High prices and scarce supply–in for-sale and rental homes–weigh on demand. They the would-be renter from forming a household. They delay an intended home buyer, especially in a tightly regulated mortgage credit environment, because prices and expenses beyond their limit are simply beyond their limit. They’re excluded from participating.

It begs the question, would the simple fact of more inventory, more units available for rent or for sale, lower prices, expand the size of the universe of capable renters and buyers, and accelerate growth?

That’s what most housing experts and economists believe. And if that’s really the case, then given today’s conditions, you have to ask–and possibly worry–about an effect opposite to accelerated growth.

What if keeping a tight lid–of high prices and scarce supply–on demand does not simply add to a pool of pent-up demand, but rather, starts to smother it?

Or causes it to find other outlets, like doubling-up, or remodeling existing homes, or co-living?

In other words, is suppressing today’s demand corralling people into a sub-universe of pent-up demand for rental and ownership opportunity at some near-term future moment? Or, by dousing their fervor today, is the market signalling to those folks, “go away, you have no place here.”

A question like that is hard to answer. Yogi Berra said it. “It’s tough to make predictions, especially about the future.”

And this question, particularly, has a chicken and egg quality about it, because it’s challenging to figure out the difference of when more supply begets more demand and when more supply just turns into oversupply.

Ivy Zelman and her team of Zelman & Associates analysts explore this phenomenon in the latest The Z Report, under the title “Could Tight For-Sale Inventory Depress Consumer Enthusiasm Shortly?” For a free trial of The Z Report, click on this link.

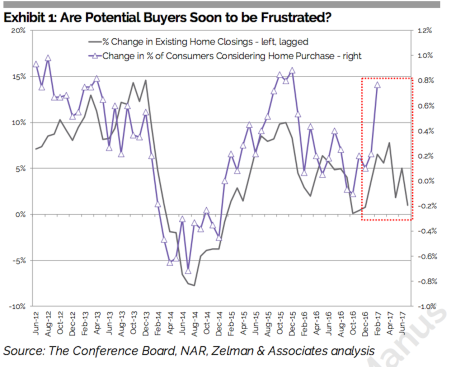

The Zelman take on the numbers looks at the relationship over time between National Association of Realtors’ existing home transactions data and The Conference Board’s metric tracking consumers who intend to buy a home within the following six month period.

Here’s the kicker:

“We delve deeper into the comparison of these two ratios dating back to the start of the housing recovery in early 2012. Interestingly, the strongest correlation (83%) between consumer intentions and existing home sales growth is on an eight-month lag, with existing home sales being the leading indicator. In other words, actual transactions and a healthy market give rise to consumer interest in purchasing a home. This is the exact opposite relationship than one would anticipate.”

The current moment may come down to an odd reality, that a prevailing fear of oversupply self-fulfills a prophecy of oversupply by stifling demand, not only in the present but among future would-be renters and home buyers.

That’s where one would hope to turn to data for answers. Probably it’s the case that at an individual organization level, decision-making among strategists and investors is impacted to a more significant level by that fear of oversupply. Exposure to an oversupplied market can be harmful or fatal at the micro, enterprise level.

At the same time, the collective benefit that could spring from a normalized supply and demand in the market is not–so far–sufficient to offset the risk of individual exposure. A tide that conceivably could lift many, if not all, ships, is being held back by each company’s hesitancy to risk getting too far out over their skiis on land and development.

So, instead, a slow, painstaking dig out continues. Unless, of course, something gives.