The strength in the housing market today is driven by nearly every buyer type, which allows for different products, price points, and geographies to thrive. Each of these buyer groups share five main motivations for buying a home today, including taking advantage of rising prices, locking in a mortgage with historically low interest rates, the increased savings throughout 2020 and early 2021, the pandemic-induced lifestyle changes, and the intangible psychological effect of “fear of missing out.” Each buyer group, however, also has its own unique set of motivations and risks that are important to understand when trying to forecast housing growth.

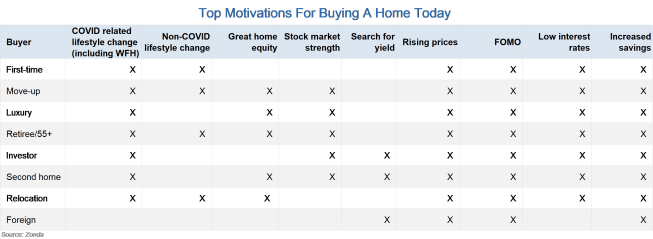

After a brief pause, the housing market flourished in 2020, and Zonda’s forecast calls for another great year in 2021. The current enthusiasm stems primarily from today’s buyers. Of the eight main home buyer groups, seven of them are fully engaged in the housing market today. Foreign buyers, the eighth group, have some limiting factors related to COVID-19 that are holding back the full potential of the cohort. See the table for the eight groups and the main motivations for each, as well as buyer-specific analysis below.

1. First-Time Buyers

First-time buyers include individuals of any age but are largely comprised of millennials, those between 21 and 41 years old. The full extent of the cohort took years to be realized after the Great Recession, but millennials are not only the largest living generation but also today’s top home buyer. This cohort is not exclusively buying entry-level product, though. Some millennials waited until later in life to purchase their first home for lifestyle or financial reasons, resulting in their first home looking more like a move-up property. The increased savings throughout 2020 was among the most impactful for first-time buyers. The cohort cites affordability and the inability to come up with a down payment as the No. 1 reason they do not already own a home.

Motivation: A Zonda survey of millennials conducted from December 2020 through February 2021 asked homeowners in the cohort why they decided to purchase their home, and their top three answers were: stability and settling down; the desire to make somewhere their own; and appreciation and rising home values. Other motivations include a favorable rent versus own equation, change in lifestyle including marriage or having a child, and the desire for more space.

Impact on overall inventory: When a first-time buyer becomes a homeowner, they are removing a home from the market. First-time buyers are often competing with downsizing baby boomers, other cost-constrained individuals, investors, and some move-up shoppers.

Risk: This is the biggest and most powerful group of the seven active shoppers with a lot of runway remaining. Affordability is the No. 1 risk to monitor with rising prices, eventual higher mortgage rates, and an inevitable wallet share shift. Watch the policy response though. If demand from this cohort starts slowing, the Biden administration appears ready to push through the $15,000 first-time buyer tax credit. The controversial $10,000 student loan forgiveness program is still on the table as well.

2. Move-Up Buyers

When the housing market slowed in March and April of last year, many were quick to remember the price drops of the Great Recession. There was a collective sigh of relief when it became apparent that the housing market was actually bucking the unemployment and uncertainty trends and started to grow again in late April and May, led by move-up buyers. Move-up buyers span different generations but are generally associated with Generation X, those between 41 and 61 years old. Move-up buyers benefit greatly as home prices increase, especially if they’ve paid down a good amount of their existing mortgage.

Motivation: In 2020 and early 2021, move-up buyers experienced two main things: equity gains and a lifestyle change. CoreLogic data estimates that equity is up $17,000 on average nationally over the past year, which is important for both confidence and for funds to be used for the next home. Furthermore, the ability to work remotely combined with children who are schooling at home drove many of these shoppers to upgrade their space, usually including more square footage.

Impact on overall inventory: These buyers often need to sell a home to buy a home.

