During her 13 years with the HBA of Greater Chicago, the executive director Rita Unzner has pushed for broader access to health care insurance for the group’s members. Many of the HBA’s 200 builders can’t afford to offer this benefit to their employees, some of whom “have children with illnesses and other problems that can break families” financially, she says.

In September, the HBA launched an online portal through which builders and employees can apply for health care insurance. It’s modeled after a similar access point the Wisconsin Builders Association set up about a year ago, says the group’s executive vice president, Jerry Deschane. Builders can compare different insurance carriers’ plans and get multiple price quotes. They can also put together their own plan online, the way some automakers allow customers to “build” and customize a new car on their websites.

Unzner thinks the specter of the Patient Protection and Affordable Care Act, which Congress passed in 2010 and whose constitutionality the U.S. Supreme Court upheld last June, may have been what finally nudged the association into action. “The Act made it easier to get this off the ground,” she says.

The do-it-yourself approach to buying health insurance that such programs enable, however, is risky now that the insurance world is being turned upside down by the Affordable Care Act, a/k/a “Obamacare,” with its 2,000-plus pages of rules and regulations, $1.2 trillion price tag, and staggered rollout over the next several years.

The Act’s ambitions are to provide coverage to 30 million uninsured Americans and to expand Medicaid to households earning up to 133 percent of the federal poverty level, by using subsidies, tax credits, and enforceable law. Its key date is Jan. 1, 2014, when all Americans must be insured, either through their employers or by purchasing policies through state- or federal-run exchanges, or face fines and penalties.

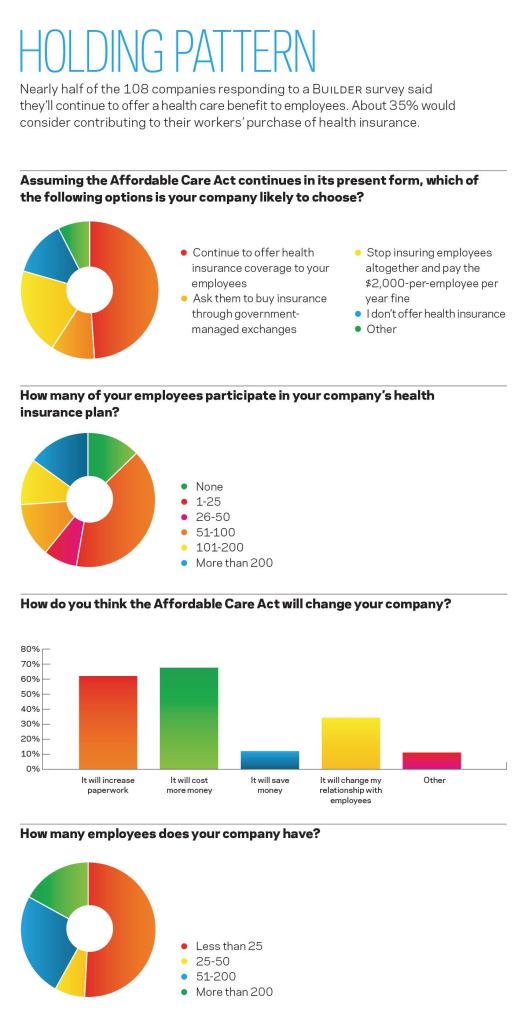

It’s hard to know whether the Act’s potential implications for their companies have sunk in yet with builders. Calls to executives at more than 25 home building companies found many of them unwilling to discuss this topic and not exactly up to speed on its details. “It’s still too early,” was the response from a spokesperson for one of the housing industry’s top 10 builders.

Indeed, corporate America’s attitude toward the Act can be described as “the Good, the Bad, and the Indifferent,” deadpans Larry Harrison, a 23-year insurance broker based in Las Vegas. Harrison blames any obliviousness on Obamacare’s complexity, which he asserts “is designed to confuse.”

FINGER IN THE DIKE

One thing builders aren’t confused about, however, is how rising health care costs are taking bigger chunks out of their profits. The numbers are stark: Total national spending on health care approached $2.8 trillion or 18 percent of the U.S. economy in 2011 and is projected to rise to 19.6 percent by 2021 and 25 percent by 2037, according to Congressional Budget Office estimates. The Kaiser Family Foundation calculates that the average family premiums for employer-sponsored coverage rose 113 percent during the 2000s.

Builders that during the housing recession struggled just to maintain basic benefits for their diminished workforces have a major stake in legislation that promises—quixotically, say its critics—to slow the rising tide of health care expenditures.

