William Lyon Homes (NYSE: WLH), Newport Beach, California, early Tuesday reported net income of $26.6 million, or $0.68 per diluted share, for the third quarter ended September 30, down from $0.71 per share in the prior-year quarter. Analysts polled by Dow Jones were expecting a gain of $0.66. Shares of WLH were up nearly 6% in heavier-than-usual trading by early afternoon Tuesday.

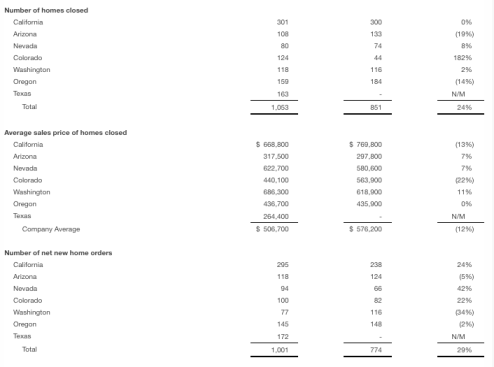

Home sales revenue for the third quarter of 2018 was $533.5 million, as compared to $490.3 million in the year-ago period, an increase of 9%. The increase was driven by a 24% increase in deliveries to 1,053 homes, compared to 851 in the third quarter of 2017.

Net new home orders for the quarter were 1,001, up 29% from 774 in the third quarter of 2017. The overall increase in net new home orders was driven by an increase in community count to 116 average sales locations, from 86 in the year-ago period, an increase of 35%.

The dollar value of homes in backlog was $800.6 million as of September 30, 2018, an increase of 14%, compared to $699.3 million as of September 30, 2017. The increase was driven by a 32% increase in units in backlog to 1,596 from 1,208 in the year-ago period. The average sales price of homes in backlog decreased to $501,600 from $578,900 in the prior year, due to the number of homes in backlog at our Texas division of 248 homes at an average sales price of $275,300, with no comparable amount in the prior year.

Home building gross margin percentage for homes closed during the third quarter of 2018 was 18.2%, up 10 basis points from 18.1% in the third quarter of 2017, and up 30 basis points from 17.9% in the second quarter of 2018.

Sales and marketing expense during the third quarter of 2018 was 5.4% of homebuilding revenue, compared to 4.5% in the year-ago quarter, which is driven by an increase in advertising and outside broker commissions of 60 basis points combined, as well as the impact of the adoption of ASC 606 of 20 basis points, which was adopted on January 1, 2018, requiring the Company to record certain selling costs that were previously recorded as cost of sales to sales and marketing expense. General and administrative expenses increased to 5.6% of homebuilding revenue, compared to 4.7% in the year-ago quarter as a result of continued investment in our growing operating business, incremental information technology investment and further investment in building out our financial services group.

At quarter end, cash and cash equivalents totaled $50.8 million, owned real estate inventories totaled $2.4 billion, total assets were $2.9 billion and total equity was $1.0 billion. Total debt to book capitalization was 60.3%, and net debt to net book capitalization was 59.5% at September 30, 2018, compared to 57.1% and 56.1% at September 30, 2017, and 54.5% and 49.6% at December 31, 2017, respectively.

“While the long-term fundamentals remain positive in the broader economy as well as our local markets, the cost of home ownership has increased with the significant price appreciation in several of our markets over the last few years, combined with the recent rise in mortgage interest rates,” said Matthew R. Zaist, president and CEO. ‘As a result, and most notably in Northern California and Seattle, we have experienced some sales pace moderation, which has led us to adjust our expectations for our fourth quarter results. Overall, in the face of some challenging market conditions, our strong backlog of 1,596 units with a dollar value of over $800 million still puts us in position to finish the year strongly and achieve another year of profitability growth for the Company and a record year in revenue and deliveries. The company expects fourth quarter results to include backlog conversion of 85% to 92.5%, which we believe will contribute significant cash in-flows in the fourth quarter, enabling us to make further progress on our debt reduction for the year and keep us on track toward our long-term balance sheet goals, including targeting 40% debt-to-cap by 2020. Looking forward, our new community openings over the next several quarters will be focused on affordable price points below the market medians with an emphasis on the entry level and active adult buyer segments, which we believe will help to address affordability concerns and drive continued growth for William Lyon Homes.”