The question is rhetorical, and many of you have heard it.

Paraphrased, it’s this. “How can American builders continue to [stick-] build homes largely the way they have done so for the past 100 years, when the rest of the world’s builders have moved into a modern era of mostly building home structures in factories, saving labor, waste, and loss of precision and quality?”

By definition, a rhetorical question is posed for dramatic effect rather than to get an answer.

However, here, answers are important.

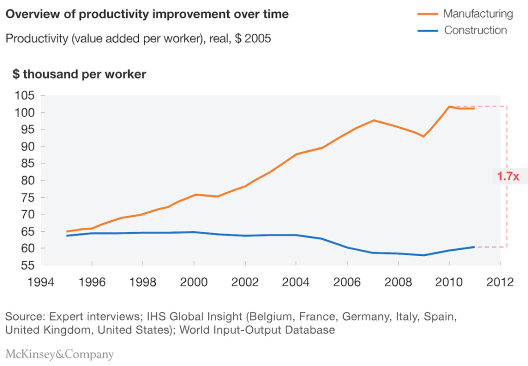

It matters, particularly now, as McKinsey & Co., the firm behind one of the most widely used images in home building and development business presentations of the past 24-months or so–showing construction sadly lagging broad manufacturing industry sectors in measures of business productivity–is out with a new report , new data, and a fresh assertion that “modular construction’s time may finally have come.”

Here’s a link to the report, which you should check out, in part for how important it is as a business community to begin clearly defining, sharing those definitions, and agreeing on them so that every stakeholder using the terms has clarity and consensus on what each means, and why each matters. The McKinsey report does a great job at unpacking those terms, laying them out among visualized operational and business value chains, and probing where there are relational decision sets and where choices need to be made in isolation.

At this moment in the real estate cycle, broader economic dynamics, and the relative [declining] expense investment needed to access to technologies and data necessary to take the reins of a skilled-labor-capacity issue that’s gotten well out of control, a straightforward, plainspoken, easy-to-follow, and inclusive pluses versus minuses analysis for builders of all business-size model is critical.

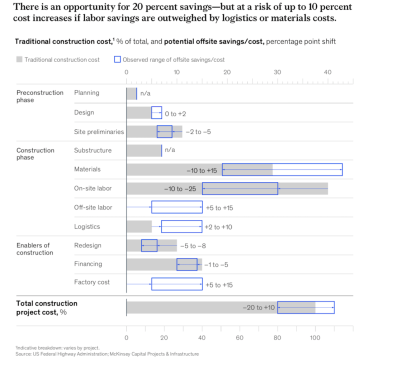

For me, one of the key focal points of the McKinsey study is right here. It’s where the report gets down to quantifying–visually–the potential rewards of a macro pivot by American home builders to offsite construction stacked up against known and foreseeable risks.

Source: McKinsey & Co. "Modular construction: From projects to products."

