Adobe Stock/Elenathewise

Young adults.

To a number of us in the housing sector, the two words together smack of a contradiction in terms, but don’t be tempted to laugh.

Instead, compound the oxymoronic challenge of that term with another one: Millennials. What and whom that demographic references, what it means for home builders and residential developers, and why it matters, continues to matter, and will always matter is the thing here.

If you thought that crossing into a new decade would mean freedom from housing’s obsession with America’s single-largest generational cohort, America’s single-largest labor force age-group, and America’s single-largest conundrum on housing preference and behavior, think again.

Plain truth of the matter is that–like so many other topics that abound in study, data, and exponential theorizing–we don’t know a lot more than we know about Millennials and their ultimate housing choices.

Rather than working from some deep base of knowledge into Millennial whys and wherefores, we’re really at just the beginning of a learning curve. And that learning curve alone will very likely last at least the 10 years that will compose the 2020s. The good news is that what we need to learn fits nicely into four buckets of challenge.

- When?

- Where?

- Why?

- If

The other good news is that recent years of relatively robust home purchase traction among leading-edge Millennials rules out the “failure-to-launch” and “renter nation” scenarios being bandied about at the onset of the just-finished decade of the 2010s.

Still, these are some big questions. What’s more, Millennials’ ultimate uptake on homeownership as a generation hangs in the balance of the 10 years we might equally well call either the “Roaring 20s” or the “Snoring 20s.”

Being more educated, they both earn more and owe more than young adults typically have at their 17-to-37 year-old lifestage.

Now, we’ve learned this much about Millennials: As household formers, family formers, and home buyers, they’re at best, “better late than never.”

That’s a root cause issue for predicting demand for those in the investment, development, construction, distribution, and manufacturing business of new homes and communities.

But isn’t it in fact a symptomatic mask of a more profound societal root cause?

The real, roiling root cause around all the key questions for our young adult, Millennial, first-time buyer cohort has to do with this: Far too much focus on what’s held housing back for a decade now has been on cost and supply constraint. Far too little focus has been on an area society has been struggling with and challenged by but begs for solutions: wage and earnings growth.

Earnings uncertainty tied to fundamental “future of work” ambiguities. In June 2018, Census analyst Benjamin Gurrentz wrote, “For Young Adults, Economic Security Matters for Marriage.” He noted:

It is unclear which aspects of economic security truly matter with regard to young adult marriage rates: At the aggregate (county) level, is it a matter of employment, wages, poverty, or housing? Or, do all these factors matter? Moreover, how does the measurement of each concept matter to understanding how an economic prerequisite to marriage may operate among young adults?

The job now is to match data- and technology-enhanced human judgment, planning, product development, and marketing with present- and future foreseeable earnings security–employment, marriage, and plans for family formation.

Meyers Research director of economic research Ali Wolf has this clear-eyed, evidence-vetted take on detecting hole-in-the-donut opportunities for developers, builders, and residential land investors counting on a Millennial surge in the 10 years ahead.

The housing industry has been waiting for years for a full rebound in the homeownership rate among young shoppers. For example, the homeownership rate for those under 35 years old averaged 40.8% in the year 2000, peaked during the housing boom at 43.6% in 2004, and remains depressed at 37.5% today.

With marriage assumed to be the ticket to owning a home, we collected data on top metros across the country to look for commonalities in Millennial homeownership.

