We’re into a big week for home building on the capital investment and builder sentiment and confidence front, with a one-two punch on Tuesday and Wednesday.

Not a builder we’ve spoken to of late–large, small, high-end, low-end, east, west, south, north, middle–says that momentum has held up from the first half of 2018 through and into the beginning of the fourth quarter.

“We’ve slowed down, for sure,” has been a widely-spoken mantra. “We’re still seeing good pace, especially at the lower-priced offerings, but it’s definitely slower.”

Almost all of them chalk the slowdown up to “absorbing and digesting” higher interest rates, a necessary adjustment that has historically proved to account for only temporary loss of mojo. Economic, jobs, and wages fundamentals–all on the back of a still surging demographic wave of millennial adults in household and family formation mode, and Baby Boomers in next-stage-of-life mode–are constructive. So, too, have been corporate profitability trends, suggesting further investment in people and growth opportunity.

So, a good-healthy interest rate increase-related belch may be all it takes for the market to resume on its 8-year upward trajectory for another year or two after moving sideways through preliminary push-back to the monthly payment impacts of higher mortgage rates and material price pass-alongs.

That’s the talk-track, at least, for many of the home building executives we’re in touch with over the past few weeks. Their best hope–despite needing to plan for the worst–is that a choppy next few months may reconstitute themselves into solid footing for a “next leg up” for the housing recovery into and through 2020.

Still, although monthly measures are seldom reliable taken in isolation, the coming week’s release of both the National Association of Home Builders/Wells Fargo Housing Market Index and the Census Bureau’s housing starts for September carry more than typical freight of significance, especially on the heels of Wall Street convulsions last week.

Builder sentiment has remained in strongly positive territory, however directionally it’s been slipping over the past few periods. Starts, up a pinch in August, were expected to take a hit in the wake of the impact, especially in the hot, hot Carolinas markets, of Hurricane Florence, whose damage and surge effects extended far beyond the days the storm hit hardest.

Here’s how Wall Street Journal staffers Akane Otani and Tristan Wyatt cue up their analysis– “Home-Builder Stocks Primed for Key Test This Week“–looking at Wall Street expectations related to the NAHB HMI, Census housing starts and permits, and the National Association of Realtors’ existing home sales data, which finishes up the series:

Beaten-down home-builder shares face a key test this week when investors get a fresh look at data on housing starts, existing-home sales and building permits.

Investors have soured on home builders this year, citing signs that the housing market is cooling. A rebound in the housing sector will be pivotal to renewing investor interest in a particularly hard-hit part of the stock market, analysts say.

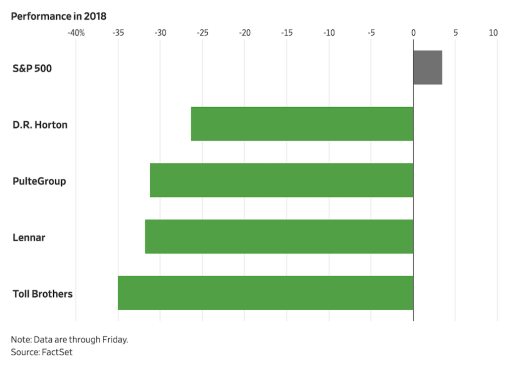

The article notes that the big national home builder shares have taken a bigger beating than the market as a whole, and what’s more, firms with more exposure to higher-end customer segments and price points are getting hit harder, as it’s thought that those companies will be first to succumb to price-point in-elasticity.

The more focus on lower price, entry-level and starter segment homes, the softer the shock to builder shares, as is shown in the chart above.

Jockeying among bigger builders to increase that focus on the entry-level front, and make that lower-priced unit volume scalable geographically accounted for a lot of the mergers and acquisition activity over the past 24 to 36 months. We expect a residual few deals to play out that theme through the coming months, as the biggest players in each of the most active markets continue to wrest operations, construction cycle, and expense gains from market share dominance and local scale, and a few others adjust their customer segment portfolio mix to add in lower price offerings.

Meanwhile, a host of other late-cycle price-decreasing tactics–new density reprogramming, land optimization, products that gain square footage vertically vs. on a lot footprint, etc., and smaller floorplans altogether, not to mention incentives, free upgrades, and other sales inducements–have gotten lots of traction as more builders pivot, at least for the moment, to a “harvest” mentality that can generate sales and volume as priorities, even at the expense of per unit margins.

And, just as deliveries and execution become essential to a builder’s ability to book revenue as forecast, new stresses to schedules emerge in the wake of two staggering hurricanes–Florence and Michael–whose collateral damage siphons both labor and materials from new construction sites to insurance repair work, which pays higher on both fronts.

So, this one will be an important week to gauge how well economic, demographic, and corporate profitability fundamentals do to offset and at least momentary momentum loss due to the multiplier effect of interest rate increases on would-be home buyers’ monthly payment models.