“It has taken a shotgun to what might have been better addressed with a fly swatter.”

That’s a quote from Jonathan Johnson, an attorney at Hopping Green & Sams in Tallahassee, Fla., describing the Internal Revenue Service and Department of Treasury’s proposal to change what qualifies as a political subdivision, thereby restricting many builders and developers from having access to tax exempt bonds.

In 20 states, developers can secure tax exempt bonds to finance infrastructure projects like roads, sidewalks, and sewer systems by establishing special purpose taxing districts made up of political subdivisions.

“With these proposed regulations, you would basically be neutering and rendering much less effective an important tool for how infrastructure has been financed in these states,” says Johnson, who has been working exclusively on special purpose taxing district cases for nearly 20 years. If passed, he adds, the regulations would hurt builders’ and developers’ bottom lines. “Without access to the tax-exempt capital markets, you’re going to see increased costs for the development of the backbone, basic infrastructure, which translates into reduced returns, more expensive product, or changes in the development timing or plans.”

Once the infrastructure is financed through the developer (after receiving the tax exempt bonds from a state or local government) and enough people move into the area, its residents eventually assume control of the roads, sidewalks, sewer systems, etc. and are responsible for the upkeep.

That’s all well and good, says the IRS, but when a developer gets a tax exempt bond and uses it for a political subdivision that serves a commercial purpose, such as a golf course, there is an issue. Since no one lives in a commercial district and there are no residents to one day take it over, it stays perpetually in the hands of the developer. That’s a problem, says the IRS.

The main concern for the National Association of Home Builders is that in order to receive a tax exempt bond, a special district would have to have people living in it. J.P. Delmore, federal legislative director for the NAHB, asks how can people move in when the homes and infrastructure have yet to be built?

“When [a tax exempt bond] is used for residential infrastructure there’s always going to be an initial development period when the developer controls the district because no one’s living there yet,” he says. “There is no way to make people live there before you build them a home.”

The other sticking point for the NAHB, Delmore adds, is not only the regulations’ impact on future development, but for the hundreds already in place. “It could also hamper the existing developments’ ability to recapitalize and maintain that infrastructure,” he says. “It wouldn’t be able to issue new tax exempt bonds moving forward.”

“It seems that the IRS has an issue with a few bad actions out of a multi-billion dollar industry that has mostly worked very well and the way it’s intended,” Johnson says.

The regulations would amend the eligibility requirements for a political subdivision in order to provide “greater certainty to prospective issuers and to promote greater consistency in how the definition is applied across a wide range of factual situations.” The proposal calls for a political subdivision to meet three requirements, taking into account all of the facts and circumstances: Have sovereign powers, serve a governmental purpose, and have governmental control.

Governmental control is the major change and the biggest issue, explains Carter Froelich, managing principal, Development Planning & Financing Group. To check off the governmental control box, the proposal states, a political subdivision must meet one of three criteria: The right or power both to approve and to remove a majority of an entity’s governing body; the right or power to elect a majority of the governing body of the entity in periodic elections of reasonable frequency; or the right or power to approve or direct the significant uses of funds or assets of the entity in advance of that use.

In the IRS proposal, it states, “Rights or powers to direct the entity’s actions only at a particular point in time are not ongoing and, therefore, do not constitute control.” Also, the proposed regulations state, “control by a small faction of private individuals, business corporations, trusts, partnerships, or other persons is fundamentally not governmental control.”

In 2013, the IRS issued a Technical Advice Memorandum (TAM) declaring additional requirements for political subdivisions after auditing a development community in Florida, Johnson explains. To make the requirements official, the government agencies are looking to formalize those additions. But, Johnson adds, “They’ve done so in an extremely overbroad manner and in a way that’s exceptionally detrimental to this critical tool for the development and building trades.”

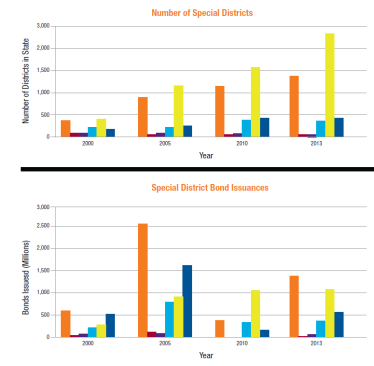

Courtesy NAHB

Trey Lary, an attorney with Allen Boone Humphries Robinson, a firm with offices in Austin and Houston that deals exclusively with special purpose taxing districts, says he’s concerned with the proposal’s potential impact in Texas. He’s part of a collation of professionals who are associated with special purpose taxing districts and work toward public policy goals.

In the Houston area, Lary notes, millions of people live in Municipal Utility Districts (MUDs). People from across the country move to the Greater Houston area and Texas as a whole because the state offers well-priced homes and strong job growth. Without these special purpose taxing districts, though, Lary says that could change. “I’m very concerned about any proposal from the IRS that would interfere with, or diminish the ability of, utility districts in Texas building infrastructure that is necessary for, and contributes to, our economy,” he says.

The IRS and Treasury are currently accepting comments on the proposed regulations and will do so until May 23. Then, there will be a public hearing on June 6 in Washington D.C.

“I think the IRS has bitten off a bit more than they expected with this but we’ll see how they respond,” Delmore says.

“They really opened up a can of worms and who knows what’s going to happen?” says Froelich.