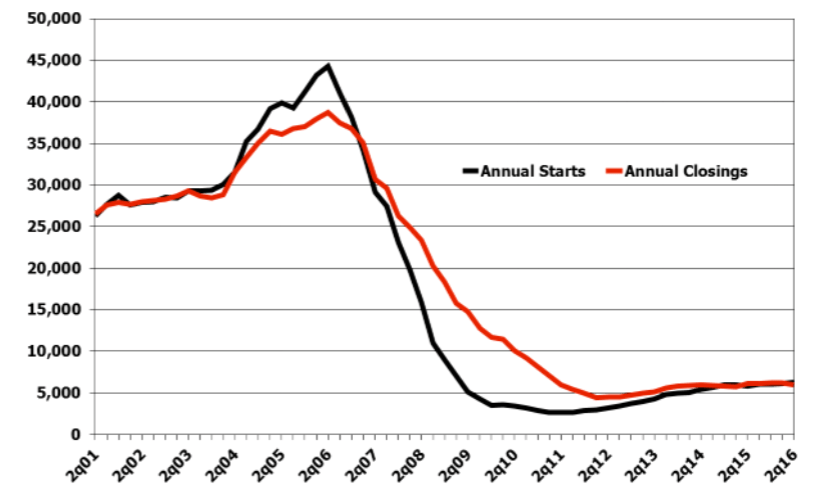

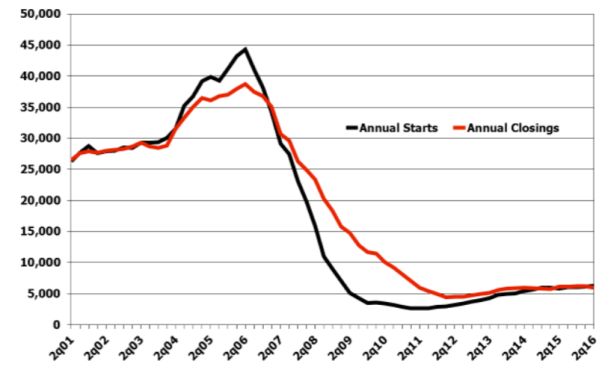

According to Metrostudy’s survey of the new home market in the twelve-county Chicagoland region, there were a total of 6,250 new units started in the twelve-month period ending 2Q16, an increase of 5.6% compared to the previous year. The annual rate of starts increased slightly in the second quarter from the prior quarter, up 125 units. This was the strongest annual starts performance in over seven years. Year over year, the annual rate of closings decreased in the second quarter to 5960 units, a 4.1% decline compared to the prior year.

The 1,728 units started in the second quarter of this year represent an increase of 7.8% from the 2Q15 starts total. The number of homes closed in the second quarter of this year fell by 14.1% compared to the 2Q15 total. Concerns remain regarding rising new home prices, political instability leading to higher real estate taxes and the general lack of confidence shown by consumers in the marketplace.

Builders in this market will be challenged to bring new housing units to market under $300k as construction costs, land and lot prices and development costs continue to increase.

“During the prerecession years, the market expanded into the outlying counties of the Chicagoland area,” said Mark Gianopulos, Regional Director of Metrostudy’s Chicago office. “The post-recession market has seen a consolidation of activity around Cook and the traditional collar counties. Cook, Kane and Will counties in Illinois, along with Lake County in Indiana, continue to account for the majority of activity in the Chicagoland region, with 72% of all new home starts in 2Q16 occurring in these four counties. A decline in new home construction, however, can be seen in Will County for the second straight quarter. The second quarter saw construction declines in five of the 12 surveyed counties, with the largest decreases in Will and McHenry. Outlying areas of the Chicagoland market, are beginning to slowly turn around, with slight construction increases in Boone, DeKalb and Winnebago counties.”

The supply of finished and vacant inventory has remained flat over the past year (currently, it sits at 2.7 months). With the current pace of construction activity, and the slowdown reported by builders of traffic, it is expected that inventory levels might rise slightly heading into the second half of 2016. Metrostudy expects the rate of growth for construction to continue to remain modest, as traffic and contract activity has been lackluster through the Spring.

With the continued pace of new home construction (the rate of lot absorption), and a declining level of vacant developed lot inventory, the months of supply for lots in the Chicago market has fallen from a high of over 250 months in the Third Quarter of 2011, to the current level of 86.4 months. Increases in construction activity in seven of the 12 counties have continued to drive the months of supply indicator downward. While the overall market shows an oversupply of lots, lots in many of the most desirable locations are becoming more and more scarce, leading builders to seek land and lot opportunities in those markets (driving up the price of the land) as well as some secondary markets.

Deed data in the Chicago MSA indicates resale closings in the first four months of 2016 are on pace to exceed the volume of sales in 2015 with the average sales price at $290,552. As the REO market has returned to prerecession levels, home buyers are primarily choosing between new or existing units. There were approximately 23,700 existing home sales in the first half of 2016, this is under reporting as some counties take up to several months in reporting transactions.

The top 15 subdivisions comprise 21% of the new home activity. The majority of these neighborhoods offer models starting under $300,000. Cook County holds the highest percentage of top producing communities with five developments while Lake County Illinois is home to three neighborhoods.

“With a limited supply of lots in “A” locations, builders are looking to infill locations rather than pushing out to those prerecession municipalities to the west,” said Gianopulos. “Builders in this market will be challenged to bring new housing units to market under $300k as construction costs, land and lot prices and development costs continue to increase. Given these factors, Metrostudy forecasts new home starts in 2016 to range from 6,200 to 6,500, representing growth from 6% to 8%. Interest rates and energy costs have remained low, providing further motivation for new home buyers. The amount of vacant developed lots available in the marketplace will provide the necessary supply to meet the demand forecast provided above through 2017.”

For more analysis of the Chicago market, reach out to regional director Mark Gianopulos: [email protected]