Enzo Perfetto, manager of Enzoco Homes, a custom builder based in Munson, Ohio, with five employees, says medical costs account for at least 30 percent of his company’s annual operating expenses. Chris Schell of Schell Brothers in Rehoboth Beach, Del., with 90 employees, says health care is his company’s second-highest expense after payroll. “Since I started the company in 2003, general liability insurance has gone down 95 percent but health care rates have increased 10 times, at least. It used to cost us $242 per employee per month for insurance with no deductibles under Blue Cross/Blue Shield; now, it costs more than $2,000, and it’s not even the same insurance.”

Market forces have led builders to shift more of their health care costs onto employees. Woodland Homes of Huntsville, Ala., recently asked its 15 associates to contribute, on average, 35 percent of the cost of their coverage, says CFO Jeannie Samz. Over the past two years, Eastbrook Homes in Grand Rapids, Mich., has been successful in convincing its 35 employees to open Health Savings Accounts (HSAs), which allow them to put aside tax-free dollars for qualified medical expenses. (Eastbrook’s employees are on the hook for the first $4,000 in expenses before insurance kicks in, says CFO Mark Woudstra.)

Louis Genuario Jr., who co-owns the Genuario Cos., a builder/developer in Alexandria, Va., considered an HSA option when, on Aug. 1, carrier Capital Care said rates were going up 25.6 percent from the $65,000 per year the builder was already paying. Instead, Genuario lowered his company’s premiums to $42,000 by shifting his 10 employees into a plan called Healthy Blue 2.0, which Capital Care sets up directly with workers and allows them to put aside $2,650 for expenses, or $5,250 for family coverage. The deductibles are $300 individual/$600 family.

Genuario thinks the Affordable Care Act is compelling employers to scrutinize and scrub their insurance plans. “The Act makes things more complicated” and has the potential for placing companies “in jeopardy” as far as tax liability, he posits. “So we need to have a better understanding of the tax code.” Under the Act, businesses and individuals must also keep precise records of their contributions so as not to miss out on Act-mandated rebates from carriers that don’t spent at least 80 percent of premiums collected on clinical services.

TAXING OBLIGATIONS

A lot of this legislation remains unclear to builders and even brokers who use words such as “ambiguous” and “uncertainty” when they talk about the Act. The Department of Health and Human Services (HHS) and the Internal Revenue Service (IRS) can’t even agree on what “affordable” means in determining which individuals and families will be eligible for insurance-purchasing subsidies. So employers’ obligations to employees’ dependents are cloudy.

But to be clear: The federal government is serious about enforcing this law. The tax revenue provisions of the Act are designed to generate $438 billion to help pay for this reform. To enforce these provisions, the IRS is beefing up its staff by more than 2,000 full-time employees for fiscal years 2012 and 2013, according to the Treasury Inspector General for Taxation. Consequently, “many companies have started paying attention” to what the Act means for them, observes George Givens, senior vice president of The Meltzer Group, a Bethesda, Md.–based insurance broker whose clients includes several builders.

Among its myriad provisions, the Act this year requires employers that process 250 or more W-2 forms to include the value of their company’s health care programs for their associates. All companies must provide HHS with a summary of benefits and coverage.

Next year, the Act gains momentum as 22 new taxes go into effect, including a 0.9 percent Medicare tax on high-income earners and a new 3.8 percent Medicare contribution on capital gains over $200,000 for individuals and $250,000 for families. (On the plus side, the threshold for deducting unreimbursed medical expenses rises to 10 percent of annual gross income, from 7.5 percent.) Companies with more than 200 workers must automatically enroll them in health care plans. And employees’ tax-free contributions to flexible spending accounts will be capped at $2,500 a year.

FAIR EXCHANGE?

The biggest decision for builders and employees will be whether to purchase health insurance through exchanges starting in 2014 or to stick with employer-sponsored plans. Employers with 50 or more full-time workers that don’t offer insurance starting that year will be subject to annual fines of $2,000 per worker (the first 30 employees are exempt). Adult Americans who decide not to buy insurance are subject to annual fines of $695.

Exchanges are likely to interest employees whose household incomes are less than 400 percent of the federal poverty level ($92,200 in 2011), because they’ll be eligible for government subsidies to purchase coverage through the exchanges.

In 2014, the Act will limit employees’ deductibles and out-of-pocket expenses to no more than 9.5 percent of their incomes and reduce the waiting period for an employer to add a new worker to its health care plan to 90 days. Such limits could make decisions about exchanges simpler for builders such as Enzoco Homes, whose current deductibles are $5,000 for individuals and $10,000 for families. Schell Brothers’ family plan has a $15,000 deductible, of which the employee pays the first $6,000 and Schell the next $9,000 before the insurer takes over.

