Slightly fewer than one in three Americans over the age of 25 has a college degree. For the housing and homeownership economy, that means two things. One, is that wages and income for one in three Americans are vastly better compared with the two-thirds of people who’ve only got a high school diploma. Two, is that many of the younger set of those college graduates carry debt–somewhere around an average of $30,000–into their early years in the workforce.

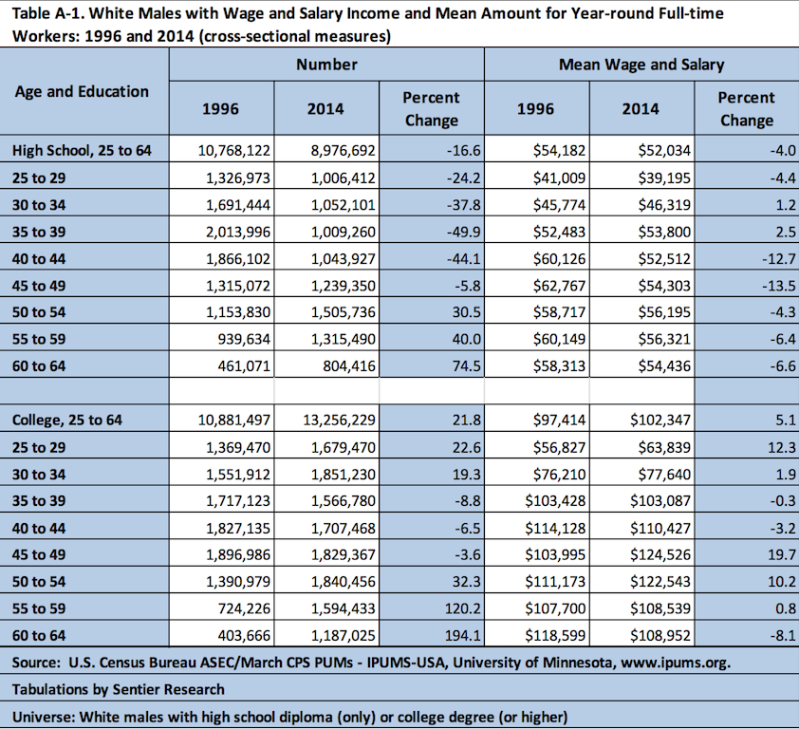

New income trend data from Sentier Research notes that the median wage and salary of a 30 to 34 year-old college-educated male is about $77,640. Compare that figure to the same 30 to 34-year-old male group two decades ago–1996–and you see about a 2% difference, upward. Now, look at the next age group up, for educated males, the 35 to 39-year-old group, where the median wage and salary clocks in at $103,087.

Now, hold that thought. College educated males, making just under $80k, from 30 through age 34 or so, and just over $100K between the years 35 and 39.

Two observations. One is that when you bake in the population growth for those two age and demographic segments over the past decade and look at the coming decade — ages 30 to 34, and males with college degrees — you get 1) a massive spike in the aggregated figure for college debt and 2) a massive increase in the absolute number of households earning a median $80k at 30 to 34 and $100k at 35 to 39.

Now, here’s fresh data on the college debt factor from NeighborWorks America, whose net net finding in its sample base is that nine out of 10 adults affirm that homeownership and the American Dream go together like peas in a pod.

Thing is, this same sample base believes that the dream of homeownership and the reality of student debt are in conflict. Thirty percent of respondents, for instance, “know someone whose student loan delayed the purchase of a home.” That’s up a tick from 28% a year ago.

Mathematically, that means two things. One is that, in fact, more of us know someone for whom homeownership running up against his or her college debt issue. Or two, more people are trying for homeownership–student debt or not–which increases the likelihood that you know someone in that state.

Take any random 1,000 American adults–as this study does–and ask them about this issue of college debt impairing would-be home buyers, and you’re likely to hear the same thing. One in three of a total universe of 77 million is a damned sight more significant than one in three of Generation X (57 million), so, the t-word–Trillion dollars-plus in student debt–gets maximum media hype.

But when you look again at college-educated males’ median incomes for ages 30 to 34 and 35 to 39, you see how and why fundamental demand for single-family homeownership has begun now to accelerate on a trajectory that’s got a decade of thrust propelling it.

Have a look at Calculated Risk blog meister Bill McBride’s take here–Demographics: Renting Vs. Owning–on the tie between young adult cohort trends and housing:

On demographics, a large cohort had been moving into the 20 to 29 year old age group (a key age group for renters). Going forward, a large cohort will be moving into the 30 to 39 age group (a key for ownership).

Like other housing analysts, we’d say that the clear “limiters” housing’s next growth spurt are supply constraints, rather than demand risk.

However, contrary to many housing observers, we believe that four big forces account for the supply constraints–not three, as is widely believed

In fact, the fourth, and almost never mentioned factor may be the most suppressive and dangerous of all the supply constraints subduing housing development, starts, and permits.

Labor, lots, and lending get all the attention as the headwinds that curb investment, deployment, and production of new communities and homes.

Still, what about the drag of the “replacement bias” in new home and neighborhood development? That is, all the money it would cost firms to change their legacy business models and operational workflows to update, streamline, retool, integrate, data- and technologically enable their real estate, manufacturing, and marketing to produce residential shelter value as it might be done by a new entrant into the space who has no pre-conceived blueprint on how to create such a platform or set of processes.

That, friends, is where a potential “discontinuity” can occur, setting apart heretofore successful incumbent players and those who will thrive tomorrow. Organizations that can spot and transform their own inertial operations, inefficiency traps, hidebound practices, and outdated workstreams will–the sustaining innovators–will jump the rails to a new “S curve” of market and economic success. The demos are coming. Who’s game to meet them full-force at the pass?