If the people at Wells Fargo Securities’ Building Products and Homebuilding Investment Banking practice and L.E.K. Consulting are right, and 2019 is a good year, (not a bad one), everyone will know why.

Whatever anybody says is the root reason, it will be because you–builders, developers, architects, investors, and partners–will have begun to crack the code.

Millennials.

The “pent up” ones, namely.

And it won’t be because of things you’re getting ready to do now to deal with a newly emerging set of uncertainties and headwinds. Rather, it’ll be because of what so many of you have worked at for years now–on design, product, density, operational processes, selling and data systems to make the present day’s nearest facsimile to starter homes, in starter home neighborhoods, for people who want and need them.

The mix shift is so overdue, and can’t come a moment too soon. ASPs on new homes averaging closer to $400k than to $200,000 have been our great nation’s way of telling most young adults–in no uncertain terms–“we’ve got nothing for you.”

But that mix shift–the combination of new communities coming online and the new barrage of competitive incentive-based pricing, financing, and other terms–has begun now to kick fully into gear, and as long as housing finance becomes part of the solution rather than part of the problem, a good year is entirely possible.

Thanks to Millennials.

They’re the ones who, by the way, aren’t already owners paying mortgage interest rates in the low 3%s, like their 55+, Boomer parents tend to be doing.

They’re the ones whose job opportunities have been improving in a really good, fast-growing, talent-deprived economy, helping–over time–to offset big loans they took on to get through college. Many of those job opportunities allow for flex-time and remote work options that expand–to some degree–flexibility around distances to job centers.

They’re the ones, too, who in many cases, can turn to “the bank of mom and dad” for help on a down payment.

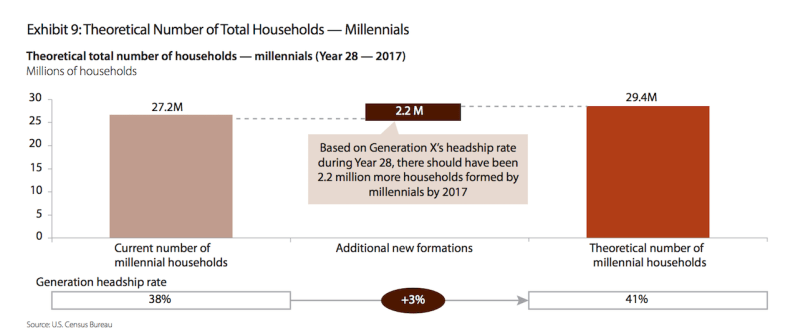

The Wells Fargo-L.E.K. study counts the birth years of the Millennial cohort differently than other demographic experts, but observations and conclusions relative to housing behavior are the same.

As prior generations reached age 35, approximately six years away for millennials, headship rates have historically approached 50%. Therefore, not only should millennial formations be a material driver of growth in the long term, but they could also do so at an accelerated rate given the current gap to the Generation X trend line, seen below in Exhibit 10. Should millennials track to the average headship rate of Gen X and baby boomers by 2023, this would imply 1.54 million millennial formations annually over the next five years. Despite the economic and behavioral dynamics that delayed millennials in forming households while in their 20s, we view the aging of millennials as a credible demand driver over the medium term.

The Wells Fargo-L.E.K. analysis bases its favorable forecast, when it comes down to it, on the same fundamental demand driver–pent-up demographic pattern-related demand–we’ve noted for years as the backdrop of the decade we’re in right now. That’s nothing new.

We’re also well aware of both the demand suppressors and the supply constraints that have played a role in driving a wedge between demand-on-paper and actual, real-world household formation, and home-purchasing behavior.

A new Pew Research 40,000-ft. look at the mystifying differences between Millennial young adults and the consumer and housing activity of prior generations of young adults, notes:

Millennials, hit hard by the Great Recession, have been somewhat slower in forming their own households than previous generations. They’re more likely to live in their parents’ home and also more likely to be at home for longer stretches. In 2018, 15% of Millennials (ages 25 to 37) were living in their parents’ home. This is nearly double the share of early Boomers and Silents (8% each) and 6 percentage points higher than Gen Xers who did so when they were the same age.

The rise in young adults living at home is especially prominent among those with lower education. Millennials who never attended college were twice as likely as those with a bachelor’s degree or more to live with their parents (20% vs. 10%). This gap was narrower or nonexistent in previous generations. Roughly equal shares of Silents (about 7% each) lived in their parents’ home when they were ages 25 to 37, regardless of educational attainment.

Millennials are also moving significantly less than earlier generations of young adults. About one-in-six Millennials ages 25 to 37 (16%) have moved in the past year. For previous generations at the same age, roughly a quarter had.

If you look closely above, you may pick up where we see real, near-term opportunity for builders to turn up the heat on their pricing, incentives, marketing, and big data journey mapping. That 10% of millennials still living with parents who do have a bachelor’s degree, not to mention the millennials who’ve been living in apartments and are currently going through lease-renewal cycles in markets where rent power has been strong.

That kind of “pent-up” demand differs from the broad paintbrush of cohort size, age, and other big-number demographics.

It’s in that kind of demand we may begin to pick up a pivot in psychology among educated, better-paid young adults, who’ve behaved as smart consumers for the past several years as though they have time on their side.

From an age, biological clock, and family formation point of view, those millennials may have begun to have run the full course of having time on their side. They’re reaching the “now or never” point in their lives, in bigger numbers, with greater levels of education, with a stronger employment environment, and–after all–better capability of taking on a mortgage than ever before.

Now we’ll see how all of the work builders have done to ready themselves for this moment–with product, pricing, and locations ready to truly activate this young adult, increasingly urgent buyer pool.