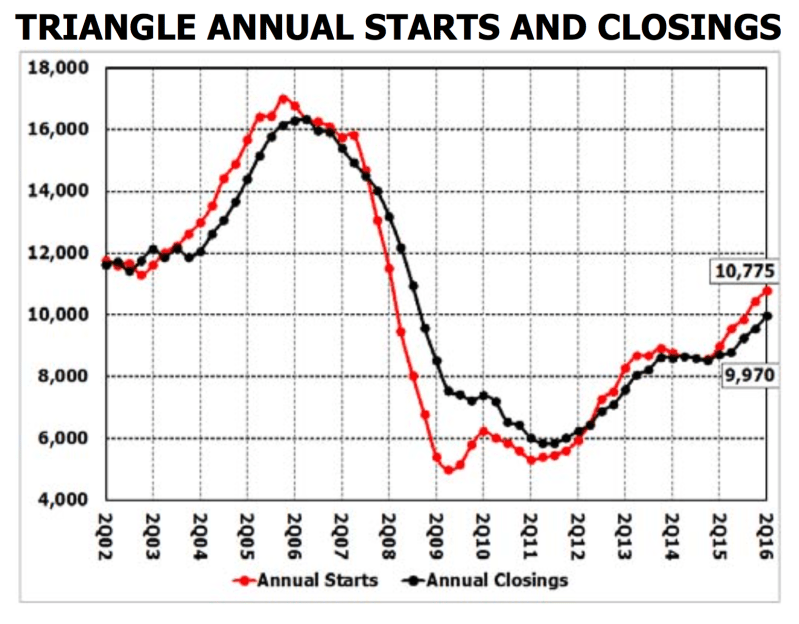

Metrostudy’s 2Q16 survey of the Triangle housing market shows that 3,050 new homes were started, up 12.3% from 2Q15. Quarterly closings – previously unoccupied new homes that now are occupied – totaled 2,770 units, a 14.3% increase from 2Q15. Annual starts surveyed through the end of 2Q16 numbered 10,775, 20% higher than the same period a year ago. Annual closings numbered 9,970 in 1Q16, 14% more than 2Q15.

“The Triangle has been able to grow briskly in spite of the continued strains of labor shortages – which have begun to shift more so toward land development rather than vertical construction – and the major capacity constraints in the public sector,” said Jay Colvin, Director of Metrostudy’s Raleigh-Durham Triangle region. “But inventories are still tight, and all aspects of the construction industry in the Triangle seem to be booming. There are signs that this pace will be tempered by outside sources in the coming quarters. We see this as a positive, and something necessary to keep the market in line with demand.”

In 2Q16, homes priced between $300K and $399K continue to lead the market in terms of production growth rate. This segment started 707 more homes to its total of new starts from a year ago. This broad range of product represents 25% of the total market. Price sensitive buyers continue to have a harder time finding new home options. The sub-$199k price range, with housing inventory of 5.6-months’ supply and only a 15.4-months’ supply of lot inventory, has the lowest total supply number among any price segment in the Triangle. The $200K-$299K market isn’t far behind in terms of shortages, with housing supply of 6.2-months, and only 15-months’ supply of lots. The short lot supply for Townhomes, which have become the de facto lower price option, will further exacerbate the overall supply shortage for more moderately priced housing.

In 2Q16, total inventory – models, finished vacant unoccupied new homes, and new homes under construction – equaled 5,993 units, 15.5% greater than the amount observed in 2Q15. Under Construction inventory stood at 4,153 homes (5-months’ supply), 18.8% higher than in 2Q15. Finished Vacant inventory numbered 1,553 homes, 9.3% greater than in 2Q15. The finished supply decreased to 1.9 months’ from 2 months’ a year ago. At current closing pace, Total Inventory (Models, Finished Vacant, and Under Construction homes) represents 7.2-months’ supply of homes.

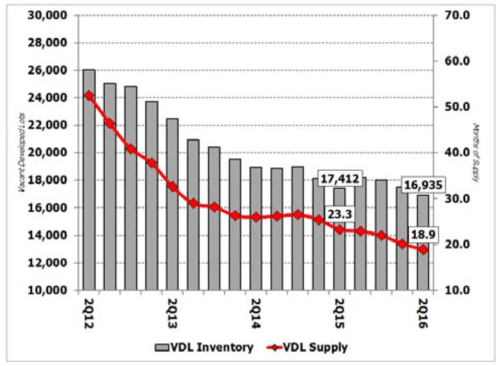

The 16,935 vacant developed lots (VDL) in the Triangle in 2Q16 represent a decrease of 447 lots from the 17,412 lots surveyed in 2Q15. At the current absorption rate, these lots represent an 18.9- months’ supply. Metrostudy considers 18-24 months to be normal, as on average that is the amount of time it takes to entitle and deliver new home lots to the market. In some submarkets, lots supplies are significantly under the 18-month mark, while in others the months-of-supply of lots remains above the 24-month mark.

“The Triangle continues to be a leading market in terms of job creation, population growth, and housing production, and has once again posted strong gains in these critical components of housing demand,” said Colvin. “The area is now seeing 14% more remodeling activity than the prior peak in 2007 and so far in 2016 existing home prices are posting strong gains. New home market participants are being driven to make decisions on the fundamentals, which is great for the longer term growth prospects of the Triangle.”

For further analysis of the Raleigh-Durham market, reach out to regional director Jay Colvin: [email protected]