Talk about scary statistics, here’s one from Trulia senior economist Cheryl Young.

“In San Francisco and San Jose, Calif. starter home buyers will need to spend over 100 percent of their income to afford an entry level home.”

For many of our young adult children coming of age as the lifeblood and true north of our communities and cities and wider jurisdictions, earn what they might from pretty good paying essential worker types of jobs–teaching, fire fighting, police work, sanitation, etc.–it doesn’t matter.

Much of our new housing activity, whether it’s in the for-sale, market rate for-rent, or rehab and renovation area, is too expensive for ordinary working people on working people’s salaries and working people’s savings.

You can earn between 80% and 120% of an area median income in more and more markets and sub-markets, and have no choice but to deal with the fact that new apartments and new home communities have nothing for you. You’re priced out, and you’ve got to move far away, or double-up, or delay moving out of a parents’ home because the private enterprise business of housing as we know it can not match its cost models to develop and build to what you can pay.

The problem may be isolated in our minds to a few hyper expensive places we hear over and over again as the regions that have become unaffordable to workforce households. But it’s not an isolated problem in reality.

Among 440 U.S. counties analyzed in the report, 344 (78 percent) posted a Q3 2018 affordability index below 100, meaning homes were less affordable than the long-term affordability averages for the county — the highest percentage of counties below historic affordability averages since Q3 2008.

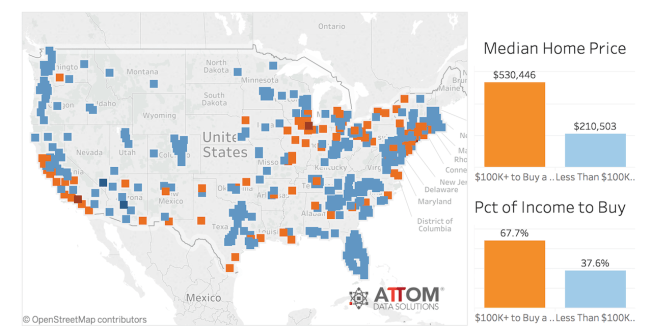

“Rising mortgage rates have pushed home prices to the least affordable level we’ve seen in 10 years, both nationally and at the local level,” said Daren Blomquist, senior vice president at ATTOM Data Solutions. “Close to one-third of the U.S. population now lives in counties where buying a median-priced home requires at least $100,000 in annual income based on our analysis of 440 counties with a combined population of 220 million. U.S. Census net migration data shows negative net migration in more than two-thirds of those highest-priced markets, while more than three-quarters of markets requiring annual income less than $100,000 to buy a home posted positive net migration, indicating that home affordability is at least one factor driving recent migration patterns.

ATTOM Data’s Blomquist notes that home prices in 69 of 440 U.S. counties (16%) require that a household earn $100,000 or more to participate in homeownership.

The culprit? House prices (and rents) have decoupled from living wages, especially of America’s working class households. Blomquist points out:

U.S. median home prices have increased 76 percent since bottoming out in Q1 2012 while average weekly wages have increased 17 percent over the same period. Meanwhile the average 30-year fixed mortgage rate is up 15 percent since Q1 2012 and up 17 percent just over the past year, according to the Freddie Mac Primary Mortgage Market Survey.

And, what’s more, the outlook ahead is worse–higher prices due to higher input costs, higher land use fees and regulatory costs, higher labor expense, higher borrowing costs across the board, and more political will-fueled constraint on new community development. These challenges are not confined to homeownership or for-sale single-family homes. They’re the same ones bedeviling market rate multifamily housing, and, even just as much squeezing developers of supportive housing for low income Americans.

Seeing through the sometimes tricky semantics of the issue here is a first step toward dealing with it.

Access to attainable, safe, decent housing is a social issue that voters and policymakers at the local, regional, and national level must make an urgent priority.

Affordable housing refers, in our business community, to the development of homes, communities, and apartment neighborhoods for people whose earnings fall below a top range of 60% of area median incomes and stretch down to no income at all.

Housing affordability, in our minds, addresses the challenge for working households’ capacity to match their wages to what builders, developers, investors, and planners can bring to the marketplace.

Being able to build quality homes and apartments affordably has been the challenge of the past couple of years, and it’s spiraling upward in intensity and level of difficulty.

This is the single impetus for Hive, our focus on where innovation can and is starting to impact outcomes in the design, engineering, construction, distribution, investment, and technology sector’s collective ability to change the course of this alarming trend.

At Hive, we unpack the issue of affordability and explore where innovative strategy, capital investment structures, building technology, consumer intelligence, and design each must play a starring role in solving for this issue. We’ll look for and recognize root causes of the growing asymmetry between household incomes and the private sector’s capacity to develop attainable access to housing. And we’ll land on action items where companies individually, and as a community may be able to take more control of progress on what has become one of the nation’s most urgent issues.

After all, it’s not just about recognizing and understanding either the problem or some highfalutin theoretical panacea to address it. It’s about what we each–as individuals, as firms, and as a business community–can do. Today.

We hope you’ll be there with us, November 28-29, at Austin’s J.W. Marriott, where we expect passion and applied brilliance of both real estate players, investors, and the tech community will begin showing a pathway to solving for housing’s biggest, hardest, riskiest challenge of the moment. Register by clicking here.