Thirty-five.

That’s how old the eldest of a 75 million strong generation of Americans known as Millennials–the youngest of whom will turn 19 in 2016–will be in the next 12 month stretch.

As a matter of fact, Millennials—the crop of people born between 1981 and 1997–this past year surpassed the Baby Boom as the United States’ largest population cohort, a wave of relatively new and emerging households that, we expect, will reshape economic , business, and geographic marketplaces for decades to come.

http://www.pewresearch.org/files/2015/01/FT_15.01.15_line.png ]

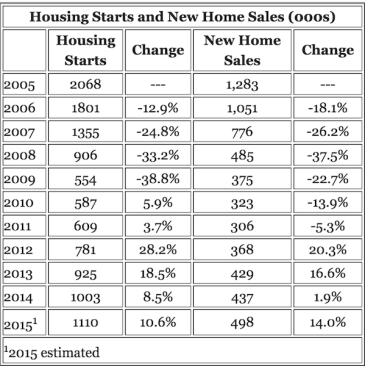

As we move into 2016, both broad economic and housing trends continue to throw off mixed—headwind vs. tailwind—signals. Uncertainty, particularly as to the timing, geography, and trajectories of recovery in America’s housing markets, make the next 12 to 48 months a critical time period in housing’s rebound. To return to multi-decade norms, housing starts will need to increase by 40% or so, and new-home single-family sales will need to almost double from current levels of just-shy of half a million.

http://www.calculatedriskblog.com/2015/12/question-8-for-2016-how-much-will.html ]

Is the data on your side?

First-time home buyers—many of whom fall into the young adult age range that matches up to the leading edge of the Millennial cohort—represent less than three of every 10 home buyers, well below the norm of 40%, according to the National Association of Realtors.

Fact is, in prior housing recoveries following recession, new homes, and specifically new homes purchased by young adults have played a big role as both a catalyst and sustaining force in broader economic revivals in the United States.

This analysis aims at three principal goals.

One, is to troll and filter through the tomes of data for the most relevant, clarifying, and helpful insights defining what we mean by the term “Millennial,” who they are, and what their attitudes, preferences, financial capabilities and constraints, and values are where it comes to their living situation selections, now and in the near-term future.

Second, we’ll explore scenarios for success. We’ll take a look at how 2016 and the three-to-five year period ahead may play out, assuming that best practices among residential developers and home builders favorably influence, impact, and “activate” the Millennial adult buyer into new-home communities.

Finally, we’ll drill down to what those best practices are, and how home builders can put them into action. We’ll look at the precision with which land position and lot development options can occur; the power of compelling design’s role in motivating young adult buyers; and the purpose of unprecedented new partnerships between builders and manufacturers to meaningfully elevate value to a point where Millennials must say “yes” to the opportunity to own a new home now.

For the first two objectives, we’ll draw from a spectrum of resources and sources of intelligence, including Hanley Wood’s own Metrostudy analytics knowledge base and regional network of residential market specialists.

For the third goal, we have a unique and exclusive opportunity to dive into a year-long learning and development process whose specific intention has been to discover how home builders and their partners can locate, develop, design, build, finance, merchandise, and market new homes for this new wave of young adults.

The 2016 BUILDER Concept Responsive Homes from TRI Pointe Group’s Pardee Homes Las Vegas division has become a 12-month, multi-million dollar discovery lab for research and development on essential new practices to identify, message, and acquire home buyers in the Millennial generation, now and over the next several years as they come of home-buying age.

The project indeed has led to both discovery and opportunity to try out—in concept, schematic, design development, and construction—some wholly new approaches to understanding and activating young adult buyers, by deliberating lowering some of the barriers to their purchase and by elevating their sense of how a home can be personalized, customized, and adapted to their needs over time.

Let’s run through the preliminaries, shall we? Then we can zero in on the take-aways of the Pardee Homes Responsive Home(s) two houses, and what they can do to help builders attract and win-over Millennials in their own markets.

Millennials: The “Who?”

Millennial is the nick-name given by marketing and management consulting companies to characterize a population of young and emerging adults born between the years 1981 and 1997. Initially, early-comers in this generation took on broad-brush characterizations that reference prior generations. “Echo-boomers,” for instance, harkens to their being the children, in most cases, of Baby Boomers and Generation Y (Gen Y, for short) comes of their arriving on the heels, generationally speaking of the vaunted Generation X, which encompassed the 15-year stretch from 1965 to 1980.