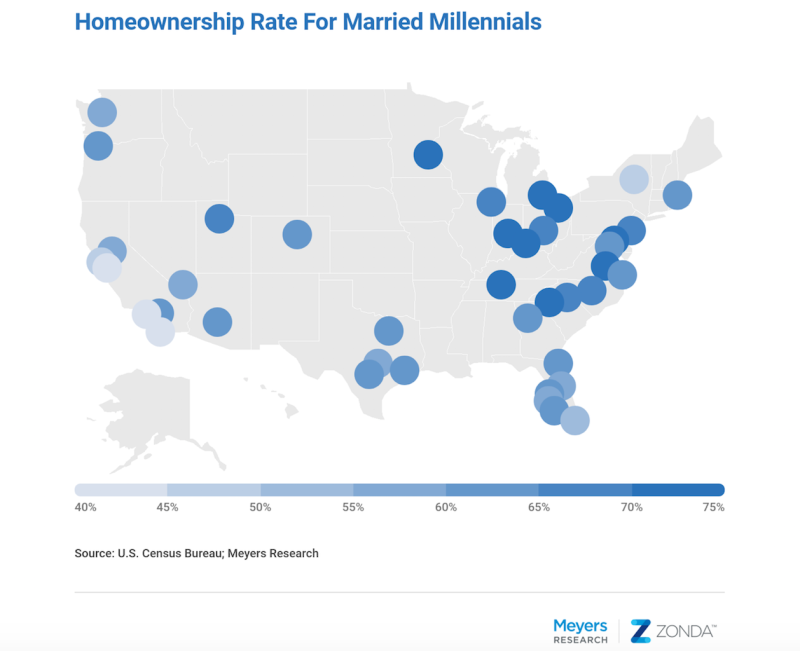

- As expected, the average homeownership rate for a married Millennial in top metros is 60% compared to 43% for those not married.

- Of the markets with the highest share of Millennial homeowners, there’s a large cluster in the Midwest (six of the top 10). Select markets in the Southeast and Northeast also have relatively high rates of ownership.

- Five markets show a homeownership rate for married Millennials over 70%: Indianapolis, Greenville, Detroit, Cleveland, and Minneapolis.

The map below highlights that markets that offer relative affordability through a combination of lower-priced homes and quality jobs allow Millennials to follow the more traditional life path similar to their Boomer parents, which includes marriage, buying a home, and having children.

MARRIAGE STRUGGLES TO SOLVE FOR AFFORDABILITY

Focusing on changes in lifestage without considering affordability can be misleading though.

- The areas with the largest share of married Millennials do not necessarily correspond with the highest homeownership rate for the cohort.

- In some markets across the country, marriage is related to a huge jump in ownership rates, while in others, the difference is negligible.

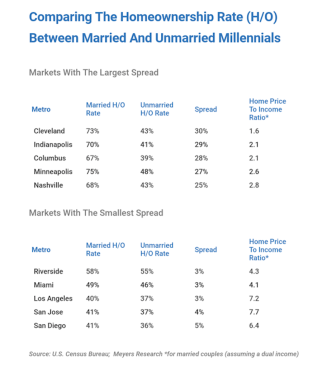

We calculated the spread between married and unmarried Millennial homeownership rates (see table below) and found a clear distinction related to affordability. For example, of the top markets, Cleveland has the largest spread between married and unmarried homeownership rates and has the lowest home price to income ratio** of 1.6, according to Zonda. The markets with the smallest spread are among the most notoriously expensive in the country.

Of the ten markets with the highest home price to income ratio, two challenge the idea that affordability is the sole driver: Portland, where the spread is 24% and Denver with a 21% difference. Both have a home price to income ratio of 4.1. Going past affordability, these outliers force a second set of questions:

- Where are the jobs?

- Where do people want to live?

- What can you get for the price?

- Are the homes large enough for a growing family to justify the price?

“These questions force our team to figure out the subtleties of each community we work on to determine how deep the demand is at a given price. Lifestage catalysts like marriage and having children are extremely important but we also have to consider what else drives the purchase decision,” explains our Senior Managing Principal of Advisory, Tim Sullivan.

This research reiterates the need for increased and modified new home offerings, concerted efforts by economic development councils to bring in more high-paying jobs, and that lifestage factors are a part of an even bigger puzzle to analyze demand.

What Ali Wolf’s analysis also shows is that variances–over time, as we progress along the Millennial learning curve–between True North and Magnetic North in navigating the relationship between Future of Work employment centers and housing market metrics will continue to show up and need course-correcting. Embrace the algorithm.