The Mortgage Book Has Shifted

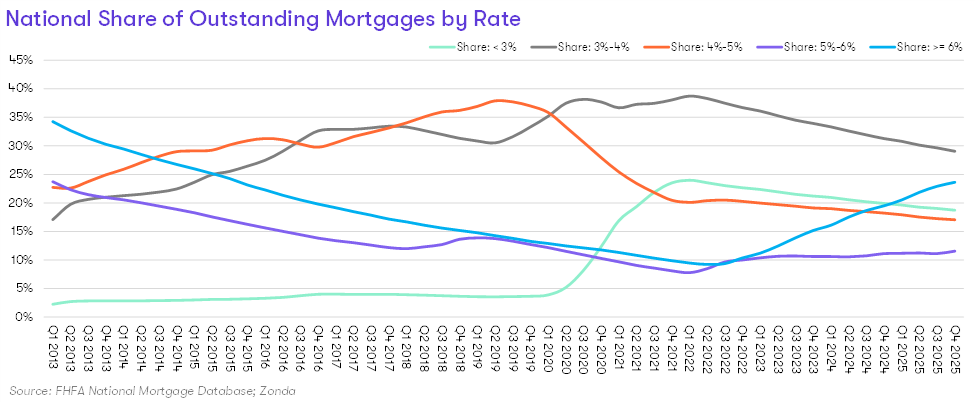

A review of the national share of outstanding mortgages by rate shows just how dramatically the market swung from the post-GFC era to the pandemic refinancing boom and then into the higher-rate environment that followed. Using data from the Federal Housing Finance Agency National Mortgage Database, the chart below highlights how deeply today’s homeowner balance sheet continues to influence housing behavior.

In early 2013, the country was still carrying a sizable block of higher-rate loans. In Q1 2013, 34% of outstanding mortgages had rates at or above 6%, while only 2% sat below 3%. Meanwhile, the middle ranges already represented a meaningful share of the market, with 23% of mortgages between 4% and 5% and another 24% between 5% and 6%.

From there, the decade-long refinance wave steadily pulled borrowers down the curve. The share of mortgages at or above 6% declined consistently from 2013 through 2021, bottoming near 9% during the pandemic refinance era. Over the same stretch, the 4% to 5% range became the industry’s version of “normal,” climbing into the high-30% range by late 2019 before reversing sharply in 2020 and 2021.

The Pandemic Boom Reshaped Consumer Expectations

That reversal is where the chart becomes especially important for builders trying to understand today’s buyer psychology and housing market dynamics.

As mortgage rates collapsed during the pandemic, the share of mortgages below 3% exploded. It represented just 4% of outstanding mortgages as recently as Q1 2020, then jumped to 8% in Q2, 12% in Q3, and 17% by Q4. The momentum continued into 2021, eventually peaking near 24%. In practical terms, nearly one in four homeowners locked in a mortgage rate that is unlikely to return anytime soon.

That matters because homeowners do not compare today’s rates to long-term historical averages. They compare them to their existing monthly payment. A household with a 2.9% mortgage may intellectually understand that a 6% mortgage is historically reasonable, but psychologically and financially, the jump still feels enormous.

As a result, many homeowners became effectively “locked in” to their existing homes, choosing to stay put rather than give up historically low financing. That dynamic has played a major role in limiting resale inventory over the past several years.

The Lock-In Effect May Have Already Peaked

While the lock-in effect remains important, the underlying mortgage mix has already started to shift. As rates moved higher between 2022 and 2025, the share of mortgages below 3% gradually declined to 19% by Q4 2025. At the same time, the market steadily restacked into higher-rate tiers.

The 3% to 4% bucket fell from nearly 39% in 2022 to 29% by late 2025, while the 4% to 5% share dropped to 17%. Meanwhile, the share of mortgages at or above 6% climbed back to 24%, up sharply from the single-digit lows reached during the pandemic refinance boom.

In other words, the mortgage book is slowly normalizing.

That does not mean the lock-in effect has disappeared; millions of homeowners still hold historically low mortgage rates and remain reluctant to move,” said Ali Wolf, chief economist for Zonda and NewHomeSource. “However, the data increasingly suggests the market may be moving beyond peak distortion as more households buy homes based on lifestage and lifestyle changes and the share of owners anchored to ultra-low mortgages gradually shrinks.”

The Builder Advantage

For builders, this transition creates both challenges and opportunities. Elevated mortgage rates continue to pressure affordability and monthly payments, particularly for first-time and payment-sensitive buyers. At the same time, many existing homeowners remain reluctant to move, keeping resale inventory relatively constrained.

Builders, however, retain tools resale sellers rarely offer. Through mortgage buydowns, incentives, spec inventory management, lot positioning, and product design, builders can actively reshape affordability for buyers. In many cases, that means lowering monthly payments without materially reducing headline prices, a critical advantage in today’s payment-sensitive market.

As consumers gradually adjust to a higher-rate financing environment, builders may also be increasingly well positioned to capture buyers who are no longer waiting for a return to pandemic-era mortgage rates.

The insights in this article were taken from more in-depth research reports published in Zonda’s National Outlook.