Ask the question, “is disruptive innovation likely to occur with any impact in new home building and residential development in the near future?”

If the question comes up among people with long-standing legacy experience in the industry–as it did when I raised it in a recent ULI session with home builders, developers, investors, and consultants–the answer is perfunctory. No. Next question, please.

I beg to differ.

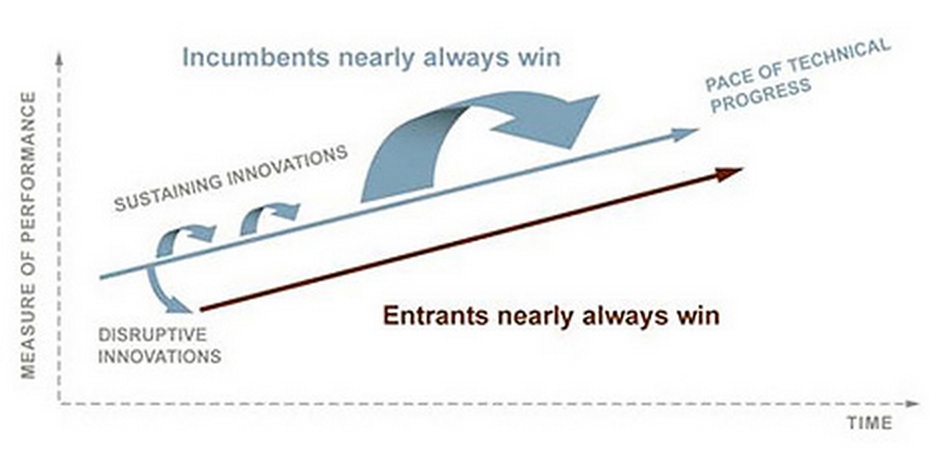

Let’s look first at a definition, and secondly at two pictures, one of a graph and one, of a home. The definition comes from Clayton Christensen, who’s credited with coining the term:

Disruptive innovation describes a process by which a product or service takes root initially in simple applications at the bottom of a market and then relentlessly moves up market, eventually displacing established competitors.

Now, take a look at a diagram that gives you a picture of how disruptive innovation works, particularly as technology advances information, product development, and logistics.

Now, the home.

Let’s consider, for a moment, this one.

Are we overly fixated on entry-level home buyers, or rather their absence as a primary momentum driver in housing’s recovery so far?

If it seems so, it’s not because we’re in any position to cast judgment. We’ve looked hard at the many reasons it’s so challenging for new home builders to break through the capital, local regulatory, cost, and psychographic trends barriers to serve the entry-level community market. There are no easy answers. At the same time, if you look at the work of LGI Homes and D.R. Horton’s Express line, and a handful of other companies whose sweet-spot is somewhere south of the $200,000 mark, it’s clear that it can be done and it is being done.

Our obsession stems more from a worry on behalf of the home building community we serve, not a criticism of it. We worry simply that if those who crusade against housing prevail in their effort to make it impossible for ordinary people to buy a home, then a prized and unique value, the American Dream of homeownership and the promise of economic mobility fades.

Capital has been, and continues to be, the rub. One of the reasons for this is that capital investment hardly ever works predictively. Even in “risk-on” environments, capital tends to work “post-dictively.” In other words, if three years of pro formas show that transactions for homes selling for $300,000 and above are outselling homes of $200,000 and below by a two-to-one margin, investors and land investment committees will think you’re crazy to go in with a deal proposing a big starter home community in some outer-ring, path of growth tract.

Thing is, though, if an individual home building company looks at its own volume pacing and sees absorptions in the lower-price tiers starting to kickstart from a very low base to an improved level–as credit-box access improves, lending standards grow ever slightly more accommodative, people retire more student debt, wage growth improves, etc.–then those individual home builders know about the tipping point moment of entry-level demand before capital investors do.

This is where we are in the market now. The money–in the form of yield-thirsty funds–will bore into both AD&C and mortgage lending more aggressively, but bringing inexpensive lots from raw to ready will continue to suppress new-home supply at the lower price realms.

Housing economist Tom Lawler, who posts his insight as part of Bill McBride’s Calculated Risk threads, has the following commentary on the U.S. Census’ Characteristics of New Housing Units, which we wrote about earlier this week. Tom writes:

While the de minimus production of moderately sized and priced new single-family home production over the past few years almost certainly reflects extremely low purchase volumes from entry-level buyers, there is some debate regarding how much of this weak production/sales reflects weak demand, and how much reflects “supply” issues (e.g., an inability of many builders in many markets to produce small, moderately-priced homes at high enough profit margins to make it worth there while.)

Those looking for an eventual rebound in single-family housing production to more “normal” unit levels should realize that such a rebound is extremely unlikely without a major increase in the production of smaller, more moderately priced homes.

Now, let’s go back to the opening thought here. Could disruptive innovation change how the market responds to the fact that many, many, many Americans–some great number of whom are currently priced out of homeownership–want and will work for their shot at the American Dream?

Will it be modular? Will it be Blu Homes or some hybrid of stick and factory-built, vertically-integrated process?

Or will more single-family builders respond to the need for below-$200,000 homes?

So you can tell me, over, and over, and over again, my friend, you don’t believe we’re on the eve of disruption.