TRI Pointe Group, Inc., Irvine (NYSE: TPH) on Tuesday morning reported net income of $99.4 million, or $0.70 per diluted share, for the fourth quarter of 2018, compared to net income available to common stockholders of $74.0 million, or $0.49 per diluted share, for the fourth quarter of 2017. The increase in net income available to common stockholders was primarily driven by a higher home building gross margin and a lower provision for income taxes.

The gain beat analyst expectations of a net of $0.65 per share.

Current year net income available to common stockholders was negatively impacted by the $17.5 million settlement payment. In addition, the company incurred $686,000 of expenses related to the purchase of a Dallas, Texas based builder that closed in the fourth quarter. Prior year net income available to common stockholders was negatively impacted by a $22.0 million tax charge related to the re-measurement of the Company’s net deferred tax assets and a pretax charge of $13.2 million related to the impairment of an investment in an unconsolidated entity. Excluding these items, adjusted net income available to common stockholders was $112.9 million or $0.79 per diluted share for the fourth quarter of 2018, compared to 107.4 million or $0.70 per diluted share for the fourth quarter of 2017.

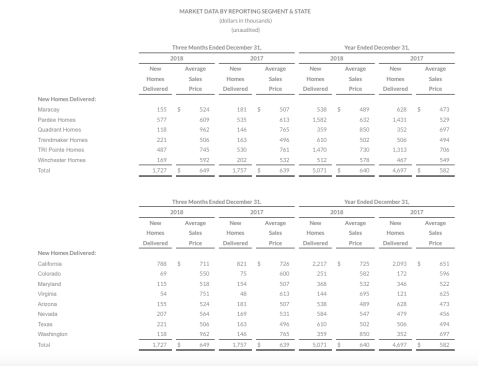

Home sales revenue was flat at $1.1 billion for the fourth quarter of 2018 and 2017. The average selling price of homes delivered during the fourth quarter of 2018 increased 2% to $649,000 from $639,000, offset by a 2% decrease in new homes delivered in the fourth quarter of 2018 to 1,727 from 1,757.

Home building gross margin percentage for the fourth quarter of 2018 increased to 21.9% compared to 21.7% for the fourth quarter of 2017. Excluding interest, impairments and lot option abandonments in cost of home sales, adjusted home building gross margin percentage was 24.8% for the fourth quarter of 2018 compared to 24.2% for the fourth quarter of 2017.

Selling, general and administrative (“SG&A”) expense for the fourth quarter of 2018 increased to 9.1% of home sales revenue as compared to 7.2% for the fourth quarter of 2017 due to expansion initiatives, including the expansion into the Carolinas, Sacramento and Dallas markets. In addition, the adoption of Accounting Standards Codification 606 resulted in various sales office, model and other marketing related costs that were previously capitalized to inventory and amortized through cost of home sales being expensed when incurred to selling expense or capitalized to other assets and amortized to selling expense.

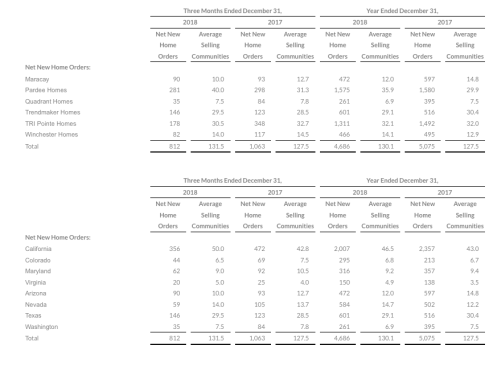

New home orders decreased 24% to 812 homes for the fourth quarter of 2018, as compared to 1,063 homes for the same period in 2017. Average selling communities was 131.5 for the fourth quarter of 2018 compared to 127.5 for the fourth quarter of 2017. New home orders per average selling community for the fourth quarter of 2018 was 6.2 orders (2.1 monthly) compared to 8.3 orders (2.8 monthly) during the fourth quarter of 2017.

