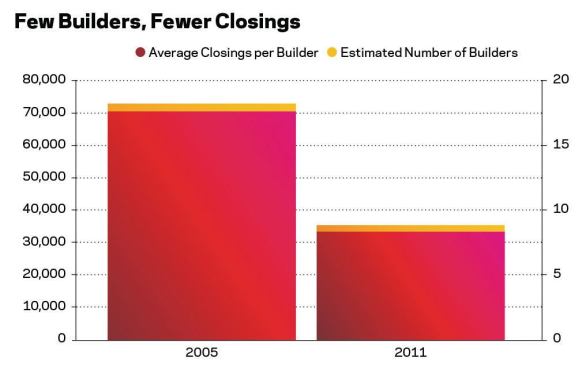

More than 73,000 builders were active in 2005, chasing 1.3 milli…

Even in down years, the Builder 100 and Local Leaders data releases are a celebration of the winners. The builders improving in rank, or growing, or not declining as much as the market are especially important—despite numerous challenges and difficulties they are finding a way to prosper, not just survive. How hard has it been to survive? In 2005, we estimate that there were more than 73,000 active builder companies across the country. In 2011, that number had declined to less than 34,000, a decline of over 50 percent.

Besides being smaller in number, builders have also learned to operate with fewer sales and closings. In 2005, there were almost 18 closings per builder on average. In 2011, there were fewer than nine closings per builder on average.

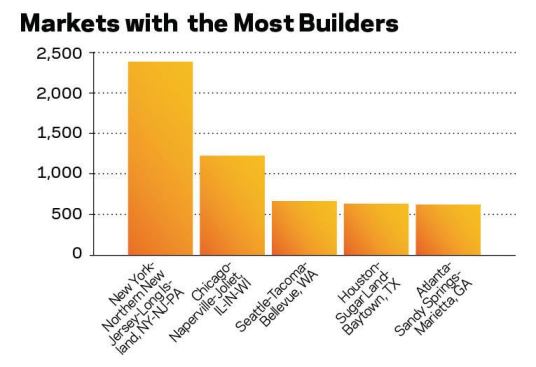

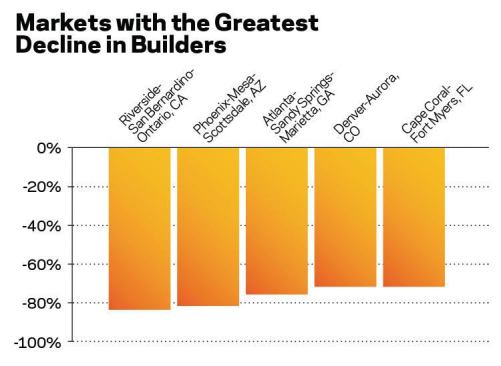

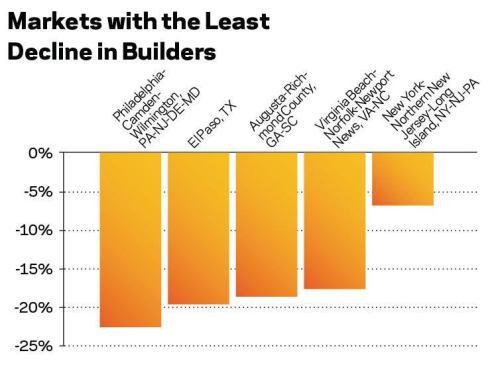

Looking at the 50 largest home building markets in the country featured in the Local Leaders charts (see page 72), three of those markets now have less than 25 percent of the number of builders that were operating in 2005—Atlanta, Phoenix, and Riverside-San Bernardino, Calif. The Local Leaders in these markets are the very definition of survivors.