Millennials, you see, “came of age” as the 1990s became the 2000s, and in so crossing the threshold of a new millennium.

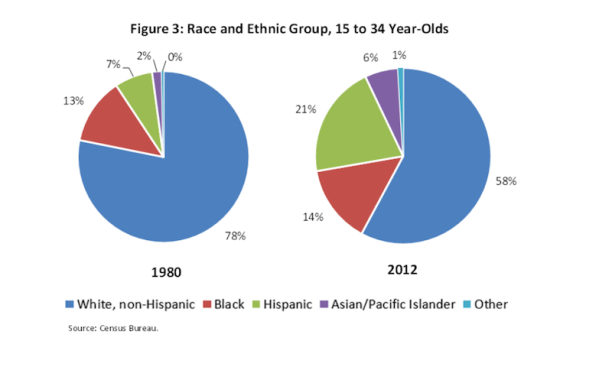

Other than the sheer size of the population, one of the more pertinent demographic facts about this cohort of Americans is the cultural diversification—assuming, as we do, that cultural heritage impacts consumer behaviors in various parts of the consumption funnel.

Here, from a White House analysis of Census Bureau data, is a look at the dramatic changes in race and ethnic make-up for the age 15 to 34 group, contrasting 1980 with 2012.

Fast-forward to the present, and this generation, the very first generation of digital natives, had their attitudes and understanding of the world around them shaped around technology-enabled online access, connection, and community; around the notion that gratification and instant gratification are one and the same; and around the idea that if something could be imagined, it could not only be, but it could be had.

Much has been written and much more could be said of how Millennials’ “coming of age” engrained preferences and values that set them apart from prior generational cohorts flowing through their respective early-adult lifestage.

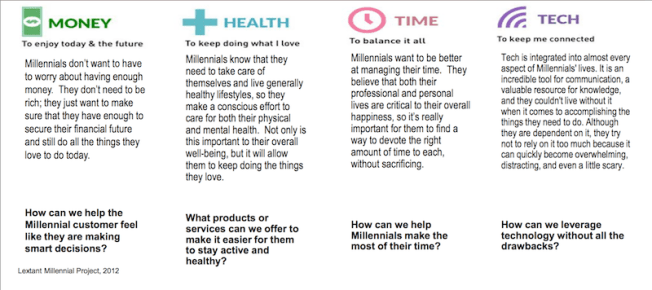

Here’s helpful learning from Whirlpool, which tapped Lextant’s 2012 Millennial Project to identify four distinctive “motivators” underlying their buying behavior.

This may be a true, and helpful lens through which marketers, residential developers and home builders may look for resonance among today’s generation of young adult potential home buyers.

Still, isn’t it also true, as the authors of “Stop Designing for Millennials,” a recent Harvard Business Review analysis Timothy Morey and Allison Shoop assert, that “applying a generational lens can backfire?” Morey and Shoop, (of frog, a global design firm), write:

The history of product design is littered with [similar] examples that fail to take into account that emotions, wants, and needs of people vary greatly within and across generations.

A better approach is to design for archetypes that are representative of certain attitudinal and behavioral traits, and then combine these with social, market and emerging technology trends—all things that transcend age or generation. Defining an ideal customer for a potential product or service using broader human themes allows you to create solutions that resonate with a larger group of people.

In other words, generational psychographics notwithstanding, people want roughly the same things across generational cohort dividing lines. So, more productively, as regards young adults funneling toward their own decisions on forming and committing themselves around households and housing preferences, let us zero-in on those “social, market and emerging technology trends” so that we can map young adults’ evolving needs to the solutions they bring to bear in meeting them.

