Fact:Carl Mulac, a veteran of public home building companies for almost 30 years, has picked exactly now to start his own Phoenix-area private home building firm, and he’s planning to close on about 60 homes in 2010, his first year of operations. Fact: He’s got money behind him in the form of a private equity investor and a $3 million Mutual of Omaha construction lending facility. And he’s got a honey of a land deal stretching out ahead of him in the form of a pennies-on-the-dollar master-planned-community tract he knows like the back of his hand.

The question in a residential real estate environment and a macroeconomic climate still rife with uncertainties, twists, conflicting signals, and reasonable doubts, not to mention unknowable random setbacks, must be, “Why now?”

Even the more sanguine housing forecasts peg home prices nationally to cave another 6 percent or 7 percent from the current 35 percent off of 2007’s peak; and, somehow, either in a nuclear blast or in a water-torture fashion, as many as 7 million more homes must clear through foreclosure in the next few years. Add to that anxieties over what happens as the government policy punch bowl helping housing with tax credits, interest rate support, and foreclosure suppression gets taken away, and that nobody has much of a clue about how to set in motion a 7-million-job creation swing from minus to plus, and you’ve got real reason to question timing here.

Mulac’s answer to the timing question, and he’s sticking to it, is simply this:

“I am a home builder, that’s why.” Saying “I’m a home builder” at a Wall Street investor conference can cause the better part of his audience to head to the buffet table—and it has. One recent investor presentation of his business plan got off to a shaky start the minute he stated, “My name is Carl Mulac, and I’m starting a home building company.” To which one of the young finance and investment whizzes in the room blurted anonymously, “You’re crazy!” Still, the same words, “I’m a home builder,” professed in a roomful of private home building operators, explain the nature, the behavior, the skill set, and the conviction—running the gamut from “I can’t help it” to “I know what I’m doing here,” plus everything in between.

Now, he’s just got to prove it.

Back at the office It would be an injustice to the Carl Mulac story to overplay the metaphor and magic, but it’s sorely tempting. There he is in Phoenix, his new company rising out of scorched earth and ashes, generating orders of about 12 or more a month. That is quite a leap, some would say backward, from the prototypical division president of a Top 15 public home building enterprise that he was, churning out 2,500 closings a year and taking in more than $1 billion in revenue from plush business offices, with a staff of 300 and a credit card limit of next to infinity for lot purchases.

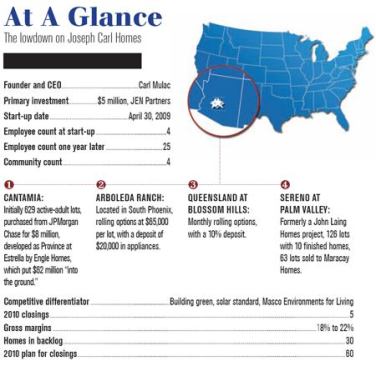

Now, his company office bears a sharp resemblance to the casita in back of his Phoenix home. Check that, that is the company headquarters, unless you want to call headquarters Mulac’s trusty SUV, where he spends so much time doing the 90-minute to two-hour drives from one outpost in the Phoenix metro to another, connecting with the brain trust of his yearling enterprise, which has swelled to 25 people, 11 of them in sales.

The emergence in late 2009 of a brand-new name in home building—Joseph Carl Homes, which actually draws on Mulac’s given and middle names—has a metaphoric ring to it, particularly after three years of private home builder collapses that rival the Federal Deposit Insurance Corp.’s growing list of bank failures. Some analysts and home building veterans predict that if capital costs remain as prohibitive as they are now—and there’s no compelling reason to believe they won’t—as many as four out of five private home building operations in existence in 2006 will have “exited” from the markets they’ve competed in.

Some, no doubt, will be back, without the debt. Dozens of newly formed and reconstituted home building operators have already popped up in a de-leveraging real estate economy, and many more are readying the shingle they’ll hang out when the moment is right and the money is there.

Timing the cycle Which brings us to Reuben Leibowitz, whose JEN Partners initially committed $5 million in equity in 2009 to shepherd Mulac’s fledgling outfit and has since expanded the commitment to $7 million. Leibowitz “retired” after 22 years of running a number of investment sectors at Warburg Pincus, having ridden the wheel of residential real estate fortune into, out of, and back into the money since the late 1980s.

“I never lost money on somebody else’s mistake,” says Leibowitz, who bet and won big-time on Tony Mon at Pacific Greystone in the early 1990s and, notably, fell short of a similarly favorable outcome with a $65 million investment in Wall Homes in 2005 and 2006. Pacific Greystone is the model in Leibowitz’s mind as the one to shoot for—invest when the market bottoms, build on management talent, size operations, strategize for strength, and exit via a public option (either through an IPO or a sale to a public company, or both). In fact, Pacific Greystone, led by Mon, followed just such a course, ultimately selling to Lennar. Wall Homes, however, failed to survive the convulsion.

“You need a strong team, and you need a good cycle,” says Leibowitz. “We had the strong management team with Steve Wall, but you need to get in at the bottom of the cycle. That time, we didn’t, and we thought we could beat the cycle in Texas because it held up at first.” By spring 2008, the banks were ready to shut Wall down, and Leibowitz conceded he’d mistimed his investment. It was a $65 million lesson learned.

Learn more about markets featured in this article: Phoenix, AZ.