I work with two of housing’s best and brightest economists–Mark Boud, senior vp at Real Estate Economics/Metrostudy, and Brad Hunter, Metrostudy chief economist and director of consulting. It’s humbling.

I tell them what I hear from home builders about what they’re doing, what they expect, and what scares them. Mark and Brad listen, nod, smile, and dip quietly into their own deep reserves of patience and tolerance as they piece together a response, an explanation.

I tell them builders I talk to express a bi-polar outlook on their own businesses. They worry most about access to the resources–money, developed lots, and labor–to meet the need they’ve identified in their operating arena(s).

They also worry about consumer confidence.

Indeed, broader economy observers, like Nobel Prize winner Robert Shiller, here and Wealth of Common Sense poster Ben Carlson, here, have begun to cite fear, loss aversion, and panic as behavior drivers that trump rational, sensible, thoughtful response to supply and demand conditions.

Wall Street gyrations, China’s convulsions, the energy sector glut, a global undercurrent of terror, a sharply polarized election year, and, now, shaky corporate earnings and outlooks have snowballed into a big confidence downer.

The question is, what can offset, neutralize, or reverse the very important mood and sentiment “grease” for the economy’s big wheels?

Builders come face to face with consumers–whether they work on Wall Street, or Main Street, or the local factories–every day and every way. They pick up the vibe, and they tend to know pretty well whether they’re “pushing on a string” when they’re pumping new work-in-process units into their respective neighborhoods, versus, pulling them elegantly through their businesses.

Both Mark and Brad look at 2016 as a step-up year in housing’s recovery, as they look at economic fundamentals and new residential development and construction’s key building blocks–vacant developed lots in the pipeline and their pace of absorption by builders, and, ultimately home buyers.

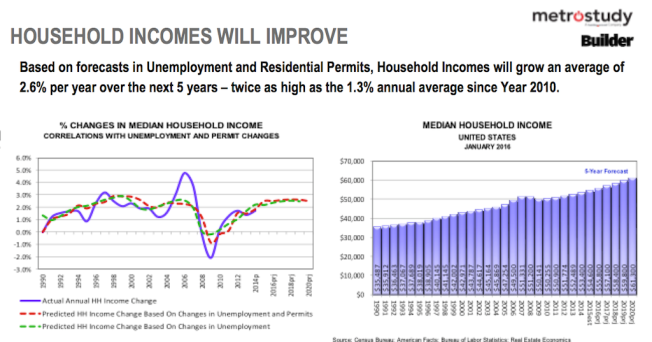

Both of my colleagues look at improved broad economic conditions, including the basics that drive corporate results, income growth, household formations, and consumer spending. For instance, here’s a look at Mark Boud’s sense of what will happen to household incomes over the next five years.

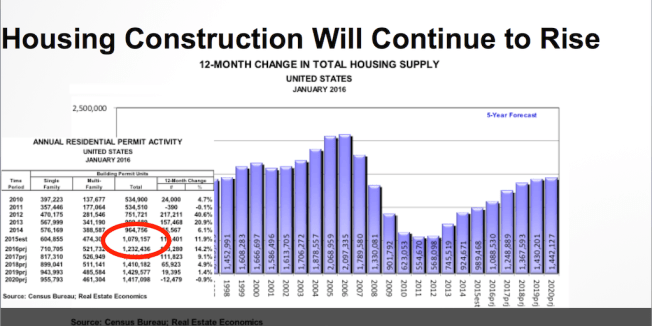

Here’s Mark’s outlook on permit growth, suggesting a 14.2% year-on-year pick up in single-family, multi-family and manufactured housing permits from 2015 to 2016.

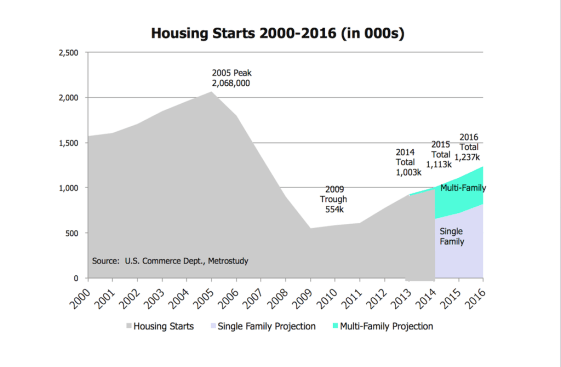

Here, Metrostudy’s Hunter shares an outlook for an 11% increase in single- and multifamily housing starts, 2015 to 2016, given a scenario that doesn’t include a Black Swan hit to consumer confidence, jobs and household formations.

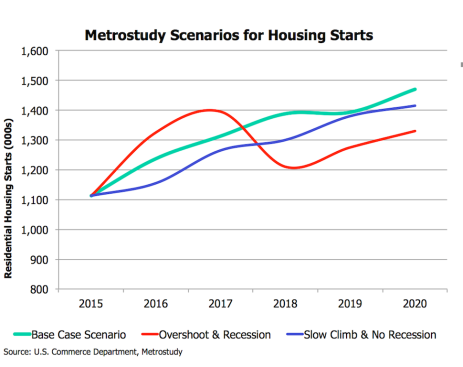

Here’s Hunter’s baseline-plus-two cases–one a “slow climb-no recession” outlook and the other an “overshoot-recession” forecast.

Clearly, if the worst-case scenario comes about, we’ll see home builder casualties, especially since many are front-loading the next 24 to 36 months with capital investment risk that assumes jobs, households, and income growth will fuel demand.

It’s precisely this market environment that marks a definitive end to average performance on the part of home builder operators. Either you’re excelling at the workmanlike low-margin, higher volume program and process that can pull people out of spiraling rentals, or you’ve got clout, “cred” and a high-margin program meeting the thinner stream of move-up and second-time move-up communities.

The ones who rely on a tide to lift all ships may find themselves tugged under. It’s right to worry. Until traffic, conversions, low-cans, and closings prove they can propel housing into its erstwhile role as the engine of the economy, it’s right to worry in spite of the fundamentals.