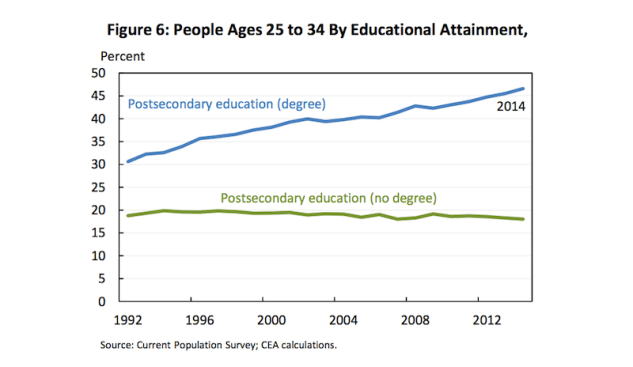

Two critically important shapers of evolving need among young adults have money as the common denominator: what they owe, and their capacity to earn. Defining traits of this younger adult generation vs. its predecessors are that they’re more educated, in greater debt coming out of college and graduate school, and, thereby, may enjoy higher earnings in their careers—once the economy has restored jobs and income opportunity in broad terms. According to the U.S. Treasury, college-educated Millennials are more likely to earn higher wages and be employed than those without a college degree. A four-year degree yields approximately $570,000 more in lifetime earnings than a high school diploma alone, while a two-year degree yields $170,000 more.

Let’s look back at the White House study on Millennials, at the “investment in human capital” this generation (and its parents) have made, vs. prior generations.

The price tag for this huge human capital investment has been and will continue to be a headline-grabber, for as a result—in absolute terms—the debt-load borne by today’s college and post-graduate young adults is staggering. From the White House study, we note:

Total student outstanding loan debt surpassed $1 trillion by the end of the second quarter of 2014, making it the second largest category of household debt. In part, this increase in the aggregate level of outstanding student debt is due to greater enrollment among Millennials and to the changing composition of students, including a larger share of students from lower-income families who need to take out more loans, as discussed in Fact 4. Other contributing factors include: rising tuition as state governments have cut funding; parents’ impaired ability to use the equity in their homes to offset some portion of their children’s college costs; and the fact that students are taking longer to repay their loans. Consistent with these factors, average real per borrower debt increased from $24,000 in 2004 to $30,000 in 2012.

Of course, the other side of the debt-load coin is the relative ease, or difficulty in this case, and timing of the repayment of this debt as the result of earnings capacity once graduates take hold of their degrees and enter the work force.

That too has been an area of unprecedented challenge for our current crop of new and emerging young adults. Going back to the White House analysis of Millennials:

The Great Recession likely will have important implications for Millennials’ future labor force outcomes, since research finds that macroeconomic conditions in childhood and young adulthood are important determinants of future earnings and financial behavior. Early career economic conditions have large and lasting impacts on lifetime wages, particularly for college graduates. Research shows that entering the labor market during a recession can result in substantial earnings losses that persist for more than a decade, with negative effects lasting longer for college graduates. 40 Workers who start their careers in a recession earn 2.5 to 9 percent less per year than those who do not for at least 15 years after starting a career. Research further suggests that one reason for these lower earnings is that new entrants take jobs that are a worse fit for them when they start their careers in a recession.

So, encumbered by debt from the get-go, and challenged by a jobs and wage environment that has been inordinately inhospitable, you might think that our young adult segment would report a pessimistic outlook on their eventual access to what they value and want in their lives. This could not be farther from the truth.

We’ll get to that, but let’s take a look first at a couple of the important adaptations or “coping mechanisms” Millennials have turned to as they begin to navigate their way into the realities of adult life in an era defined by economic adversity, technological wizardry, and entrepreneurial strides that have begun to define the sharing and “gig” economy.

Note that it is in exploring how these adaptations, coping mechanisms and needs, that residential neighborhood developers and home builders can begin to conceptualize, design, develop and build houses and communities that meet these needs.

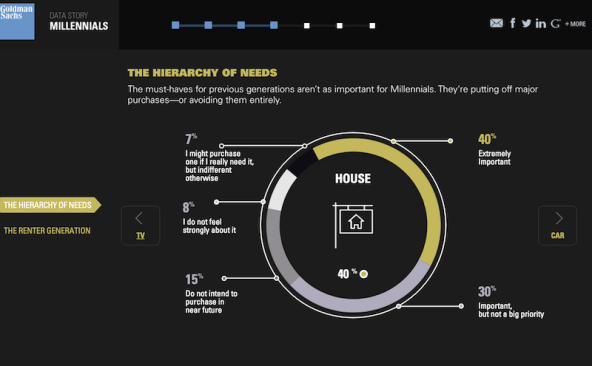

For instance, this Goldman Sachs analysis offers a stark, precise illustration in point, of how, collectively, Millennials have coped with their particular set of financial straits, and the opportunities that have grown up around that coping.

http://www.goldmansachs.com/our-thinking/pages/millennials/

The context of access vs. ownership is clearly at work in another, absolutely critical, dimension of young adults’ coming-of-age behavior, the formation of their own households, and pipeline into homeownership.

