Big mergers and acquisitions stories in home building are always at least two big stories.

One is about the deal itself, and the other is about M&A, consolidation, concentration, who’s for sale, who’s buying, etc., writ large.

This one, the $2.4 billion combination announced yesterday as Taylor Morrison agreed to purchase William Lyon Homes, is no different. It’s a relatively rare, public-to-public merger by one of home building’s more dynamic organizations of the past five years, with implications for both public peers and privately-owned players who happen to play in Taylor Morrison’s suddenly massive footprint of markets stretching from coast to coast.

We’ll take a look here at both the strategic merits of the Taylor Morrison-William Lyon combination, and we’ll also ask some questions and speculate a bit on what the end of 2019 mega-merger means in the world of single-family high-volume housing and community development, and why that matters for other decision-makers, investors, operators, and myriad partners in new residential construction.

For starters, here’s the gist of yesterday’s announcement:

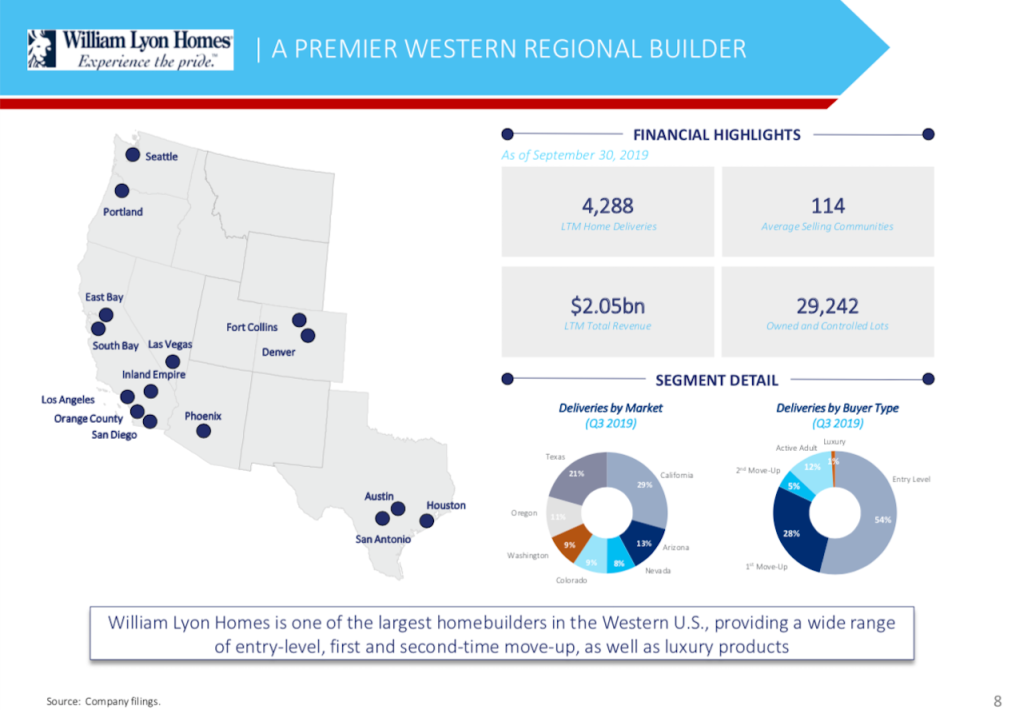

In a deal that would enable Taylor Morrison to leapfrog KB Home into the No. 5 position in our Builder 100 rankings, Taylor Morrison announced its agreement to purchase a primarily western and southwestern mega-regional home builder and community developer, 65-year-old William Lyon Homes.

The deal values William Lyon Homes at $2.4 billion in cash ($2.50/share) and stock (0.800 shares of TMHC common stock). That implies a company value for William Lyon Homes of $21.45 per share or $2.4 billion, including assumption of debt. This yields a purchase price multiple of 1-times book value.

