We can almost hit replay on our March analysis, but it is worth repeating with updated data so the point we originally made can really sink in: the existing home market is indeed getting stronger but you need to get used to stronger equating to fewer but better sales.

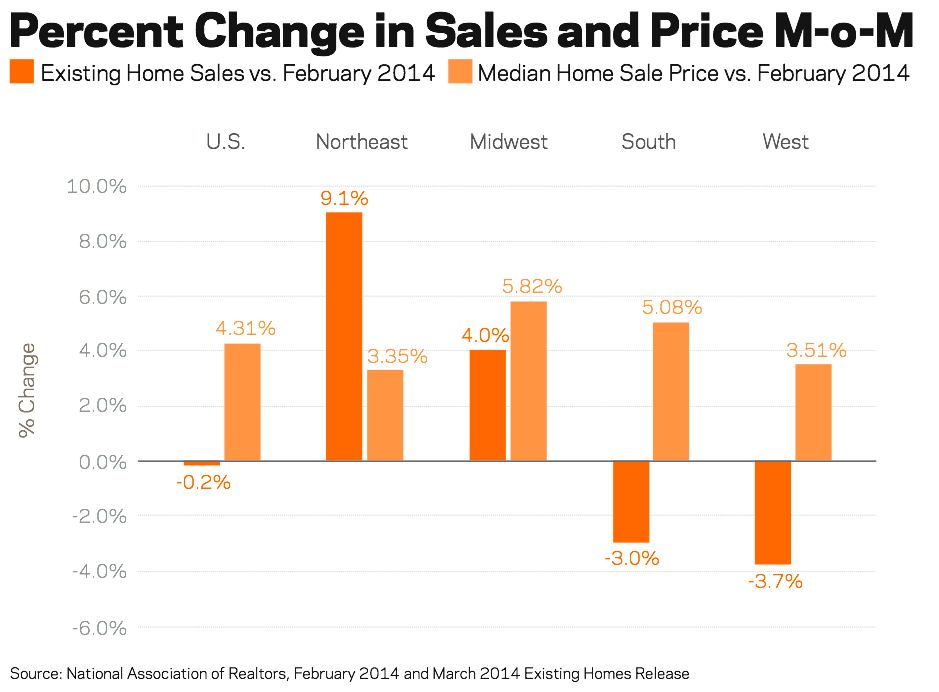

Economists were expecting another slight decline in existing home sales in March from 4.60 million originally reported in February to an annualized rate of 4.55 million in March, and results came in better than expected. The report this morning from the National Association of Realtors (NAR) set the initial March reading at 4.59 million, a decline of 0.2 percent from the unrevised February rate of 4.60 million. However, the volume is not the key number; the most important metrics reveal the composition.

A stronger resale market is one where we see increasing levels of good ole fashioned, non-distressed sales consummated between normal consumers amidst price appreciation and limited supply. We want to see fewer foreclosures, fewer REO sales, and fewer investors. And indeed we are seeing less of what we don’t want to see and more of what we do want to see—it’s just netting out that the totals are slightly lower. And that’s fine because the current rate of single family existing home sales is still almost 15 percent above the 45-year monthly annualized rate.

Leveraging the deed level data we track from around the country, this is what we see: Within existing sales, the share of foreclosures and REO sales combined were down 9.2 percent in the first quarter of this year compared to last the last quarter of 2013, while the share of regular resales was up almost 2 percent. Looking year-over-year the comparisons are even more significant: Foreclosures are down 24 percent in their share, REO sales down 20 percent, and regular resales up 11 percent. Investor activity is indeed on the decline, with the investor share down 1 percent quarter-over-quarter.

Once again we can look at pricing as a key indicator that conditions are improving and not deteriorating. According to the NAR release, the median existing home price in March was $198,500, 7.9 percent up over this time last year. Supporting continued price appreciation is the low level of supply, which remains below normal at 5.2 months of supply.

Despite continued rhetoric about higher mortgage rates hurting the recovery, the facts don’t support that concern. The average interest rate on purchase mortgages on regular resales in the first quarter of 2014 actually declined 7 basis points from the fourth quarter of 2013 due in part to an increasing share of adjustable rate mortgages. The average mortgage rate is up 12 basis points over the first quarter of last year, but as we enter the second half of the year, the year-over-year comparison will start looking better.

Bottom line—housing is getting stronger, not weaker. Don’t be fooled by the seemingly odd context that less is better in existing home sales while real demand improves. We will likely see these conditions continue as the year progresses. These conditions set the table for gains in new home sales, about which we will get the initial March reading tomorrow.

The National Association of Realtors Existing Home Sales full release and data are available here.