Adobe Stock

Demographic tailwinds are a key reason to be bullish about future housing demand, and no group is more important than millennials. Understanding millennials, defined here as those born between 1980 and 2000, is vital for determining housing demand. Zonda’s economics team has surveyed the cohort for the past five years and provides the findings from the latest report, which covers answers from roughly 1,000 millennial respondents across the U.S. from November 2020 to April 2021.

The Basics

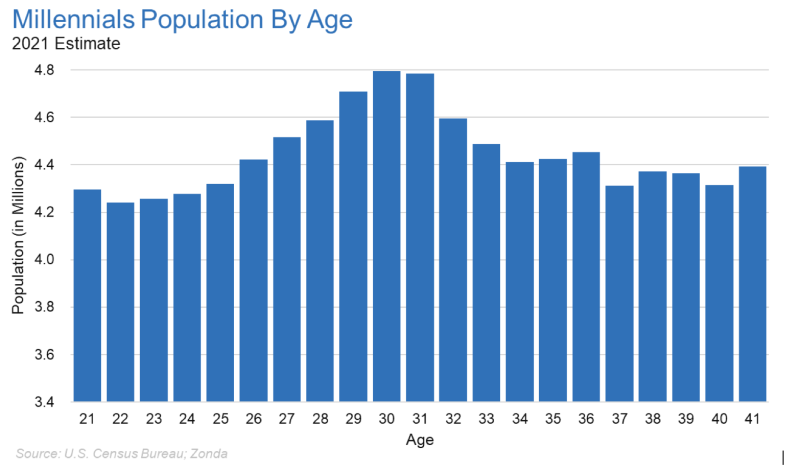

The age distribution of millennials is most concentrated at 30 and 31 years old. This is an important note because, according to wedding website The Knot, the average age for marriage in 2020 was 32. Marriage and homeownership often go hand in hand.

The ability to buy a home, however, comes down to one thing: money. Four of the top five reasons millennials are still renting are related to affordability, led by the inability to afford a home, no down payment, and student loan debt. In fact, the homeownership rate today for those younger than 35 (38.1%) is below where it was 20 years ago (40.5%), and under the 30-year historical average.

A silver lining of the pandemic is that the finances for many in this generation either stayed the same or improved over the past year. For example, 42% of millennials surveyed by Zonda reported that their income increased compared with last year. Furthermore, 60% said they saved more money in 2020 compared with 2019. The savings happened for many reasons, including a change of habits because of the pandemic, stimulus checks, and student loan forbearance.

Millennials reported their top priority was to continue to save as much money as possible, followed by using their savings for a down payment on a home. From our survey:

- 17% of millennials are planning to buy a home over the next one to three years. Extrapolating from the results, that means nearly 16 million millennials are considering buying a home in the near future, or roughly 5 million a year. However, we recognize that there is likely a difference between intent and reality.

- 7% of millennials (6.5M) are trying to buy as soon as possible but limited inventory is slowing their purchase.

- An additional 27%, or an extrapolated 25 million millennials, are unsure when they are going to buy.

- Only 7% said they plan on never owning a home.

While many millennials reported improved finances over the past year, 15% of those surveyed, or an extrapolated 14 million people, said their newfound savings isn’t enough to buy a home yet.

Millennials in the Housing Market

It’s important for builders, especially on the sales and marketing side, to understand why millennials are buying in the first place. Below are the top five reasons millennial homeowners cited for their purchase. Note: It’s a mix of personal and financial reasons.

- Customization. Wanting the ability to make somewhere their own.

- Put down roots. Wanted to settle down and have more stability.

- Housing as an investment. Appreciation/rising home values.

- Math. It turned out it was cheaper to own than rent.

- Pay to yourself. Tired of paying rent.

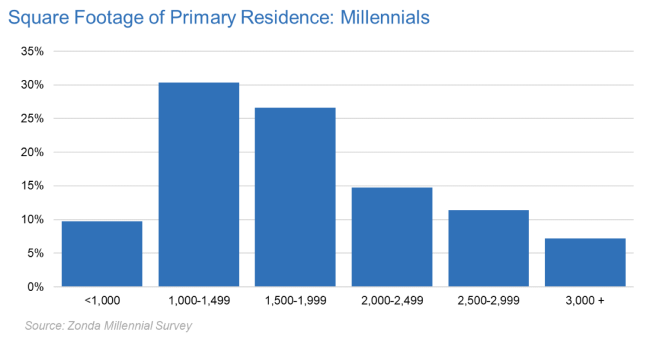

Of the millennial homeowners surveyed by Zonda, the majority live in a home less than 2,000 square feet. The sweet spot for affordability and livability appears to be between 1,000 and 1,999 square feet, with 57% of millennials reporting their home falls within that range. Meanwhile, 26% of millennials report living in a home between 2,000 and 2,999 square feet.

When it comes down to what matters most in the home, both homeowners and renters reported that a large kitchen was of the utmost importance. A large kitchen ranks almost two times above the second-most reported answer, a garage. A functional backyard with space for socializing landed as the third highest priority in the home.

COVID-19 Changes

Millennials are among the most mobile cohort given the propensity to rent, flexibility that comes with either no kids or young kids, and a greater willingness to change jobs. Even before the pandemic, 41% were seriously considering leaving their current city. The pandemic started what we call “migration mania,” where an additional 8% of millennials reported seriously considering leaving their city and 6% moved over the past year. The top reasons were virtually identical across age groups: a search for more affordable housing, better employment opportunities, and a bigger yard. The only exception among the millennial age buckets came from those aged 21 to 26 whose No. 2 reason was to be closer to family.

A noteworthy shift in the migration trends is that those aged 27 to 36 were the most likely to move before the pandemic, but now 37- to 41-year-olds—more likely to be existing homeowners—reported the most interest in moving. The shift matches what we’ve seen on the builder side, where move-up buyers are the most active shoppers, followed by first-time buyers.

For the fifth year running, most millennials reported living 11 to 30 minutes from work. We classify this as “close-in suburbs.” Additionally, and unsurprisingly, the latest data captures the work-from-home trend.

- 45% of our respondents reported working from home over the past year, up substantially from the 11% pre-pandemic.

- 18% of those that are working from home reported that they are doing so because of the pandemic and expect to fully return to the office upon full reopening.

- 14% of those working from home reporting they are doing so because of the pandemic and do not plan to fully return to the office. This group should be of most interest to the home building industry.

The demographic tailwinds that were driving housing before the pandemic have only been exaggerated over the past year. With a larger number of millennials working from home, looking to move, and interested in buying a home in the near future, there are reasons to be optimistic about demand. Hearing directly from millennials, however, surfaces a lingering issue: affordability. Affordability concerns permeated the survey ranging from the ability to own to where people live. As we plan for the demographic-driven demand, we need to stay focused on identifying the right product for a rising mortgage rate and price environment.