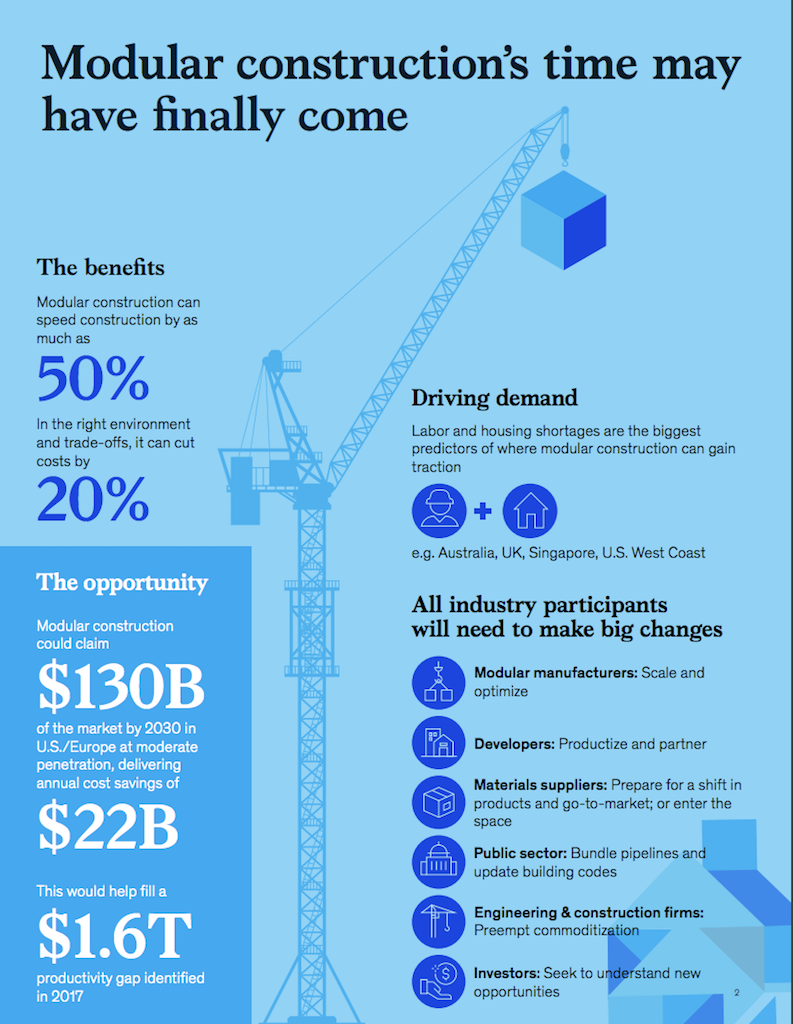

The modular approach […] has the potential to yield significant cost savings, although that is still more the exception than the norm today. As supply-chain players advance along the learning curve, we believe that leading real-estate players that are prepared to make the shift and optimize for scale can realize more than 20 percent in construction-cost savings, with additional potential gains in full-life costs (for instance, through reducing running costs via energy and maintenance savings) (Exhibit 2). Under moderate assumptions of penetration, the market value for modular construction in new real-estate construction alone could reach $130 billion in Europe and the United States by 2030.

Simply, from the looks of it, and from the vantage point of established home building operators at the small to medium-sized to enterprise level, the business performance reward of a successful pivot clocks in at double the downside risk of failing. Said another way, a win in securing the layered benefits of a move to integrate offsite construction into the operational and business model could drop per unit direct inputs costs by as much as 20%. Trying to make the transformation, but doing it unsuccessfully could potentially add 10% to inputs that are already squeezing margins.

Mind you, home building executives aren’t looking at this risk-reward dynamic in isolation, but rather as part of a tangle of equally compelling resource allocation and priority points of focus.

So here’s the rub: few builders can have missed a now-clarion rally to action toward re-flowing operational models to involve more access to factory vs. on-site construction–especially as labor capacity constraints and their severe cost-side ramifications have worsened and can be expected to continue to do so–but they’re now viewed as reactionary because they’re slow on the offsite uptake.

Still, for many builder businessmen and women, the risk-reward spectrum they’re looking at is not a clear slam dunk, particularly as they peer ahead at the future through thicker clouds of uncertainty on economic demand drivers.

Flat out, when they weigh what it would take to migrate their operations to a model that makes a full move to sourcing factory-based pre-constructed structural wall, flooring, and roofing panels, for instance, the gains strike them as theoretical, while the losses would be real and potentially crippling.

Here’s a way to get some insight into the builders’ business and operations model dilemma.

George S. Day, the Geoffrey T. Boisi Professor Emeritus at the Wharton School of the University of Pennsylvania, and founder of the Mack Institute for Innovation Management at the Wharton School, maps the predicament and a roadmap through it in his Harvard Business Review [a paid content site] piece, “Is It Real? Can We Win? Is It Worth Doing?: Managing Risk and Reward in an Innovation Portfolio.” Check out Dr. Day’s recommendations here.

“Aversion to Big I[nnovation] projects stems from a belief that they are too risky and their rewards (if any) will accrue too far in the future. Certainly the probability of failure rises sharply when a company ventures beyond incremental initiatives within familiar markets. But avoiding risky projects altogether can strangle growth. The solution is to pursue a disciplined, systematic process that will distribute your innovations more evenly across the spectrum of risk.

Two tools, used in tandem, can help companies do this. The first, the risk matrix, will graphically reveal risk exposure across an entire innovation portfolio. The second, the R-W-W (“real, win, worth it”) screen, originated by Dominick (“Don”) M. Schrello, of Long Beach, California, can be used to evaluate individual projects. Versions of the screen have been circulating since the 1980s, and since then a growing roster of companies, including General Electric, Honeywell, Novartis, Millipore, and 3M, have used them to assess business potential and risk exposure in their innovation portfolios; 3M has used R-W-W for more than 1,500 projects. I have expanded the screen and used it to evaluate dozens of projects at four global companies, and I have taught executives and Wharton students how to use it as well.

