1

of 5

A year ago, after DSLD Homes in Louisiana joined forces with another local contractor, Vicknair Builders, owner Saun Sullivan predicted confidently that the combined companies would close at least 600 homes in 2011, or 65 percent more than what DSLD had closed the previous year. His projection was under by 87 units.

DSLD has been one of the housing industry’s fastest-growing builders for a while. As of mid-April of this year, it was selling homes in 51 communities in Louisiana and Mississippi, up from 34 communities at the end of 2010. Its accelerated closings last year elevated DSLD to No. 37 on the Builder 100 list for 2011, up from No. 75 for 2010.

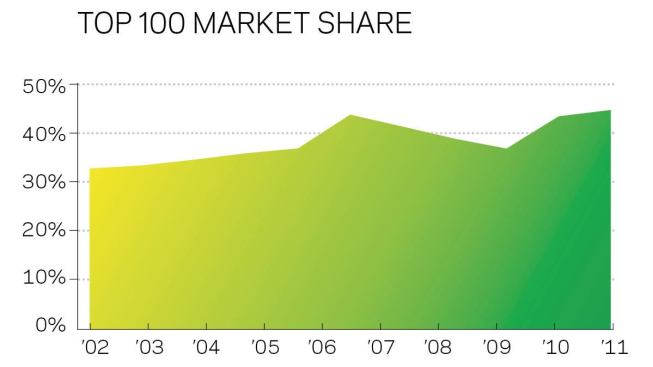

Builders ranked on the top 100 list recorded their highest market-share percentage of closings in a decade and gained ground for the second consecutive year, albeit in a housing market that wasn’t much to crow about. Starts nationally rose by 3.7 percent to 608,800 units in 2011, according to Census Bureau estimates. Of that total, 430,800 were single-family homes, representing an 8.6 percent drop-off from the previous year. Conversely, starts of two or more units—a percentage of which was built to target a rental market that a small but significant number of builders perceive as burgeoning—increased by 54 percent to 178,200 units.

Any new construction, however, faced an unpredictable reception from home buyers. New-home sales and multifamily completions fell last year by 10.2 percent to only 318,000 units. Builders grasping for any shred of good news could point to a reduction in unsold new single-family inventory, to 5.7 months supply from 6.9 months in 2010. That gave builders hope that their products might be more valued by customers returning to the market and comparing new homes with available existing products that include foreclosures and short sales.

Sales of existing homes increased marginally last year, to 4.263 million units. Unsold existing inventory also fell to 8.2 months from 9.4 months in 2010. That shrinkage was attributable, in part, to a retreat in foreclosure activity, down 34 percent to its lowest level since 2007, according to RealtyTrac estimates. However, last year ended with 12 million homeowners underwater on their mortgages, so the final chapters detailing the impact of foreclosures on the housing market have yet to be written.

In this still-volatile business environment, making money remained problematic. Just ask the 13 largest public builders that reported aggregate net losses in 2011 of $746.7 million on $21.4 billion in home building revenue that was, in turn, down 11.5 percent from 2010, according to their filings with the U.S. Securities and Exchange Commission. None of the top 10 for-profit builders had increases in closings or gross revenue (which includes sales from home building, financial services, and other businesses), except for Lennar, the only company that reported a gain in gross revenue. But that didn’t stop the giants from buying land aggressively—sometimes at prices that caused their competitors to scratch their heads in bewilderment—and restarting projects they had mothballed.

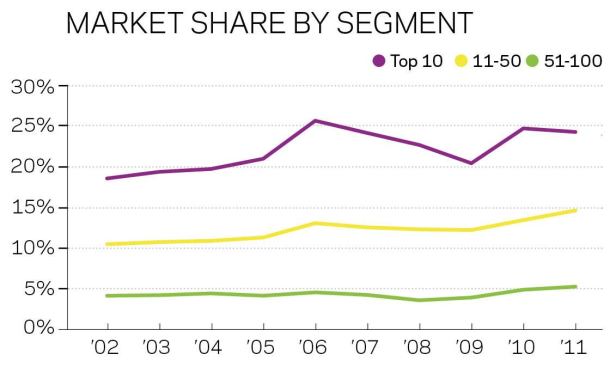

In fact, last year offered more evidence that the recession has played into the hands of the larger builders, and not just the publics. The middle tier of companies within the Builder 100, ranked from 11 to 50, enjoyed the greatest percentage of market-share gain.

Why some builders performed better than others had a lot to do with being in the right place at the right time. Landon Homes, Chesmar Homes, and LGI Homes—which all reported exceptional percentage increases in closings—operate in Texas markets that have avoided the recession’s severest shocks.

Housing demand generated by Fort Benning’s $3.5 billion expansion was the balm that soothed Georgia-based Grayhawk Homes, which moved up 44 slots and cracked into the top 100 in 2011. And when Minnesota–based Rottlund Homes closed last year, Grayhawk was able to scoop up its division in Iowa and now sells homes in six communities around Des Moines.

Military base realignments in the Carolinas have created demand for housing built by Blacksburg, Va.–based HHHunt Corp., which broke into the 2011 top 100 by climbing 71 places. This builder targets a variety of different customers who include buyers seeking senior and golf-resort living to families interested in the amenities of master planned communities. In April 2012, HHHunt announced that 23-year company veteran Daniel Schmitt would be its next president and COO. Schmitt is currently overseeing the development of 12,800 homes in communities throughout Virginia.

After emerging from a year-long bankruptcy in February 2011, Pennsylvania-based Orleans Homebuilders appears to be righting itself, based on its closings last year. CEO George Casey Jr. sees his company’s future success resting on four pillars, which he described last November at the Urban Land Institute’s fall meeting in Los Angeles: Orleans must be market-niche focused, operationally excellent, organizationally efficient, and become a better steward of capital.

“We must build discipline into everything we do,” Casey said about Orleans, and perhaps indirectly about his industry as well.

Learn more about markets featured in this article: Baton Rouge, LA, Houston, TX, Des Moines, IA.