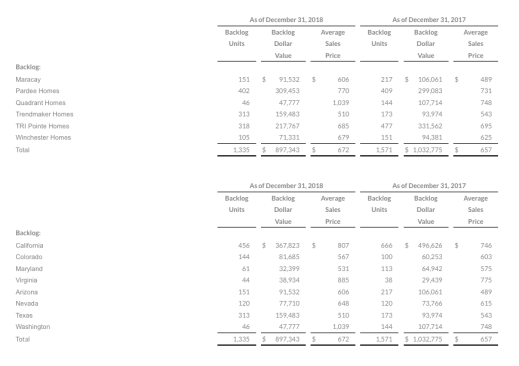

The company ended the quarter with 1,335 homes in backlog, representing approximately $897.3 million. The average selling price of homes in backlog as of December 31, 2018 increased $15,000, or 2%, to $672,000 compared to $657,000 at December 31, 2017.

Results for the full year included:

- Net income available to common stockholders was $269.9 million, or $1.81 per diluted share, compared to $187.2 million, or $1.21 per diluted share. Adjusted net income available to common stockholders for the full year 2018 was $283.6 million, or $1.90 per diluted share, after excluding the $17.5 million settlement payment and $686,000 of transaction expenses related to the Dallas acquisition. Adjusted net income available to common stockholders for the full year 2017 was $220.6 million, or $1.42 per diluted share, after excluding the $22.0 million tax charge related to the re-measurement of the Company’s net deferred tax assets and the $13.2 million pretax charge related to the impairment of an investment in an unconsolidated entity.

- Home sales revenue of $3.2 billion compared to $2.7 billion, an increase of 19%

• New home deliveries of 5,071 homes compared to 4,697 homes, an increase of 8%• Average sales price of homes delivered of $640,000 compared to $582,000, an increase of 10%

- Home building gross margin percentage of 21.8% compared to 20.5%, an increase of 130 basis points

• Excluding interest, impairments and lot option abandonments, adjusted home building gross margin percentage was 24.5%

- SG&A expense as a percentage of homes sales revenue of 10.6% compared to 10.1%, an increase of 50 basis points

- New home orders of 4,686 compared to 5,075, a decrease of 8%

- Active selling communities averaged 130.1 compared to 127.5, an increase of 2%

• New home orders per average selling community decreased by 9% to 36.0 orders (3.0 monthly) compared to 39.8 orders (3.3 monthly)• Cancellation rate of 18% compared to 15%, an increase of 300 basis points

- Repurchased 10,392,609 shares of common stock at an average price of $14.05 for an aggregate dollar amount of $146.1 million in the full year ended December 31, 2018

“2018 was a record-setting year for TRI Pointe Group as we delivered over 5,000 homes for the first time in our company’s history and recorded net income in excess of $270 million,” said Doug Bauer, CEO of TRI Pointe Group. “We established a presence in two new markets – Dallas and the Carolinas – expanding our geographic reach and further diversifying our operations. We also generated over $300 million in cash from operations and ended the year in excellent financial shape with a net debt to net capital ratio of 35.5%.”

Bauer continued, “2018 was also a year of two halves, as the strong sales momentum we experienced in the first part of the year dissipated in the back half of the year as buyers pulled back from the market in response to a rise in interest rates and higher home prices. While this recent market correction adds an element of uncertainty to our industry in the short-term, we remain encouraged about the outlook over the long-term thanks to the under supplied nature of our industry, strong demographics and job growth. We continue to stay focused on our long-term goals while also adjusting our business to remain competitive in the current environment. With a seasoned leadership team, well located communities and a strong balance sheet, we believe that TRI Pointe Group is well positioned for long-term success.”

“Product differentiation is critical in a more challenging demand environment, which is why TRI Pointe Group continues to focus on ways to distinguish itself from the competition with innovative home designs and customer-centric features like smart home technologies,” said TRI Pointe Group President and Chief Operating Officer Tom Mitchell. “We remain focused on core locations for our communities, targeting sites that offer easy access to employment centers, quality schools and vibrant neighborhoods. We believe that offering customers homes that are tailored to their needs in places that they want to live is the right strategy for long-term success and builds a premium brand perception in our local markets.”