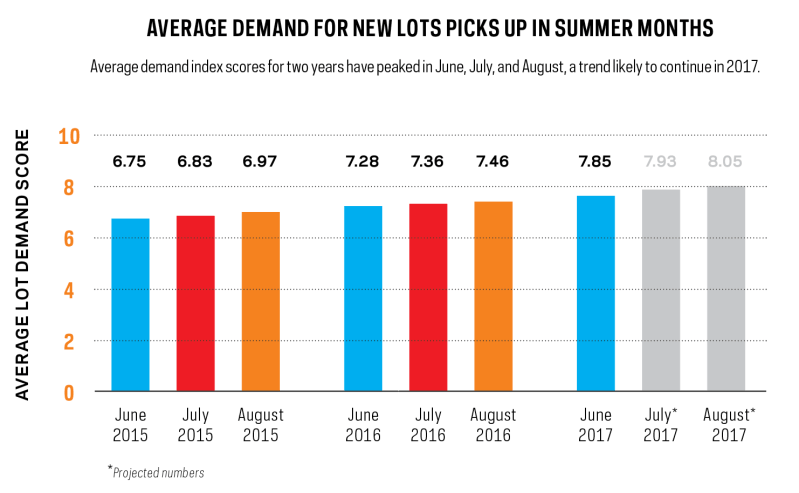

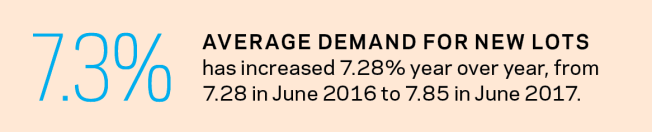

Builders are looking to secure land for 2018, now that spring selling season is over. Average demand for new lots across Metrostudy’s 36 markets peaked in June, July, and August the past two years. While some builders look to acquisitions in order to secure lots—like D.R. Horton’s acquisition of publicly held mixed-use developer Forestar Group in June, which landed it roughly 9,700 lots in 14 U.S. markets—builders in other markets with tight lot inventory must employ other strategies.

Regional directors in Houston and Austin report that builders are scrambling to fill their lot pipelines, with a focus on 40-, 45-, and 50-foot lot size programs. Houston regional director Lawrence Dean says the search is true “even for builders who have not historically focused on such smaller lot size product.” In Philadelphia, builders and developers are pursuing deals in top school districts to get ahead of the anticipated move of millennials into the new-home market.

New and small builders are at a disadvantage, paying a premium to get lots on the ground in markets where land is reaching all-time high prices, like Seattle and Salt Lake City. CalAtlantic’s entry into Seattle landed it over 1,500 home sites via its acquisition of Oak Point, and builders who had counted on purchasing finished lots are concerned that the already limited supply of future lots could potentially have just been cut by 30% if CalAtlantic has first right of refusal on Yarrow Bay Developments inventory. Builders in North Carolina’s Raleigh-Durham were also ousted by one of the biggest single land transactions in the market’s history with Lennar’s $25 million purchase of 225 acres in Apex, N.C.

Despite the fact that many markets saw the highest volume of quarterly lot deliveries since the recession, vacant-developed lot inventory continues to trend lower, with the pace of lot deliveries still falling short of quarterly starts. If the price of land (and the expense of developing infill areas) stay at near-high levels, big builders will likely squeeze out smaller builders and further dominate markets where inventory is slim