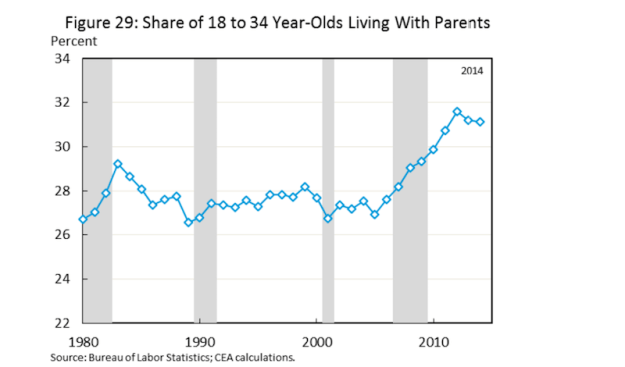

Again, returning momentarily to the White House Council of Economic Advisors analysis on Millennials, we observe the cause of all the media hype around 18-to-34 year-old rates of living with mom and dad.

Commentary from the CEA notes:

Entering adulthood during the Great Recession and recovery has not only affected Millennials’ schooling and employment decisions, but also their housing and household formation patterns. In the aftermath of the Great Recession, the share of 18 to 34 year-olds living with their parents increased from 28 percent in 2007 to 31 percent in 2014–which is a notable increase even if the actual magnitude falls well short of some popular perceptions. Correspondingly, the pace of household formation is low and the “headship rate” among Millennials – the rate at which Millennials head their own households – has fallen.

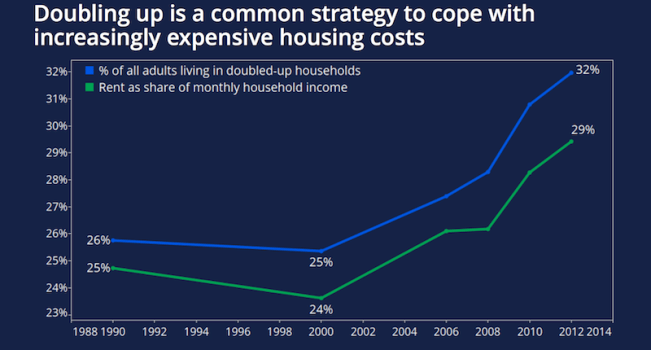

“Doubling-up” in living situations, whether it’s with one’s parents or with other housemates or roommates, has definitely had an impact seen in the lagging rates of household formation since the Great Recession, again tracing to those two enormous financial pain-points weighing on and slowing down the progress of many young adults in their housing decision-chain.

Housing analyst and former Trulia chief economist Jed Kolko takes a deeper-than-usual dive into the question of “Why Millennials Still Live With Their Parents,” and concludes that the housing bust and recession do not fully explain the reasons grown adults choose to live with their parents—it’s actually a long-trending demographic pattern. Kolko writes:

The decline in young adults being married with kids long pre-dates the recession and the rise in living with parents, and has been relatively steady for decades (see chart above). That means marrying later is not the effect of the post-2005 increase in living with parents.

Cause and effect may be uncertain here, and, if Kolko is right, the 1981-to-1997 set of 75 million 35-year-olds and younger may either choose to or have to live with parents or doubled-up for longer than prior generations because that’s part of a longstanding decline in younger-adult headship rates.