When builders apply the R-W-W screen, and think about whether re-routing their operational value chain through an offsite pre-construction facility, it’s important that the financial evaluation looking at indirect costs as well as direct inputs. In other words, how much “ultimate cost” might be trapped in current practices and site-building oriented workflows, versus the alternative?

Ryan Melin, co-founder and president of Jacksonville, FL-based ICG–Innovative Construction Group, which is on pace to produce walls, flooring, roofing, and integrated structural elements and components for the equivalent of about 1,700 single-family homes in 2019, calls out some of the important indirect cost impacts of a transition from on-site stick framing to offsite processes.

“Most builders are really good at recognizing their direct costs, managing their intricate relation to one another, and making smart moves to optimize those resources,” says Melin, who started ICG 10 years ago after several years as a regional executive at Stock Building Supply in the Southeast, giving him an immersive lesson in the supply chain and procurement disciplines. “It’s when you start adding up the impact of indirects–dumpster pulls, for instance, more efficient design and engineering processes, and the cost of project supervisors and costs involved in inspections, and the back-office costs of having 50 different purchase orders to process and run through accounts payable from buying separate materials and products versus one lump-sum guaranteed amount to cover structure, engineering, installation, service, and inspections as part of the offering.

“We have to be more efficient every step of the way to deliver the financial value to the builders and developers,” adds Melin, whose focus has been on single-family, but whose business is pivoting to include multifamily in the North Florida and north markets, because they can “ship up to 4 hours” efficiently when it comes to multifamily. “We have to outservice our competition. We’re held to some high expectations.

Melin says that after one test-run with a multifamily developer in North Florida, that same developer captured the metrics and quantified its gains through the pilot project, and has now leaned into offsite for its “reliability” and “predictability,” at a moment those benefits are hard to come by elsewhere.

Builders’ skepticism with regard to taking the full plunge in adapting operations models at the design, engineering, and constuction level to a new role for factories in the pre-production of integrated structural elements–be they walls, roofing, floors, components, and beyond–generally takes three forms.

- One of them applies to their direct costs.

- The other has to do with current relationships with their trades in their submarkets, starting with framing.

- The third concerns the question of what happens when, not if, volume demand caves and these factory facilities’ business dries up, and they go broke and shut down.

Here’s where the new McKinsey analysis comes down on its conclusion that the current cross-current of forces bode a permanent transformation for residential construction.

Several factors lead us to believe that the current renewed interest in modular construction may have staying power in additional markets world- wide, first and foremost due to digitization. The maturing of digital tools has radically changed the modular construction proposition. The design of the different modules, the coordination of the pro- cesses within the construction facility, and the op- timization of the logistics of just-in-time delivery onsite are just some of the enhancements that are changing the modular proposition. The further development of these tools, including automated design, will further enhance the modular propo- sition. For example, Katerra uses an integrated technology platform across the construction value chain—solutions include global enterprise resource planning (ERP) deployment, and other industrial Internet of Things tools. The company utilizes building information modeling to directly reach its global supply chain infrastructure for ease of ordering, tracking, and manufacturing. Quality assurance in-factory reduces resources and process time, while mining advanced analytics helps to optimize productivity onsite. Additionally, some companies are successfully challenging the preconceptions of prefab housing as low-quality, prompting a change in consumer perceptions. These companies are offering high- end homes, often with a modernist look and an emphasis on sustainability. Some use residential designs by “starchitects”, and have even ap- peared on the pages of Architectural Digest and Dwell.

In bygone times, builders might have expected that housing boom-and-bust cycles would continuously revert to business conditions where at least two, if not three, of the following key resources, could be procured inexpensively: labor, lots, and lending.

While some of those dynamics may continue to play out, the kinds of pricing resets builders can expect when land costs carry more and more regulatory weight and when laborers are exiting out far faster than they’re onboarding and training up won’t measure up to the financial advantages those “bust” cycles offered in times past.

Now it’s up to cheaper microprocessing power, cheaper sensors, and cheaper data points to offset scarcity premiums the future will place on lots, labor, and lending.

This time is different.