Ed Byrd, a founder of Southeastern Insurance Consultants in Irmo, S.C., predicts that up to 75 percent of Americans might eventually end up buying insurance through state or federal exchanges. “For some employers, exchanges are definitely going to be the answer.” Employer-sponsored insurance could become less attractive by 2018, when the Act imposes a 40 percent excise tax on so-called “Cadillac” plans valued at more than $10,200 per individual and $27,500 per family. That could complicate matters for Craftmark Homes in McLean, Va., whose self-insured health care plan covers the first $35,000 of medical expenses for its associates, says Craftmark’s CEO Ken Malm.

Does this mean employers will stop offering health care benefits entirely? Probably not. The accounting firm Deloitte recently polled 560 companies in different industry sectors with 50 or more workers that currently offer health care plans and found that only one in 11 intends to drop coverage within the next three years. Bigger companies are far less prone to discontinue benefits.

The Act actually encourages businesses to stay in the mix, as it offers those with fewer than 25 employees and average annual wages under $50,000 a tax credit of 35 percent through 2013, and 50 percent thereafter, if they buy insurance for their employees and pay at least half of the premium costs.

Even if their employees flock to exchanges, many companies are expected to help them pay for it through defined contributions. “We did this with cell phones, so why not health care?” asks Richard Gaylord, a custom builder in Raleigh, N.C.

The CFO of a large production builder in the western U.S., who asked not to be quoted by name, says that while his company would probably continue to offer health care benefits, “they could be completely altered,” as the Act mandates that plans include options for employees with pre-existing medical conditions. As the Act doesn’t require companies to insure part-time workers, this CFO suggests that his company might curtail the schedules of some hourly employees.

But when asked if he still sees health care benefits as an employee recruitment and retention tool, the CFO responded, “It’s more like an expectation.”

WRANGLING COSTS WITH WELLNESS

The Affordable Care Act has stirred up a hornet’s nest within the business community that has been vocal in its opposition to new taxes and reporting (which could be particularly onerous for LLCs and S Corps, worries Genuario, the Virginia builder), as well as document filing requirements that some have cast as invasions of privacy.

The Act also raises many questions: Is rationing of services unavoidable to control costs? Will employer-sponsored health care plans lose their tax-deductible status? Will employees have to declare benefits as income? And will—as several brokers fear—younger, lower-income employees, left to make their own choices, gravitate to the least-expensive health care plan with insufficient regard for the quality or comprehensiveness of that coverage?

The Medicare component of the Affordable Care Act is now a political football in the presidential campaigns. But Givens, the Maryland broker, doesn’t think the Act will be repealed entirely, regardless of who gets elected. So employers better start thinking about how risk pools will impact their plans. “The thinking behind the Act is that younger, healthier people will be coming into the system. But that may or may not happen,” he says.

Harrison, the Las Vegas broker, opposes the Act and its costs in general but likes the pre-existing component, and predicts that the Act could bring uniformity to wildly disparate state mandates.

But neither Harrison nor most other brokers believe this Act can achieve the Congressional Budget Office’s projections of lowering the federal deficit by $210 billion over 10 years. Brokers chafe at legislation they see as all but eliminating their role as consultants. “I’ve already shifted my practice away from health care,” says Ed Thauer Jr., a broker with Design Underwriting in Grand Rapids, Mich.

The irony is that insurance brokers could be an endangered species at a time when companies need their advice more than ever. Consequently, Byrd and Susan Rider, senior account manager with Gregory & Appel Insurance in Indianapolis, are sanguine about their futures because not every company or employee will take the exchange route, health care insurance rules won’t get any less Byzantine, and businesses will always turn to experts who can lower their risks.

One of the “really strong positives” of this Act, Rider says, is its focus on wellness. Companies can offer employees rewards such as premium discounts up to 20 percent when workers participate in qualified wellness programs. Under the Act that benefit can rise to 35 percent.

That’s good news for a builder such as Schell Brothers, which already has “a ton of wellness programs,” says its CEO, including paying for gym memberships and conducting an annual weight-loss contest.

The byproducts of such programs, says Rider, are healthier, more productive employees who are less likely to be drawing workers’ compensation. And at a time when health care’s rising costs seem intractable, builders should latch onto any modicum of control they can find.

Holding Pattern

Learn more about markets featured in this article: Chicago, IL, Washington, DC.