Here are a few of the other points acquirer Taylor Morrison talked up to investors and analysts in yesterday’s announcement of the deal:

- Significant value creation potential for all our stakeholders, including earnings accretion from $80mm of run-rate synergies and optimizing WLH assets

- Management will leverage TM’s proven M&A and integration track record to deliver results

- Strong cultural alignment and timely communication will facilitate a smooth integration process

Source: Taylor Morrison Homes Investor Relations

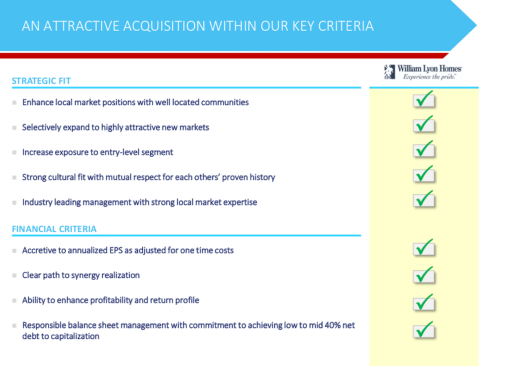

Sheryl Palmer, CEO of Taylor Morrison, told me the combination is the right fit at the right time, for a company that’s been growing fast with six meaningful acquisitions since its record-breaking IPO in 2013, and learning the art and science of integration, right through its purchase of AV Homes last June.

“This checks all the boxes, taking us into new markets, complementing what we’re offering and adding land and community pipeline in markets we’re in, and giving us greater exposure to the entry-level buyer,” says Palmer. “Where we felt the urgency, and where this combination felt so right, was that we now are strong top 5 players in Southern California and Northern California markets, and Denver, where we’ve been short on land inventory, and we’re entering the Pacific Northwest just as the market has moved off its peak pricing. We’re now in the right place, at the right time for the right price.”

Source: Taylor Morrison Investor Relations

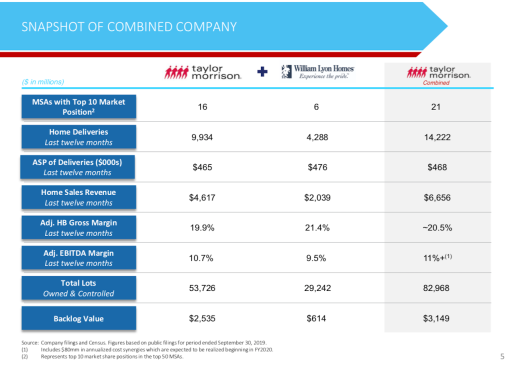

Pro forma-ed to reflect the combined businesses, Taylor Morrison’s heft increases by about 50%, with increased exposure to entry-level buyers up from about 28% to 36%, and when you add in first-time move-up buyers, it’s a full three-quarters of the product and pricing offerings of the combined company.

“For us to make a bet of this nature on an organization that makes us 50% bigger the day we close than we were, we couldn’t be any happier or more honored that it’s a company and a family whose name means so much in home building,” Palmer adds. “We’re really looking forward to welcoming the William Lyon team into a Taylor Morrison business culture we’ve worked really hard on and are so proud of.”

William Lyon Homes branded communities will mostly convert to the Taylor Morrison flagship brand in the months ahead, with the exception of the William Lyon Signature collection of homes and communities, Palmer says. Further, evaluation of the Polygon North brands currently operating under William Lyon Homes in the Northwest will occur.

Now, let’s take away some high-level ramifications of the deal, which coming as it has in November, signals that the moment is ripe for M&A activity in the current economic environment. Why?

- One of Sheryl Palmer’s points about timing is that, after 2018’s big–possibly temporary–backslide in momentum and continued talk of the possibility of a 2020 recession, acquisition target prices may have moved off their peak levels.

- Too, the Fed’s signals that it may have reached an equilibrium level for its prime lending rates–which account for a low cost of capital that may not go lower–may also factor in deal flow timing.

- Three, cost of capital in Japan, China, and Canada, from which we’ve seen a number of strategic buyers in the past several years, continues to be even lower than it is for those who access the U.S. debt markets.

