The oldest members of the Millennial generation are entering their mid-30s, and ideally also achieving financial stability. However, student debt are at historic highs, and a Millennial’s median earnings are 20% lower than their Baby Boomer parents’. It’s only recently that the 18-35 age bracket has dominated the home buying sphere, making up the largest share of new home buyers in the last few months.

Still, with median home prices climbing higher and a shortage of starter-home stock, many Millennials remain renters, or have another living situation. For some, home ownership may not be a reality for decades to come, if at all.

“At ABODO Apartments, we know that Millennials are often labeled as the renter generation, but we wanted to uncover whether or not this statement is entirely accurate,” says Sam Radbil, Sr. Communications Manager with ABODO Apartments. “Maybe Millennials are actually starting to buy homes? Well, if they are, where this happening the most? To find out, we analyzed U.S. Census data to uncover the cities with the highest percentage of Millennial owners and what it costs for them to own a home.” ABODO has also examined how Millennial home ownership rates have changed over time, and what it may take for them to save up for a down payment.

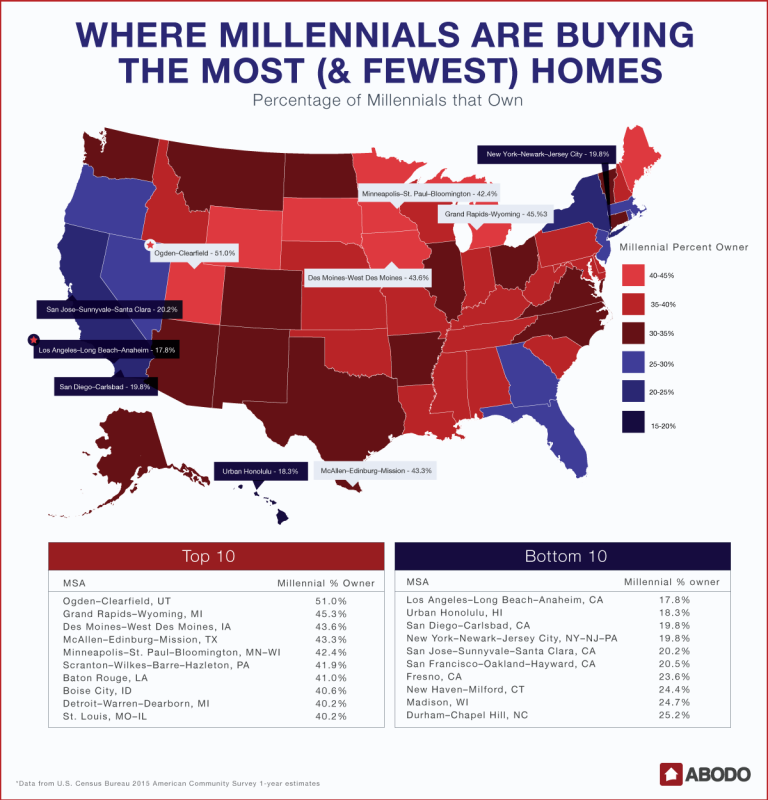

Where Are Millennials Buying the Most Homes?

The national Millennial home ownership rate is 32.1%, but some metropolitan statistical areas (MSAs) have much higher – or much lower – Millennial ownership rates. In Ogden-Clearfield, Utah, a whopping 51% of Millennials are home owners, outstripping the rest of the state by 10%. It is the only MSA where more than half of Millennials own homes – the “second place” market, Grand Rapids-Wyoming, Mich., sports 45.3% Millennial home ownership. All of the top five MSAs for home ownership are small to mid-size cities in the Midwest and South.

Conversely, the MSAs where Millennials are least likely to own homes are expensive coastal cities, where home prices are prohibitively high, or college towns, where a majority of the Millennial population are students and generally live in either apartments or dorms. Los Angeles-Long Beach-Anaheim, Calif. has the lowest Millennial home ownership rate at 17.8%, followed by Urban Honolulu, Hawaii at 18.3% and both the San Diego-Carlsbad and New York-Newark-Jersey City MSAs at 19.8%. ABODO notes that high-density urban cores generally have higher rental rates, as do college towns.

National and local home ownership rates among young adults have been on the decline since 2005, when Generation X adults ages 18-35 began buying homes at a slower rate. Between 2005 and 2015, the national home ownership rate in this age bracket fell from 39.5% to 32.1%. San Jose-Sunnyvale-Santa Clara’s young adult home ownership has fallen by 34.8% in the past ten years, followed by New Haven-Milford, Conn. With a 34.5% decrease.

Out of the top 100 MSAs in the nation, only two experienced increases in young adult home ownership – Scranton-Wilkes-Barre-Hazleton, Penn. at 12.1% and Buffalo-Cheektowaga-Niagra Falls, N.Y., at 3.8%.

When Will Millennials Afford a Home?

The value of the average Millennial’s home compared to the average home value in a given MSA also varies widely by location. Out of the top ten MSAs for equitable home value, ABODO notes that eight are located in the South and Midwest. The only two MSAs where Millennial home values exceed the area average are El Paso, Texas at 104.6% ($142,854) and Bakersfield, Calif. ($245,335.)

Tuscon, Ariz. sports the greatest value disparity among the MSAs examined. At $150,938, the average value of a Millennial’s home is 68.8% of the MSA’s average home value. Other top-ten cities include Urban Honolulu, Hawaii (70.5%) and San Jose-Sunnyvale-Santa Clara (73%). San Jose’s hefty $737,077 Millennial average may be difficult to attain “even [for] high earners in Silicon Valley”, ABODO notes.

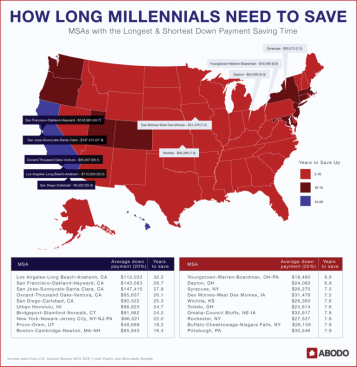

Even though trends point to younger buyers seeking out more affordable homes, their down payments may still take a decade or more to save up for on the average salary in a given area. If you assume that a given Millennial making the median income saves 15% of their income each year, then they would need an average of 15.6 years to save up for a down payment.

In California’s most expensive MSAs, saving up for a down payment on the area’s median young adult salary could take a third of a lifetime. Los Angeles-Long Beach-Anaheim tops the list – in order to save up for the average 20% down payment of $112,033, a Millennial would need to save 15% of the median salary for 32.2 years. California also rounds out the rest of the top five with San Francisco (28.7 years), San Jose (27.9 years), Oxnard (26.1 years) and San Diego (25.3 years).

Youngstown-Warren-Boardman, OH-PA sports the shortest saving time at 6.9 years for a $19,480 down payment. Dayton, Ohio, Syracuse, and Des Moines also have saving times in the range of seven to eight years.

In order to speed up this process, ABODO recommends that Millennials who plan to one day own a home take rent expenses out of the equation by living at home, or else finding other ways to save more than 15% of their salary per year.