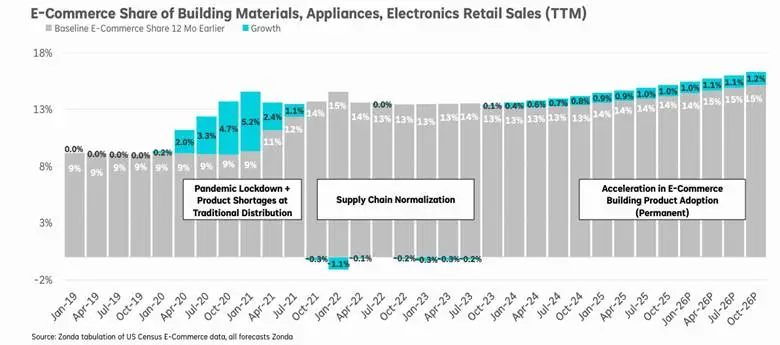

The role of e-commerce within housing supply is shifting, with progression looking a bit more like a structural inflection, beyond just “growth.” Digital share of building products accelerated 100 basis points in 2025 and is on track to outpace overall industry growth by roughly 8% in 2026, which implies an acceleration in 2026 (an 125–basis point increase) of market share growth.

That pace of e-commerce penetration growth is unprecedented in the industry outside of COVID, and rare in non-media categories. What’s changing now is the durability: digital purchases are embedding into project workflows, not just limited to contractor price checks or one‑off special orders.

To be clear, in-person purchases are still absolutely preferred by contractors, and for good reason. Personal relationships, dependability, and the service from quality sales people are central to driving sales. Eighty percent of pro contractors keep digital spend less than 25% of their overall wallet, and will probably continue to do so. But once the in-person relationship is made, the annuity of future ‘workflow purchases,’ and related knock-on purchases are renewing via e-commerce.

The data suggests building products e-commerce can probably reach 20% to 25% of overall revenue over time. Roughly one‑third of largest pro contractors now rely on digital channels for routine, repeat purchases, capturing 20% to 25% of their spend. These aren’t sporadic buys; they’re embedded in workflows and drive attached ‘knock-on’ purchases across channels.

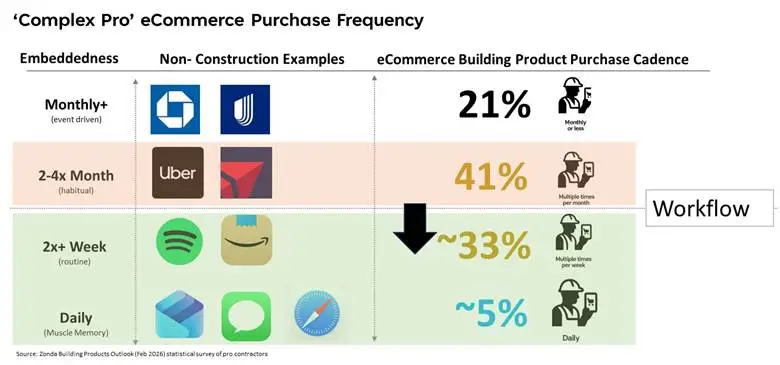

What striking is the frequency of these e-commerce interactions. Roughly 38% of the largest ‘complex pro’ contractors report using digital tools to purchase multiple times per week, with 5% purchasing daily. Consider what that means: Daily interaction with apps versus monthly is the difference between paying your bills online versus checking email or social media. Daily apps become automatic to human personal routine, perhaps even muscle memory. Contractors are shifting from occasionally ‘special ordering’ online, to using e-commerce as a psychological process in their workflow.

To make things more intriguing, the fastest digital shift seems to be happening among the ‘complex pro,’ who has been the focus of market share growth by suppliers over the past two years. Our data shows these ‘complex’ buyers purchase online two times more often, with larger baskets, broader platform usage, and higher mobile engagement. Digital procurement becoming less of a backup plan, and more of how contractors operate workflow, at least for part of their basket.

In the last month, QXO announced acquisition of TopBuild for $17 billion, and released an in-depth Q&A on various strategies underway. Part two of QXO’s technology assessment focuses on cross-selling and improving stickiness of customers via digital strategy. Similarly, Home Depot/SRS is hiring and structuring teams specifically focused on digital workflow, as well as other leaders in the industry. It’s not accidental that jobsite visibility, AI, and purchase workflow are converging together. Jobsite pricing is one of the least visible—and probably mispriced—part of the industry, and getting closer to contractor project management offers opportunities at unlocking value, including better visibility into ‘pro veto’ of major brands versus private label.

A personal anecdote:

Some of you know I enjoy woodworking, although my skill is below people who do so professionally. A few months ago, I walked into one of the largest ‘pro-heavy’ power tool stores looking for an obscure tool accessory that I needed for a last-minute project for a friend. The part I needed was out of stock, and backordered, and couldn’t be delivered online. The in-person experience was exceptional. This company offered to fabricate a custom tool the same day to ‘get the job done,’ if needed immediately. Incredible service, which is what pro contractors love about in-person purchases. Here’s the catch: this ‘in-person’ company sells far more high end tools via e-commerce than they ever sell in person, and is a leader in the category. Winning the pro digital enables in-person flexibility.

The essence is: e-commerce and digital role in housing supply is shifting, and the lines between well-executed in-person versus e-commerce pro purchases are blurring. In 1974, stagflation—and subsequent Volker-era deferral—drove what was known as the ‘lumber recession,’ which was characterized by margin erosion in housing supply, along with consolidation in housing suppliers. When inflation finally eased in early-mid 1980s, the housing market was left with a pent-up wave of moves and home improvements, which ultimately led to the DIY surge of 1984 to 1985, when Home Depot began to grow at scale. The lesson is that strategic shifts during the current deferral environment are likely to be strategically critical when the industry stabilizes. Pay attention to the shifting role of digital and ‘workflow capture’ within construction. Something seems to be shifting.

To read the first iteration of this six-part series, click here. The insights in this article were taken from a more detailed review in Zonda’s Building Products Outlook.