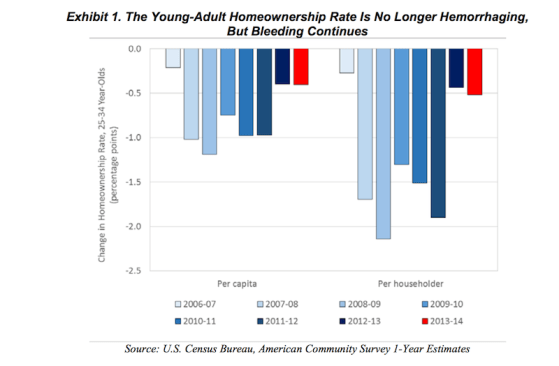

Another point of view, however, looks at the slowing rate of decline in young adult household formation and homeownership rates as a possible pre-indicator that the decline itself may zero-out and even shift into a positive rate of change.

Patrick Simmons, director of strategic planning for the Economic & Strategic Research Group at Fannie Mae writes this as a relatively conservative middle scenario:

Declines have moderated recently, however, as the number of young homeowners fell by fewer than 100,000 in 2013 and was essentially flat in 2014. Improvement came as the population of 25- to 34-year-olds continued to grow at a healthy clip, while the decline in the young-adult homeownership rate moderated. Given that the young-adult population is expected to continue expanding rapidly during the second half of the decade, it would take only modest further improvements in homeownership rate trends for the number of young homeowners to return to growth. In fact, even if the young-adult homeownership rate simply stabilizes at the current level, projected population growth would generate increases in the number of 25- to 34-year-old homeowners during the second half of the decade that exceed gains registered during the housing boom period of 2000 to 2005.

What Fannie Mae economist Simmons’ scenario at least suggests is this: Demographically, young adult buyers will be an increasingly significant factor in total home sales. What’s more, plausibly, they could amount to a sustainably epic factor with relatively conservative estimated improvements.

The question—and it’s one that even after all the talk about the importance of activating the Millennial buyer segment of the housing market this past year remains—is whether and how residential neighborhood developers and home builders can induce Millennials into “the funnel” of buying a new home.

Is it a matter merely of waiting until external forces create and grow a stream of willing and able buyers? Or can and should developers and builders take an active role in kindling and stoking demand?

Clearly, the strongest case can be made for the new residential business ecosystem of capital sources, land developers, architects, builders, and marketers to act—invest, develop lots, design neighborhoods, create new products, and market new communities specifically to meet the needs of Millennial buyers.

The Millennial Mandate: Why Act Now, Before the Wave Hits?

Here are the most compelling reasons to be proactive, moving dollars, time, talent, and commitment fully into action ahead of the Millennial wave of buyers:

1. They want to own

2. They want to own in the suburbs

3. They want to own new homes that they can attain, personalize, adapt to their needs, and live in a connected, accessible way

Let’s look at these compelling reasons one at a time. First, take a look at the above-mentioned analysis from Goldman Sachs, where its analysts surveyed Millennials on their “hierarchy of needs,” finding homeownership to be among the highest-ranking of priorities.

The data below show that 77% of the respondents regard a home purchase as ranging from important to extremely important, to “I might purchase one if I really need it…”

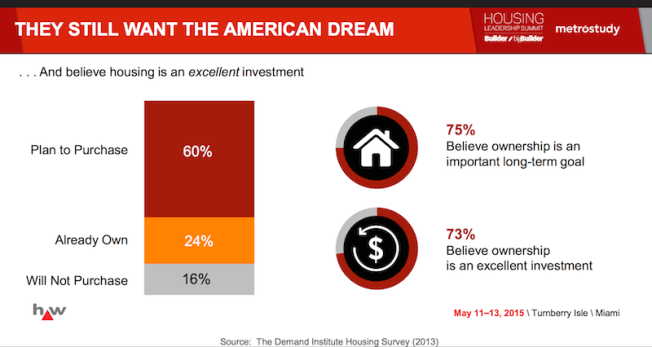

Secondly, from Demand Institute vp and analyst Jeremy Burbank, here is a look at a similar data conclusion, showing that, in a structural sense, The American Dream of homeownership is alive and pulsing among young adults.

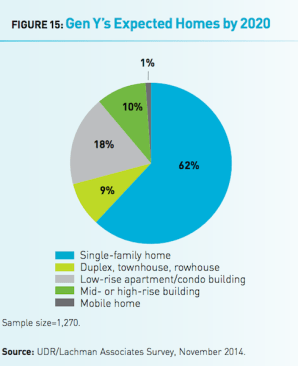

As further evidence, Urban Land Institute survey analysis reached essentially the same conclusion, and added a date as dramatic punctuation of its statement that Millennials may not currently be big time homeowners, but they’re planning to be—soon.