Risk: Move-up buyers are susceptible to changes in wealth, including a faltering stock market or falling home prices. Watch for some would-be move-up buyers staying put due to the lock-in effect of refinancing at historically low interest rates, which will assist in keeping inventory low and slow overall transaction volume.

3. Luxury Buyers

The luxury market means different price points in different markets, but the buyers’ needs are often the same. They are looking for quality space with some special features. Discretionary and often selective, luxury buyers are active in today’s housing market fueled by many of the same drivers as move-up buyers, including more time spent at home and increased wealth. Moving to lower-taxed states also has become increasingly popular as there is more flexibility around where we live.

Motivation: The COVID-19 pandemic upended all of our lives, and this buyer group was, and is, well positioned to control how their daily life is impacted by moving into a home that better suits their evolving needs.

Impact on overall inventory: Luxury buyers may sell a home to buy a home, keeping the impact on supply neutral, but may also keep an existing home as either their second home or a rental property, pushing inventory lower.

Risks: Risks include any shocks that could negatively impact these buyers’ net worth, changes or tightening to jumbo loan lending standards, and higher interest rates contributing to the lock-in effect.

4. Retirees/55+

The retiree/55+ buyer is at a unique time in life where their lifestyle likely has either changed or they are planning for a change. Planned retirement, forced retirement, early retirement, chasing grandchildren, or just simply looking for a larger or smaller home are all reasons why this buyer group is shopping.

Motivation: The 55+ buyer was hit harder and stayed away longer than some other buyer types in 2020. Once it became clear that the stock market rebound was not a head fake and personal protective equipment was commonly available, the 55+ buyer started buying homes in phases. Buyers in their local markets came back first before those who were relocating. Now, the strength is virtually universal on many of the same reasons listed above, including low interest rates, good home equity, and lifestyle changes brought on by COVID-19.

Impact on overall inventory: Many 55+ homeowners, depending on the state where they live, are disincentivized from moving due to tax reasons. For those who do move, some opt to hold their existing home as a rental property, depressing inventory, while others sell and buy a home where the impact on supply will depend on the price of said homes. Depending on the level of wealth, this group is competing for inventory against first-time buyers, move-up buyers, and the luxury buyers.

Risks: Like the luxury buyer, fluctuations in net worth can impact demand. Housing inventory is also a big factor. The 55+ buyer often has specific needs with single-story homes with good accessibility to retail, hospitals, and family. Finally, there is a group of these buyers who are not financially constrained given their stock holdings and home equity. However, 48% of adults older than 55 have no retirement savings, according to AARP, and many live on a fixed income. As such, affordability is also important to watch for this cohort.

Take from our expert: “The 55+ market took a significant pause in the early days of the COVID-19 pandemic, particularly due to travel restrictions and the disproportionate effects of the virus on the older demographic,” says Kristine Smale, Zonda’s senior vice president of advisory for Florida. “However, the subsequent rebound and frenzied demand surprised even the most bullish home builders. Record stock market returns, which are closely tied to retirement savings, created even further comfort and motivation for a new-home purchase.”

5. Investors

Investors were a staple of the housing market during the mid-2000s housing boom. Both mom-and-pop and institutional investors scooped up many of the foreclosed homes in the wake of the heyday, but some were left scarred from the boom-bust cycle. Fast-forward, and the changes brought on by COVID-19 supported renewed interest in purchasing an investment property. Some investors are seeking rental income, and the tenant pool for single-family dwellings is heightened as people look for larger homes and more private space. Other investors are incentivized by rising home prices, for which there is no shortage today.

Motivation: For investors, the main drivers are portfolio diversification and the search for yield.