- Four, as signs come clearer that there may be continued headroom for U.S. housing momentum–especially if builders and developers can bend the buyers’ cost curves lower and open up the homeownership universe to more first-time and entry-level customers–big players suddenly have a renewed appetite for extended land pipelines, deeper local scale, and more lower-priced product offerings for their portfolios.

- Five, as was evident in word yesterday that Berkshire Hathaway unit Clayton Properties has continued a six-year expansion surge in single-family site-build acquisitions, with the addition of Louisville, KY-based Elite Homes under Indianapolis-based Arbor Homes tent. Clayton has laid out a massive, Colorado-to-East Coast footprint of single-family site-build operators within an even vaster coast-to-coast infrastructure of manufactured home production and distribution facilities.

Ceo Warren Buffett doesn’t play up a vertical integration strategy intention for the Berkshire Hathaway portfolio of operating units. Still, when you look at the housing and real estate and construction and technology and manufacturing and materials supply and distribution and housing services-related nature of the B-H portfolio, it’s one of the most vertically integrated non-vertically integrated strategies imaginable.

As Buffett said earlier of Clayton’s single-family home operator acquisitions, “more will come.” It’s also worthy of mention that Clayton Properties ceo Kevin Clayton is mission-driven around his organization’s part in making the American Dream of homeownership attainable to working people as it is so far from being the case today. So, the firm’s continued build-out of a national entry-level footprint is far from complete.

Now, those five factors speak to the environment and key motivators for strategic would-be acquirers to pull the trigger on M&A deals that they have been cultivating for some time.

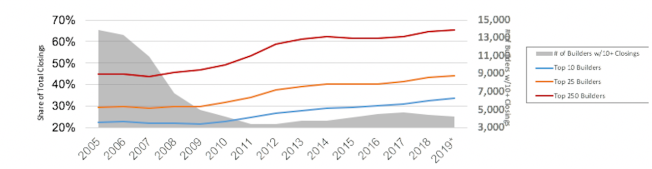

Let’s review a few of the would-be seller motivators, particularly in the 2019 “red-zone” period, where economic, consumer sentiment, employment, international trade, political turmoil and demographic signals and noise are doing their best imitations of one another. The macro trend to keep in mind here is that the home building world, as we’ve known it, is shrinking, ever more concentrated, ever more consolidated, where fewer more powerful players account for a greater and greater volume of new home sales activity.

Source: Metrostudy, BUILDER analysis

Small-cap publics–namely Green Brick Partners and New Home Company–for different reasons, rank high on many target lists, because their nimbleness and ability to scale their business and operations models are constrained by a shorter leash on capital. This makes it challenging to be agile and long-term value-focused when quarter-to-quarter financial interests carry so much weight. It would not be a surprise to hear that Green Brick may be of interest among a number of publics, some of whose need for Texas land assets may be greater than others’.

Ten-year-old New Home would be a fit and a prize for publics who want to add or strengthen relationships with higher-end customers in highly land-constrained, mostly coastal, markets. New Home has also relatively quietly diversified its spectrum of offerings, and has moved aggressively into entry-level price points with high-concept, high-design models that address the “attainability” crisis in California and other supply-constrained markets.

Private home builders with a top 10 “Local Leaders” position in any of the top markets, and with strong exposure to entry-level or first-time move-up buyers may look at now as a moment to sell, if only to access the kind of capital they don’t have but will need if they want to go back into land-acquisition and development mode after taking some of those chips off the table earlier during the Recession Scare of a few months ago.

Lastly, age demographics is also a motivator. Many private companies are family-run, by principals who’ve reached “a certain age,” and may need a succession plan that doesn’t involve passing the company down to a son or daughter. We’ll continue to see and hear of this as a factor in some of the transaction activity ahead.

In all, it may not be one of the busiest M&A periods in terms of the volume of deals, but we’ll certainly see more deals, and report to you what we learn of them, in the weeks ahead leading to the end of the second decade of the 21st century.