Taylor Morrison Home Corp., Scottsdale (NYSE:TMHC) on Wednesday morning reported net income of $9.05 million, or $0.08 per share, for the fourth quarter ended Dec. 31, 2018. The gain compared with a net of $19.9 million in the prior year quarter. The gain missed the consensus estimate of analysts polled by Dow Jones of a gain of $0.47 per share.

The results included $96 million in expenses resulting from the AV Homes acquisition, costs associated with the company’s Canadian unwind and corporate reorganization, land charges and an increase in reserves related to remediating a warranty issue.

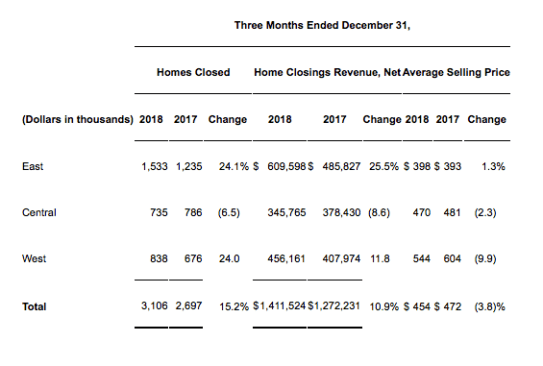

Revenue rose to $1.46 billion from $1.3 billion in the prior-year quarter. Deliveries rose 15.2% to 1,533 homes as home closing revenue climbed 10.9 to $1.41 billion. The average selling price fell 3.8% to $454,000.

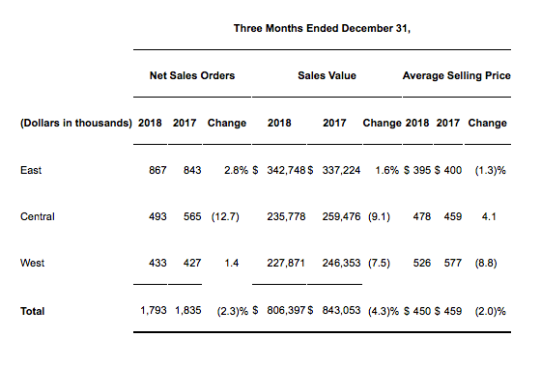

New orders were up 2.3% to 1,793 with a sales value of $806. million, down 4.3% from a year earlier. The average selling price of new orders fell 2% to $450,000.

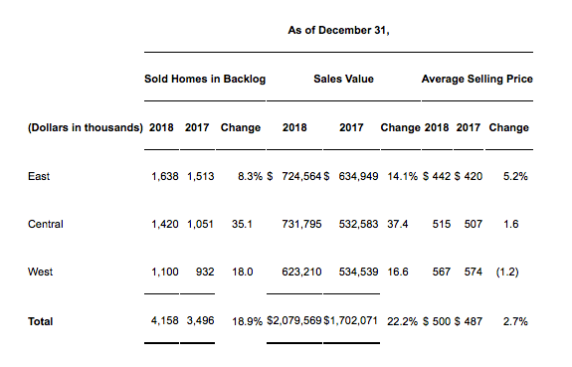

Homes in backlog rose 18.9% to 4,158 with a value of $2.07 billion, up 22.2%.

For the full year:

- Home closings were 8,760, a 9% increase over the prior year

- Total revenue was $4.2 billion, an almost 9% increase over the prior year

- Net sales orders were 8,400 and sales per outlet were 2.3

- Home closings gross margin, inclusive of capitalized interest, was 17.1%

- Adjusted home closings gross margin, inclusive of capitalized interest, was 18.2%

- Net income was $210 million and net income adjusted to exclude unusual items was $306 million

The company ended the year with $330 million in cash. Since the start of the fourth quarter 2018 through February 11, 2019, $196 million was spent repurchasing 11.7 million shares at an average stock price of $16.72. Since the closing of the AV transaction, the Company has reduced its share count by 10%. This exceeds the 9.0 million shares issued in the AV acquisition by 30%. As of December 31, 2018, Taylor Morrison owned or controlled approximately 57,000 lots, representing 5.5 years of supply.

“We continue to believe that the current new home sales environment has best been described as a break in momentum as the industry finds its new normal,” said Chairman and CEO, Sheryl Palmer. “The conditions the industry experienced during the back half of 2018 in regard to interest rates, affordability and the resulting press coverage, led many potential buyers that had been in the market to take a wait and see approach. With that said, there continues to be plenty of macro data points that give us confidence in the near-term outlook. Unemployment and job creation are still at historically very healthy levels, incomes continue to grow, many of the major markets in the U.S. continue to have limited housing supply and the industry continues to be under-built based on historical averages.”

Palmer added, “It’s been about four months since we closed the AV acquisition and I’m happy to report that we are on track with our integration plan – and in some areas, well ahead of schedule. Based on our work to-date, we can comfortably take the run rate synergy estimate up to $40 million, $10 million more than originally communicated.”