In an attempt to give home buyers a safe alternative to subprime lenders, Congress this year is considering two bills to modernize the FHA. Representing the largest mortgage insurer in the world, FHA lenders offer qualified buyers a low-interest, fixed-rate mortgage backed by the mortgage insurance premiums the borrowers pay as part of their monthly house payment.

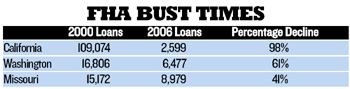

In recent years, the FHA has virtually dropped off the map—in California, FHA loan volume dropped 98 percent between 2000 and 2006—as an option for most home buyers, hampered by loan limits that didn’t keep pace with rising real estate prices. In addition, the FHA’s down-payment requirements were higher than what was widely available in the market. Whereas private lenders can quickly shift practices and offer new products to meet demand, the FHA literally needs an act of Congress to remain competitive.

In 2006, the House of Representatives overwhelmingly passed the Expanding American Homeownership Act to address the issue, but the Senate failed to pass the bill before the session ended. That bill would have allowed the FHA to insure zero–down-payment loans, increase the loan limits to reach more buyers in high-cost markets, increase the loan term to up to 40 years, allow condominiums to be insured as single-family units, and offer risk-based pricing on mortgage insurance premiums, giving a price break to buyers with better credit.

Part of the reason the 2006 bill didn’t pass the Senate was that at that time, the FHA’s loan insurance program was on a high-risk list put out by the General Accounting Office (GAO). The GAO cited concerns about a lack of controls on a wide range of issues, including lending, appraisals, and property disposition. In January 2007, the GAO reported that the FHA had made significant progress and removed the agency from the high-risk list.

Since then, two new bills have been introduced in the House this session. H.R. 1752, co-sponsored by Rep. Judy Biggert (R-Ill.) with 16 other Republican representatives, is identical to her bill that passed in the House last year. H.R. 1852 is co-sponsored by Rep. Barney Frank (D-Mass.), chairman of the House Financial Services Committee, and Maxine Waters (D-Calif.), chairwoman of the House Subcommittee on Housing and Community Opportunity. The latter bill includes many elements of the one the House passed in 2006 as well as some fee reductions in closing costs, the requirement of prepurchase counseling for riskier borrowers, and a contribution of FHA surplus funds to an affordable-housing fund.

Federal Housing Commissioner Brian D. Montgomery notes that both House bills “recognize the need to modernize the FHA, which is a good thing. They both allow for some sort of risk-based pricing, which brings the FHA into line with the rest of the industry. … If we’re going to reach hard-working families, we need some flexibility in the premium structure.”

Modernization would provide a powerful tool for builders serving entry-level buyers, says Kim Shelpman, president and CEO of Melbourne, Fla.–based Holiday Builders and a veteran of the mortgage lending industry.

“It will increase the number of buyers we can get into our homes,” she says. “The FHA is a better program for buyers, because they won’t ever have an interest-only or piggyback loan. When [buyers] make a payment, they’ll build equity in the house.”

Plus, the FHA’s stringent underwriting requirements should help builders feel confident that the deal will progress to closing, Shelpman says. “With a loan that comes through on the FHA, I know the buyer is credit-qualified, income-qualified, and I know I have a buyer who can afford the house.”

Learn more about markets featured in this article: Denver, CO.