Fully 70 percent of survey participants expect to be homeowners by 2020—even though only 26 percent currently own.

As an interesting side note, ULI data suggests that while more than one in five respondents currently lives with mom and dad, less than 4% plan to be doing so within the same five year period, between now and 2020.

It is abundantly clear that, even adjusted for over-optimism, Millennials want to, prefer to, and intend to work their way past their current financial impediments into homeownership.

The Millennial Opportunity: How to develop, design, and market

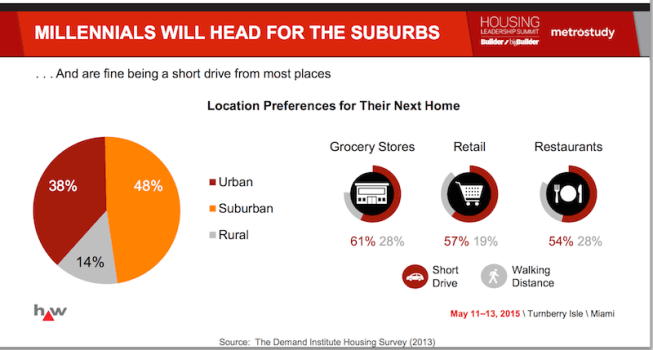

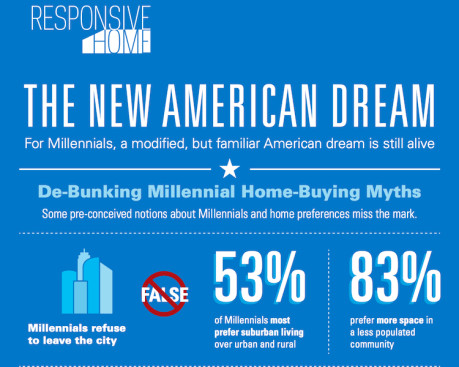

Just as it’s clear that Millennials mean, sooner or later, to be homeowners, what’s also clear is that suburban—not urban—living suits them just fine, despite what may be appearances to the contrary (we’ll address those in a bit).

Here, more Demand Institute Housing Survey data comes into play as we look at Millennials’ preferences about where they intend to settle.

Too, in our own specific research into this dimension for the Pardee Homes Responsive Homes project, BUILDER and the TRI Pointe Group teamed with Ketchum Global Research and Analytics, conducting an online survey among 503 Millennials age 25–34 with a HHI of at least $60K who either intend to purchase a home in the next 12 months, or currently own one.

Among the survey’s chief findings are the age group’s interest in maximizing space and affordability while maintaining a level of community found in urban environments, and capitalizing on opportunities to customize and personalize their homes.

Preference: Urban-Suburban Environment More than half of survey respondents (53%) are eager for a suburban lifestyle, and millennials are four times more likely to opt for more space over living in a populated community. That said, urban benefits of being within walking distance to parks, grocery stores, schools, and work were high priorities for respondents.

Solution–Ideal Location: The Responsive Homes are located in the Inspirada community of Henderson, Nev. Homeowners will be able to take advantage of community amenities and will have a grocery store, coffee shop, pharmacy, bank, dry cleaner, restaurants, and more within walking distance of the Responsive Homes.

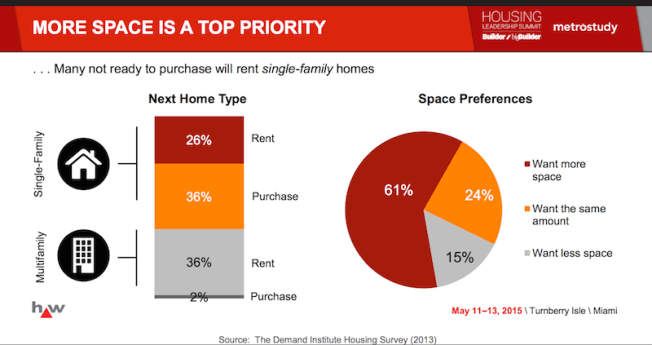

Demand Institute data, again, backs up this conclusion, indicating that Millennials hold a higher priority around “space” in their living situations—and access to connectivity—than actually living in an urban environment.