Impact on overall inventory: Like first-time buyers, typically when an investor buys a home, they are a drag on overall supply levels. Groups like Opendoor and Zillow Offers, for example, are offering a “stress-free sale” for those considering listing their homes, competing with other potential home buyers and helping to keep inventory suppressed. Estimates from the National Association of Realtors calculate that 14% of homes sold in December were from either individual investors or the next buyer group on our list, second-home buyers. Investors are scooping up both new and existing homes, but we are starting to see some builders implement a “no investor” policy at some of their communities.

Risks: Risks for investors come back to their core motivation: making money. If mortgage rates rise, home price growth slows or drops, or better returns are found in other investments, the investor pool could shrink.

6. Second-Home Buyers

2020 was the year of the staycation, including a search for a “home away from home.” Not everyone was in a financial position to buy a second home, but for those who were, the lifestyle changes brought on by the pandemic fueled demand.

Motivation: Much of the motivation for the second-home market was driven by the desire for more space. The ability to work from home and leave employment hubs sparked a shift, with low interest rates adding fuel to the fire.

Impact on overall inventory: Like first-time buyers and investors, when second-home buyers purchase a home, they drag down overall inventory levels. Watch for a shift in the mindset come the vaccine economy. Some who bought a second home because of the pandemic may realize they don’t use it enough and decide to offload it.

Risks: The biggest risk is a lot of the second-home demand was pulled forward.

Take from our expert: “At the outset of the COVID-19 pandemic, second homes were viewed as a refuge from more crowded population centers,” says Adam McAbee, vice president of advisory at Zonda. “As employers shifted their workforce to a virtual platform and schools shifted to online learning, these units—often within a three-hour drive of home—started to serve as “temporary primary” housing. With continued demand and low or often nonexistent inventory today, prices are on the rise, as households reevaluate life in the big city.”

7. Relocation Buyers

2020 enabled freedom for where we live unlike any time in history. People of all ages were moving for myriad reasons, whether it was to return to their hometown, move to a city they’ve always wanted to live in, or find a place where they could live with some bang for their buck. For millennials, in particular, the aforementioned survey showed the No. 1 reason the cohort said they were considering moving out of their current town was “I’m looking for more affordable housing.” Some other reasons include the desire for a home with a bigger yard and looking for a change and better employment opportunities—tied for No. 3.

Motivation: In the Zonda division president survey conducted in December, it was found that 55% of builders reported their out-of-state buyers increased compared with last year. That was very location dependent, however. In the Midwest, it was only 18% compared with 73% when looking at the Southeast. Relocation buyers are particularly driven by space, flexibility, affordability, looking for a change, and tax reasons.

Impact on overall inventory: This answer depends on more factors than most of the other buyer groups. If someone is leaving a more expensive market to find more affordable housing, they could be leaving a rental to buy a home, dragging on the inventory. Historically, we know people moving to top migration markets, like Austin, Texas; Phoenix; Las Vegas; Raleigh, North Carolina; and Jacksonville, Florida, often rent before they own. Throughout last year and into 2021, some of those initial renters converted to homeowners. Many of today’s movers are skipping the renting step to lock in the low interest rates. Besides renters, some of the movers may sell a home to buy a home, while, again, the most financially stable may keep their first home and buy a different one.

Risks: Like the second-home buyer, some of this demand was pulled forward in 2020 when the shock of the change was top of mind. We estimate we are over halfway through full-time work from home for those who are able, so we believe this demand will carry on in 2021, but will likely fall back to more “normal” patterns in the vaccine economy. In addition, an unintended consequence of the relocation trends is the new buyers are driving up home prices in often lower-cost areas, which is hurting affordability for locals living on relatively lower incomes.

The question we get most often from clients is: How long will this demand rush last? The current intangible is how to measure the hype. Beyond the demographic strength, the frenzy around the housing market is breeding more frenzy. This is motivating every main buyer group, and we are left wondering what tempers the enthusiasm. As displayed, however, there are many reasons to be excited about the demand-fueled rally in the housing market, including a permanent shift of more people working at home part time, but we also believe some buyer groups are at more risk than others for slowing down especially as affordability gets stretched.