The Riverside-San Bernardino metro remains one of Southern California’s most active new home markets, and recent sales data shows that leadership in the region is increasingly concentrated among a small group of high-volume builders.

According to Zonda’s proprietary new-home data from the last 12 months ending March 2026, the top five builders are averaging about 3.2 sales per community per month, compared with roughly 1.4 among all remaining builders in the metro. That gap highlights how concentration is shaping the competitive landscape, particularly as smaller and regional builders face pressure from land costs, incentives, and buyer affordability constraints.

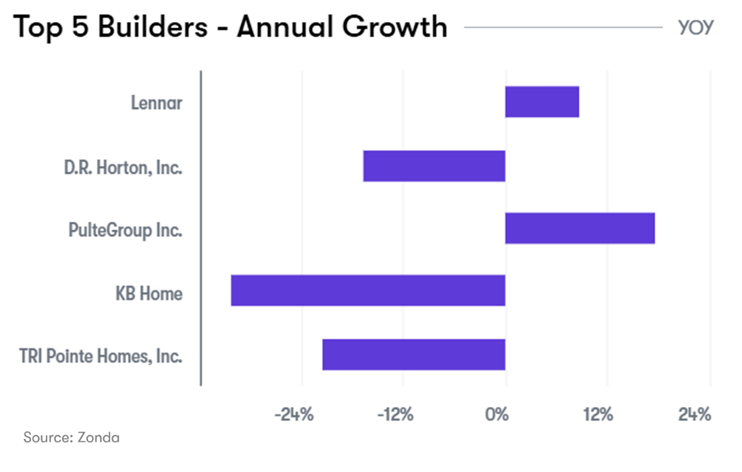

The Top Five

At the top of the rankings sits Lennar, who continues to lead the metro by a wide margin. Over the last 12 months, Lennar recorded 1,971 new-home sales, translating into 23.2% of all observed new home transactions in the region. That volume advantage has also supported positive year-over-year growth, a notable achievement given broader market headwinds and softer total sales across the metro.

D.R. Horton holds the No. 2 position, posting 1,162 sales in the past year and a market share close at 13.7%. While the builder remains a major force in the region, annual sales have declined 16.5% year over year.

Ranking third is PulteGroup, who stands out as one of the few top builders to post meaningful year-over-year growth. With 864 sales in the past year and a 10.2% share of the market, PulteGroup recorded the strongest growth among the top five builders, with sales up 17.7% from the prior year.

KB Home follows closely in fourth place, capturing 9.6% of total market share. Although annual sales declined compared with the previous year, KB Home remains a volume leader in the region.

Rounding out the top five is Tri Pointe Homes, with 586 sales over the past year and 6.9% market share. While its sales volume trails the other top builders, Tri Pointe maintains a strong presence in the region.

For those watching this inland metro, scale and product alignment remain decisive advantages, and the builders best positioned to deliver consistent volume are likely to continue gaining share as the market works through its next cycle.

The insights in this article were taken from more in-depth research reports published with Zonda’s Enterprise Subscription.