Coming out of the widespread trauma of the Great Recession, one of the most powerful motivators a new home builder could count on to close on a prospective sale was simple household math.

The monthly payment.

It was a single bundle that contained a total for principal, interest, taxes, and insurance to own a new home. It made a deal clear, doable, and rational as a argument over paying about the same amount in rent and having nothing to show for it, or paying for a resale home and risking costly repairs.

The compelling appeal of a monthly payment–which brought a vaguely daunting challenge down to a real world that made practical common sense versus the alternatives–has powered home sales to countless former renters, new families, and refugees of homes that demanded one repair after another.

Want to know when and where you can get locked in on action items you and your team can take on in light of intensifying challenges to affordability and housing? Hive. It’s next week in Austin, and you can register here.

Now, according to Danielle Hale, chief economist for realtor.com, a typically listed home would cost a home buyer $125 more each month than when 2018 started.

And here, Core Logic senior research analyst Andrew LePage, looks not only at where monthly payments are in comparison with past months and years, but where they’re going:

The U.S. median sale price in August 2018 – $226,155 – was up 5.7 year over year, while the typical mortgage payment was up 14.5 percent because of a nearly 0.7-percentage-point rise in mortgage rates over that one-year period.

A consensus forecast[1] suggests mortgage rates will rise by about 0.5 percentage points between August 2018 and August 2019. The CoreLogic HPI Forecast suggests the median sale price will rise 1.9 percent in real, or inflation-adjust, terms over that same period (or 4.7 percent in nominal terms). Based on these projections, the real typical monthly mortgage payment would rise from $922 in August 2018 to $1,000 by August 2019, an 8.4 percent year-over-year gain (Figure 1). In nominal terms the typical mortgage payment’s year-over-year gain would be 11.4 percent.

Another analysis of what’s going on with monthly payments–using different baselines, such as median sale prices, for “typical” and looking at different markets–comes from Forbes’ correspondent Ellen Paris, who writes:

According to Realtor.com, “the average U.S. monthly mortgage payment has jumped 15.8%, or $223 per month, since last year.” In September 2017, that number was $1,413, rising one year later to $1,636 based on a median price of $294,900. “In the top 20 largest markets combined, 68% of the incremental payment increase is now coming from a rise in rates,” Vivas explains. “This is a big shift from earlier this spring when rates accounted for just 36% of the payment increase,” he adds.

The combination of rising interest rates and higher prices–particularly on new homes as builders try to pass along cost increases on labor, land use fees, and materials to new home buyers–has elevated the risk that an attainable monthly payment for a renting, or existing home household could lose its appeal.

Household wages, you see, have been going up, but they haven’t kept pace with monthly PITI trends, and cost inflation and the impact of tariffs are starting to hit home as well. Interestingly, wage growth is tracking higher for lower-wage workers. This might align with how and why demand among entry-level buyers has remained strong, while more builders are seeing weakness in their first-time move-up and second-move-up segments. Still, household income growth has been eclipsed by both interest rate impacts and home prices, leading Core Logic’s LePage to conclude:

An IHS Markit forecast calls for real disposable income to rise by around 2.5 percent over the next year, meaning homebuyers would see a larger chunk of their incomes devoted to mortgage payments.

So, builders, who’ve reported widening and deepening challenges to their sales pace in an increasing number of their market arenas, have pivoted tactically. Free upgrades, in some case, and other value-increasing incentives comprise the first set of tools from the kit, and then rate buy-downs, down payment assistance programs, and discounts figure into the push to keep absorption rates at a respectable level.

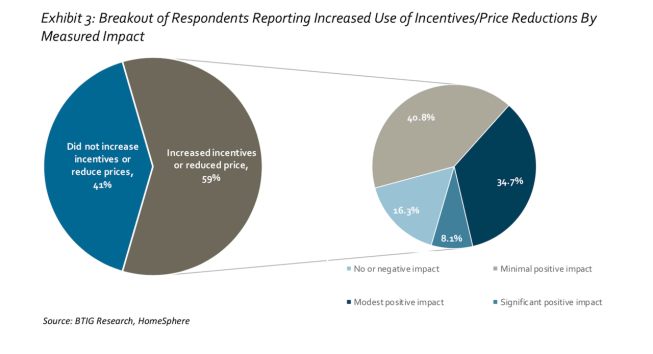

A monthly BTIG/HomeSphere Homebuilder Survey, conducted by Carl Reichardt, Jr., and his team at BTIG, notes that more builders face slowing sales and traffic reduction in their sales centers, phenomena three out of five home builder respondents are trying to counter with price and incentives promotions. Reichardt writes:

Approx. 60% of surveyed builders have raised sales incentives or cut base prices this year, with mixed results: 57% of those builders who offered incentives/cuts have seen minimal or no positive demand response from consumers to them, but 43% report modest or significant positive response.

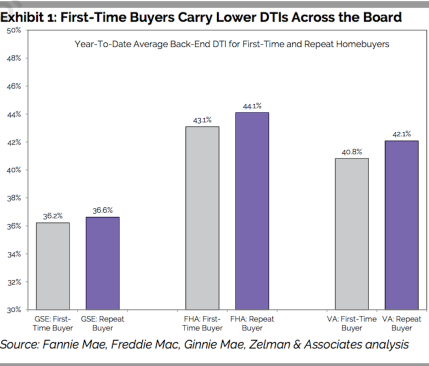

In trying to unpack whether “affordability” tolerance points or price rigidity are key factors in the slow-down in activity, the team at Zelman & Associates zeroes in on a key metric most real estate analysts say accounts for a bright line between affordability and un-affordability: mortgage debt-to-income ratios. This KPI factors in the PITI bundle, plus auto loans, credit card balances, and/or student debt, and it has been tracking upward.

In the latest issue of The Z Report explores the notion that worsening affordability and un-affordability are two separate and distinct phenomena. This is a critical tenet of Zelman’s still-constructive take that the current deceleration in new-home sales activity–while more extensive than anticipated–may be a temporary plateau rather than the beginning of a down-cycle. Looking at DTI’s for entry-level buyers, which one might assume are the most sensitive to intolerance points on pricing, the Zelman team finds no smoking gun evidence of a break point.

When comparing 2017 to 2018, the increase in DTI ratios is almost identical for entry-level buyers, climbing 110 basis points on average, versus repeat buyers up 100 basis points. We believe it is an encouraging sign that entry-level buyers, which are most susceptible to affordability constraints, are not stretching more than move-up buyers where affordability is less of an issue.

From our perspective, affordability is a cross section of many factors that require attention in a holistic manner. From this wider lens, we believe entry-level affordability is still favorable from a historical perspective, but recognize that future home price appreciation will likely be governed by impact on monthly payments.

This puts new home builders in more of a bind, considering that interest rates will keep edging upward, land fees are going up, cost inflation on key household items is still under pressure, and household income increases may continue to lag these other factors.

Monthly payment-driven sales initiatives baked in a classic “win-win,” because while they exerted a strong draw to folks wanting to escape the rental or resale home merry-go-round, they also amounted to what builders wanted on a per unit gross margin basis.

With the move from a sellers to a buyers’ market, it’s builders who are going to have to either increase their productivity and drive their expenses lower, or they’re going to build and sell units at a loss. That’s not a business.