Readiness to purchase vs. continuing to rent is a big issue here, and one that residential neighborhood developers and builders need to understand precisely as they invest resources in this segment of the market.

Toward the end of 2015, it became evident that early-to-market movers might claim a competitive advantage among home builders, not just by offering lower-priced homes to young adult buyers, but by discovering the development, design, and construction disciplines and processes that would enable them to be profitable in this sphere.

Bloomberg’s Prashant Gopal covered the “Return of the Affordable Starter Home,” in an article that beat-the-clock on the close of the year, concluding:

Following the success this year of D.R. Horton Inc.’s low-cost Express brand [and LGI Homes’ offerings], national firms including Tri Pointe, Taylor Morrison Home Corp. and Meritage Homes Corp. are testing cheaper offerings in markets from Colorado to Florida to California.

Pricing—including the tactics Gopal mentions of reducing home sizes, taking out features such as fireplaces and mudrooms, and locating communities farther from job centers and established higher-end locales—is a critical part of the “how” when it comes to builder best practices, and our Ketchum Global Research and Analytics data proves that out.

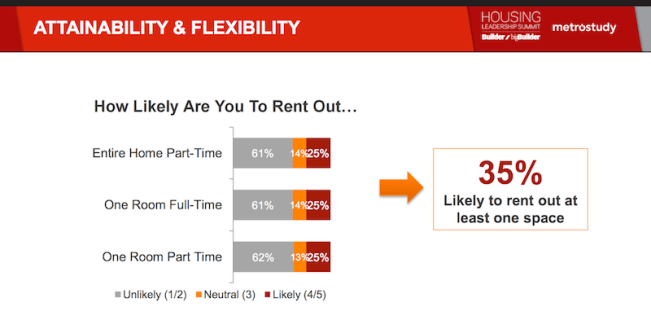

Pricing as a tactic nests itself in a broader notion from buyers’ vantage point: attainability. Attainability takes knowledge of income levels among Millennials in a particular geographical market, and puts financial solutions—beyond the price tag—into play.

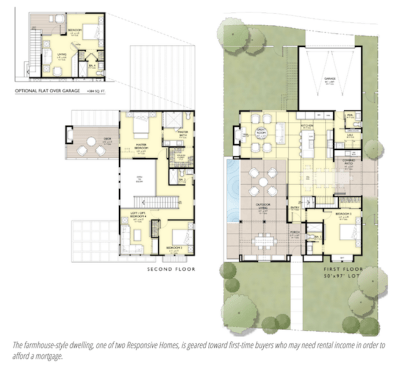

Revenue suites—allowable in the Las Vegas market and in an increasing number of new home building markets around the nation—have emerged as an “attainability” tool for prospective home buyers. The ability to rent out a room, or else comfortably accommodate parents, in-laws, or another generation of relatives on a longer-term basis, gives buyers “attainability” range they may not otherwise have available to them.

Here’s what our Ketchum data showed about what young adults say about the potential of earning revenue as part of their homeownership and finance experience:

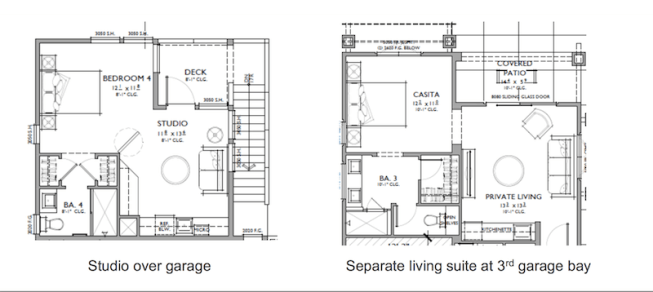

Here are a couple of executions—roughly, what our partner architects Bassenian Lagoni created for the Responsive Homes with data from our research driving the design—that show how revenue suites can work as part of new floor plans for Millennial buyers.

Attainability may work as table-stakes to awaken Millennials to the option and capability that they can own, but it will take more than that to pull them off the sidelines and into the market.

That’s why our TRI Pointe and Pardee partners dove deeper into what motivations would work most powerfully if they were triggered by design, performance, and function in new homes.

