William Lyon Homes, Newport Beach, California (NYSE: WLH) on Thursday reported net income available to common stockholders of $10.5 million, or $0.27 per diluted share, for its second quarter ended June 30, 2019, compared to $22.5 million, or $0.57 per diluted share in the prior-year quarter. The results missed analyst expectations of a gain of $0.33 per share.

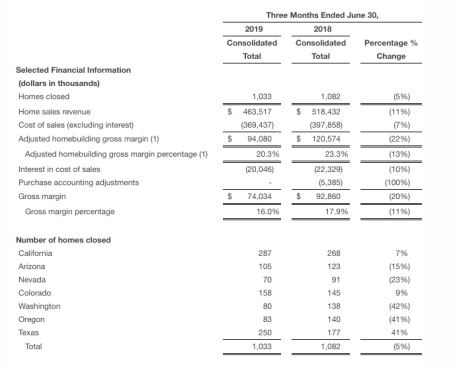

Home sales revenue for the second quarter of 2019 was $463.5 million, as compared to $518.4 million in the year-ago period, a decrease of 11%. The decrease was driven by a 5% decrease in the number of homes closed in 2019, as compared to the prior year period, as well as a decrease in ASP from $479,100 in the second quarter of 2018, to approximately $448,700 in the 2019 period. The decrease in ASP was based on the change in product mix with a higher concentration of deliveries from the Central Texas division.

Home building gross margin percentage during the second quarter of 2019 was 16.0%. Interest in cost of sales was 4.3% during the quarter, and adjusted gross margin percentage was 20.3%.

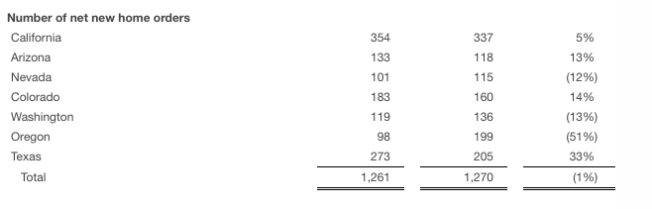

Net new home orders for the quarter were 1,261, an increase of 14% sequentially over the first quarter, and a slight decrease from 1,270 in the second quarter of 2018.

Average community count increased 15% to 123 averages sales location during the second quarter of 2019, compared to 107 during the second quarter of 2018. The monthly absorption rate for the quarter was 3.4 sales per community, compared to 3.1 sales per community in the 2019 first quarter. During the quarter, the monthly absorption pace was 3.5 in April, 3.1 in May and peaking at 3.6 in June. The cancellation rate for the second quarter of 2019 was 13%, in-line with the 12% experienced in the second quarter of last year.

Sales and marketing expense during the second quarter of 2019 improved to 5.5% of home building revenue, compared to 5.6% in the year-ago quarter, primarily due to a decrease in advertising and model operations expense during the quarter. General and administrative expenses increased to 6.4% of home building revenue, compared to 5.5% in the year-ago quarter. Adjusting to exclude the one-time personnel reorganization expenses of $1.2 million in the quarter, general and administrative expenses would have been 6.1%. The company said it believes that the long-term run-rate of this reorganization will result in approximately $3.5 million to $4.0 million of annualized savings.

The company announced the formation of ClosingMark Financial Group, LLC, a wholly-owned subsidiary under which the company intends to operate a full suite of financial services offerings, including title agency, settlement and mortgage services, for the company’s home buyers and other retail customers. ClosingMark has recently commenced its title agency services in the Central Texas, Arizona, Colorado and Nevada markets, and expects to expand its title and settlement services operations into virtually all of the company’s home building markets over the course of the next two quarters.

In April 2019, WLH closed on the acquisition of a mortgage platform, South Pacific Financial Corporation (“SPFC”), which has been rebranded as ClosingMark Home Loans. The company plans to integrating its existing mortgage joint venture operations and loan pipeline into this platform under the ClosingMark brand during the third quarter.

During the three and six months ended June 30, 2019, the company reported a separate financial services segment, to report the operations, assets, and liabilities of the services mentioned above on wholly-owned mortgage operations of ClosingMark Home Loans, the title agency business, as well as unconsolidated mortgage joint ventures.

During the quarter, unconsolidated mortgage joint ventures recorded income of $1.4 million, our wholly-owned financial services recorded a loss of $1.2 million, and we incurred transaction expenses related to the acquisition of SPFC of approximately $990,000.

At quarter end, cash and cash equivalents totaled $35.5 million, owned real estate inventories totaled $2.3 billion, total assets were $2.9 billion and total equity was $1.0 billion. Total debt to book capitalization was 57.9%, and net debt to net book capitalization was 57.3% at June 30, 2019, compared to 56.6% and 55.9% at December 31, 2018, respectively.

Matthew R. Zaist, president and CEO, stated, “We are encouraged by the evolution of the spring selling season, as the monthly absorption pace in the second quarter reflected a sequential increase of 10% over the first quarter to a healthy 3.4 sales per community, and with a number of our divisions up year-over-year on total orders and absorption. We are continuing to see strong absorption from the entry-level and the first-time move up buyers, which are experiencing the highest absorptions in the Company, and contributed 86% of our new home deliveries. In addition, we delivered another strong quarter on our spec inventory, selling and closing 39% more homes in the same quarter than we did in the prior year period. Our focus on the entry-level and first-time move-up home buyers coupled with our modified spec / start strategy has yielded significant improvement in year-over-year backlog conversion and we expect to see the benefits as we move through the balance of the year, allowing for more efficient capital turns which should lead to improved returns and the delevering of our balance sheet.”

Zaist added, “Following the volatility experienced in the back half of last year, we are pleased to see a majority of our markets stable to improving. While still taking a measured approach to pricing, we have been able to reduce incentives and increase prices in certain markets and anticipate sequential improvement in gross margins in the back half of the year. Our anticipated full year results now include deliveries of 4,300 to 4,500 units and revenues of $2.0 billion to $2.075 billion for 2019.”