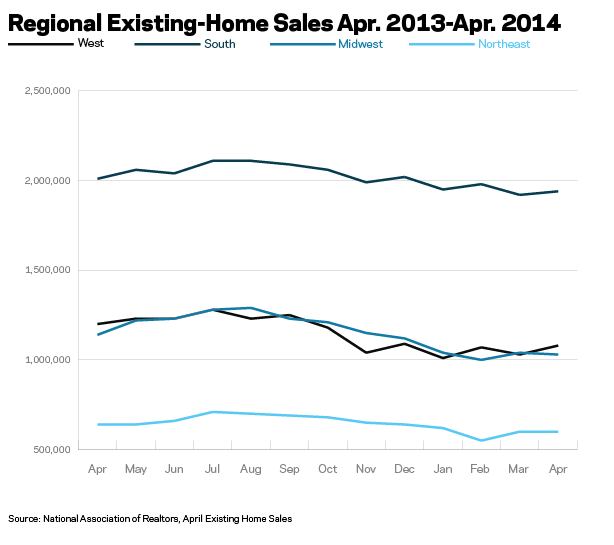

With all of the misdirected hand-wringing over the alleged stalling of the housing rebound in 2014, you would have thought that economists and analysts would have expected another slight decline in existing home sales to be reported by the National Association of Realtors (NAR) this morning. But instead they were expecting a 2 percent increase to an annualized rate of 4.69 million from the 4.59 million initially reported in March. The actual report from NAR set the initial April reading at 4.65 million, an increase of 1.3 percent from the unrevised March rate of 4.59 million.

For several months now I’ve been trying to highlight the fact that the total volumes are not nearly as important as the composition of what is being sold and who is buying. You can fret all you want about the total volumes being up or down, but the reality is that the residential real estate market is getting healthier and healthier each month. The health is reflected in the share of non-distressed, normal transactions continuing to rise; more and more consumers, not investors, are buying; and prices are remaining firm amidst continued demand relative to limited supplies.

Leveraging the deed level data we track from around the country, this is what we see: the share of REO sales among existing home sales decreased 23.5 percent from 16 percent in Q1 to 12 percent in April. The foreclosure share also decreased with a drop of 37 percent from 14 percent to 9 percent. The share of regular resales (non-distressed transactions) grew 13 percent from 69 percent to 79 percent. Comparing April 2014 with April 2013, the REO share fell 19 percent from 15 percent to 12 percent while the foreclosure share again declined from 14 percent to 9 percent. The regular resale share rose 11.5 percent, a jump from 70 percent to 79 percent.

Meanwhile, investor activity continues to decline, with the investor share down almost 10 percent in April from Q1 percent quarter-over-quarter. Why is this a good thing? Investors drove up pricing last year, and investors don’t create the same economic impact in home improvement that regular buyers do.

Pricing is a key lagging indicator reflecting that conditions are improving and not deteriorating. According to the NAR release, the median existing home price in April was $201,700, 5.2 percent up over last year. Supporting continued price appreciation is the low level of supply, which remains below normal at 5.9 months of supply.

Bottom line—today’s report on existing home sales combined with our detailed view of what’s selling and who’s buying supports the informed perspective that residential real estate is getting stronger as the year progresses. These conditions set the table for gains in new home sales, about which we will get the initial April reading tomorrow. Expect better numbers than last month.

The full release and data is available from the National Association of Realtors here.