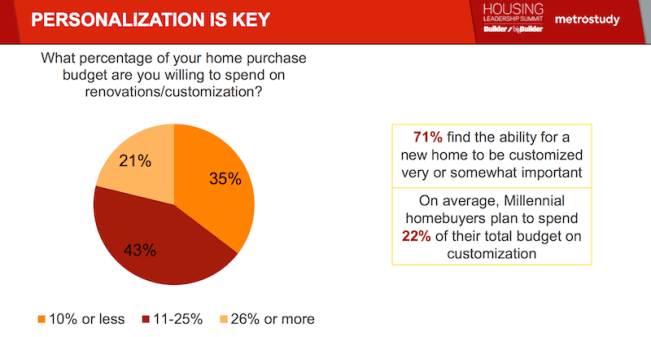

Personalization, a term that means a great deal to young adults who have grown up interacting with digital and technological interfaces for as long as they’ve been alive, becomes such a trigger. As a matter of fact, our research sample base of Millennials, on average told us that they’d spend more than one of every five dollars they’d have available in their budget on renovations that would customize their home to their needs and wants.

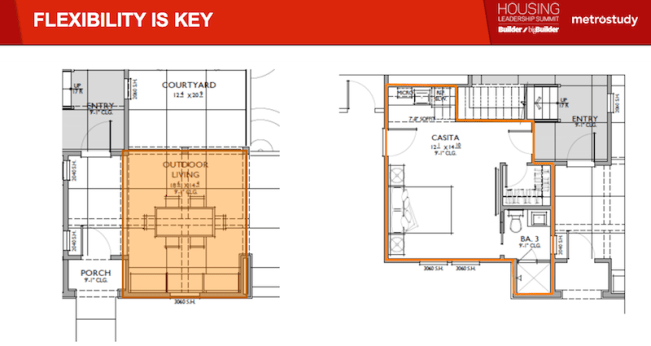

Here’s how builders and their architect partners might look at such an insight, providing flexibility and adaptability in floor plans, space usage, etc. for the near-, medium- and longer term ownership horizons.

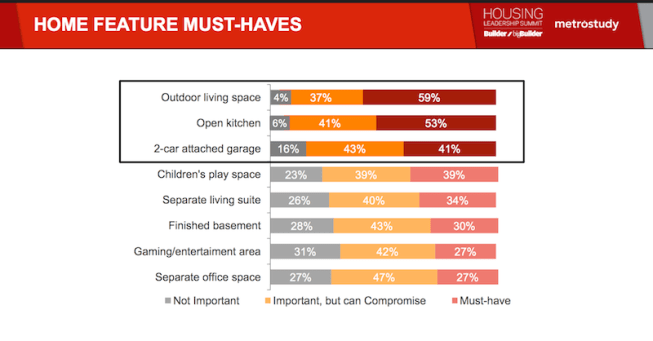

What came across particularly strongly in our research, and in ways that we believe can serve home builders and residential neighborhood developers especially well for design, lot orientation, and land planning purposes is the ranking among our prospects and recent owners of what they regard as “must-have” features.

Here’s a look at that:

Young adult buyers’ affinity with and gravitation to backyard and outdoor living can barely be overstated, which is why architects Bassenian Lagoni pulled out the stops for indoor-outdoor living zones in our Responsive Homes.

So, attainability, personalization, flexibility, connectivity to outdoor living, suburban-cum-urban styling, and become the “how” of residential neighborhood developers and builders designing and marketing to Millennial buyers.

Change occurs when two forces kick into play. One force is the lowering of the barriers preventing that change. The other is to elevate the intention, the will, and the ambition of those who need the change to the level where they see themselves as having it.

Builders and developers can do their part in both. They can, indeed, lower the barriers to entry by working on prices and products and positions of their new homes and communities.

But we believe they can make their new homes attainable in other ways as well, which is what we’ve explored with the Responsive Homes project.

We’ve lowered the barrier to entry, and by designing the homes for personalization, flexibility, and connecting them to access to both community, convenience, nature, and jobs, we’ve also made strides at converting buyers to a higher value proposition.

We hope you’ll find the insights and ideas here ones that you can put into action in your market analysis and development plans.

{kind=link}